June 1st marks the official opening of the longest railway tunnel on Earth, cutting through the Alps.

Official website. Profile of the rail track between Zurich and Lugano. Report about the contender.

June 1st marks the official opening of the longest railway tunnel on Earth, cutting through the Alps.

Official website. Profile of the rail track between Zurich and Lugano. Report about the contender.

In the FT, John Kay points out that basic income proposals have one major drawback: They are very—expensive.

Not everyone agrees. Switzerland will hold a national referendum on the introduction of an unconditional basic income on June 5th, 2016. The supporters of the proposal write:

A basic income already exists today. Everyone obtains one from somewhere; otherwise we would not be able to live. In our society today, no one can survive without an income. The level of a basic income is currently included in the existing incomes. The shift that is needed now is to make current incomes free of conditions up to the level of this basic economic security. In fact, the introduction of an unconditional basic income does not cost anything. To assure basic security by means of a social contract will bring about a new situation for income of all origins. It opens up the possibility for negotiations at all levels. Principally, the existing incomes could be decreased by the amount of the basic income.

Addendum: The Economist discusses the pros and cons of universal basic income proposals.

In the FT, Martin Wolf discusses Mervyn King’s proposal to make the central bank a “pawnbroker for all seasons” as laid out in King’s recent book “The End of Alchemy.”

Lord King offers a novel alternative. Central banks would still act as lenders of last resort. But they would no longer be forced to lend against virtually any asset, since that very possibility must create moral hazard. Instead, they would agree the terms on which they would lend against assets in a crisis, including relevant haircuts, in advance. The size of these haircuts would be a “tax on alchemy”. They would be set at tough levels and could not be altered in a crisis. The central bank would have become a “pawnbroker for all seasons”.

The key part of this quote is “could not be altered in a crisis.” Central banks and governments have always found it very difficult to commit not to support systemically (or politically) important players ex post. This problem lies at the heart of many problems in the financial system and elsewhere. By assuming that central banks could commit under the proposed arrangement, the proposal abstracts from a key friction.

In the Richmond Fed’s Econ Focus, Eric Leeper explains his views.

My view is that central banks have put far too many resources into understanding tiny fluctuations and too few resources into the things that actually matter. …

Something like the basic Taylor rule doesn’t really serve as a useful litmus test for what policy is doing in the face of these DCDs, so it’s a little bizarre to me that a lot of central banks routinely calculate what the path of the interest rate would be with a simple Taylor rule as if that’s a useful benchmark. It’s not obvious to me what that’s a benchmark for.

Now, how all of [current policy] ties into the active/passive framework is really an open question. A lot of it depends on what you think is going to happen to the Fed’s balance sheet.

… the recovery from the Great Depression in 1933 when Roosevelt took the United States off the gold standard. Going off the gold standard converted government debt from effectively real debt to nominal debt because the price level under the gold standard was beyond the control of the government. At the same time, the fiscal actions Roosevelt undertook were what nowadays we would call an unbacked fiscal expansion. … This is like a fiscal rule that says the government will run deficits until the price level recovers to some pre-depression level. And the Fed was just keeping the interest rate flat. So it looked a lot like passive monetary/ active fiscal.

The thing is, there’s not a lot of theoretical justification for creating these walls. What we’re finding more and more is that there’s always some role in optimal policy for using surprise inflation to revalue debt and bond prices, so long as there is some maturity to government debt. … maybe it is a slippery slope once you’re in the political realm. But from an academic perspective, if your objective is to arrive at a rule that would be mechanically followed by a central bank, then there’s no harm in having fiscal variables enter that rule.

On VoxEU, Torben Andersen and Jonas Maibom point out that empirical findings of a positive correlation between efficiency and equity need not contradict elementary theoretical predictions.

The trade-off [between efficiency and equity] applies at the frontier of the possibility set of combinations of economic performance and income equality available to policy makers. If policies and institutions are ‘well-designed’, the country is at the frontier. There is no free lunch and a trade-off inevitably arises.

However, there may be many historical, institutional and political reasons why countries are not at the frontier. … in which case there is scope for improvements in both economic performance and income equality.

This insight leaves one important message. In cross-country comparisons … differences in the distance to the frontier should be accounted for …

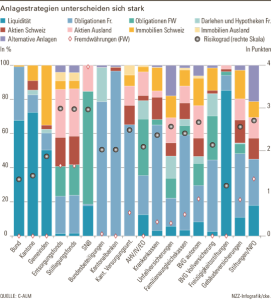

In the NZZ, Michael Schaefer reports about a study that analyzes the portfolio composition of public sector entities and social security institutions. Cantons and the Federation mostly hold cash. The SNB’s portfolio is among the riskiest.

He wants to “fix the country the right way and from the ground up.” His economic policy proposals are well known (among economists), see here. He also wants to confront North Korea and Iran.

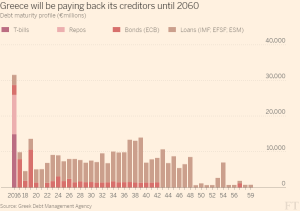

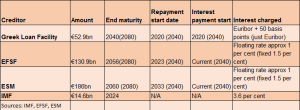

In the FT, Mehreen Khan offers a “Greek debt dilemma cheat sheet.”

In the FT, Ralph Atkins and Thomas Hale report that senior creditors will effectively receive 90 percent of their money back.

An earlier post covered the background of the bank failure.

In the NZZ,

In the FT, Richard Waters reports about the advent of the automated company.

The DAO — an acronym of decentralised autonomous organisation, the name given to such entities — has been set up to invest in other businesses, making it a form of investor-directed venture capital fund. … The organisation is governed by a set of so-called smart contracts which run on the Ethereum blockchain, a public ledger designed to make its operations transparent and enforceable.

In other words, the code provides a commitment mechanism. Imagine a world where government interventions can be encoded in a similar way. This could open the way for solving a central problem of democratic societies: The time inconsistency of optimal government plans.

From The Economist:

The Greens/EFA group in the European Parliament wants the European Union to exert more pressure on the United States: the US should no longer serve as a “tax haven” for European tax dodgers. Proposed measures include blacklisting and a FATCA-type 30% withholding tax on EU-sourced payments.

From the executive summary of the report commissioned by the group:

Two global transparency initiatives are underway that could help tackle financial crimes including tax evasion, money laundering and corruption: registration of beneficial ownership for companies (to identify the real persons owning or controlling such companies) and automatic exchange of bank account information between tax administrations. The European Union has made progress in both respects, with the adoption of a 4th anti-money laundering Directive (in May 2015) and by committing to implement the OECD’s common reporting standard for automatic exchange of financial account information. The United States (U.S.), in contrast, has done neither so far.

On May 5th, 2016 the U.S. announced new measures to improve its financial transparency, although not all the texts of the proposed regulations were provided. The U.S. Treasury announced three new measures: … In any case, not only would some of these new rules require Congress approval, but even the U.S. Treasury final proposals on beneficial ownership collection by financial institutions are not enough to solve all the problems nor to bring the U.S. into line with the OECD’s standard for automatic exchange of information. …

Two main issues in the U.S. affect the global progress towards transparency: … Company registration is regulated by each of the 50 states’ law. In 14 states, companies may be created identifying neither shareholders nor managers. At the federal level, tax rules require filing some information to obtain an Employer Identification Number (EIN). However, not all companies require an EIN and, even if they do, the ‘beneficial owners’ (the actual natural persons owning or controlling the company) are not necessarily among the information to be provided. Companies only have to identify one ‘responsible party’, who may be a nominee director. In order to (partially) address this, the White House 2017 budget proposal and the new measures proposed on May 5th, 2016 suggest requiring all companies (or according to the May 5th proposed rules, at least some foreign-owned disregarded entities, such as single-member limited liability companies) to obtain an EIN. Not only does this proposal need to become effective, but information would apparently still be about the ‘responsible party’ and not necessarily about the real physical person owning and controlling the company (the so-called beneficial owner).

… The U.S. has refused to join the trend for multilateral automatic exchange of information. Instead, it will implement its domestic law called the Foreign Account Tax Compliance Act (FATCA) and the related Inter-Governmental Agreements signed with other countries. However, these involve unequal exchanges of information: the U.S. receives more information than what it sends (for example, about beneficial ownership data). Oddly, though, the OECD did not include the U.S. among jurisdictions that did not commit to its new standard.

Even if the U.S. committed to exchange equal levels of information in the future, the current U.S. legal framework does not allow its financial institutions to collect beneficial ownership information for all relevant cases covered by the OECD’s global automatic exchange of information standard. U.S. financial institutions are currently only required to obtain information on beneficial owners for correspondent banking (i.e. accounts held for foreign financial institutions) and for private banking of non-U.S. clients (accounts holding more than USD 1 million).

Final rules to address these limitations have been announced on May 5th, 2016 although financial institutions must comply with them only by May 11th, 2018. However, the final rules still have the same problems that the IMF identified regarding the 2014 version of the rules so they will not fix all the problems. Remaining shortcomings include: some entities will still not be covered (i.e. insurance companies), the definition of ‘beneficial owner’ is incomplete (it does not include the ‘control through other means’ test, meaning that if you cannot identify at least one person owning 25% or more of the shares, financial institutions should try to find someone who controls the company through other means, before identifying only someone with a managerial position-who may be a nominee director), the verification of information would rely mainly on customer’s own certification, information on beneficial owners would be required for new accounts only (not for existing ones) and it will not need to be updated after the first time of collection, unless the financial institution becomes aware of changes as part of monitoring for risks. In addition, trusts will not be required to provide beneficial ownership information unless they own enough equity in an entity, such as a company, required to provide this information.

To fix this situation and promote equal levels of transparency, this paper provides a series of recommendations. For example, the European Union should consider including the U.S. in the upcoming list of tax havens, unless it effectively ensures registration of beneficial ownership information for companies and commits to equal levels of automatic exchange of information with European Union countries. Ideally, all financial centres should effectively implement the OECD standard for automatic exchange of information (by becoming a party to the OECD Amended Multilateral Tax Convention, signing the Multilateral Competent Authority Agreement and agreeing to exchange information with all other cosignatories). The European Union could thus consider imposing a sanction (such as a 30% withholding tax on all EU-sourced payments) against any financial institution that refuses to automatically exchange information about EU residents holding accounts abroad. In a second stage, sanctions could also be used to ensure that financial institutions from financial centres will also provide information to developing countries with which the European Union is already exchanging information.

Reports by René Höltschi in the NZZ as well as Markus Fruehauf und Winand von Petersdorff in the FAZ.

Finanz und Wirtschaft, April 30, 2016. PDF. Ökonomenstimme, May 6, 2016. HTML.

The winners and losers of the current monetary environment are not that easy to identify. Investors holding long-term, non-indexed debt gain as unexpectedly low inflation shifts wealth from borrowers to lenders. Governments suffer from increased real debt burdens and reduced revenue due to effectively lower capital income tax rates. Policies that succeed in affecting the real exchange rate entail redistribution.

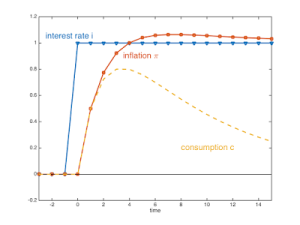

On his blog, John Cochrane offers a stripped down model and some intuition for why inflation would rise after an increase in the interest rate. The model features the usual Euler (IS) equation and a Mickey Mouse Phillips curve—inflation is proportional to consumption (or output). The intuition:

During the time of high real interest rates — when the nominal rate has risen, but inflation has not yet caught up — consumption must grow faster [the Euler equation, DN]. … Since more consumption pushes up prices, giving more inflation, inflation must also rise during the period of high consumption growth.

Also:

I really like that the Phillips curve here is so completely old fashioned. This is Phillips’ Phillips curve, with a permanent inflation-output tradeoff. That fact shows squarely where the neo-Fisherian result comes from. The forward-looking intertemporal-substitution IS equation is the central ingredient.

A slightly more plausible model with an accelerationist Phillips curve and very slowly adjusting adaptive expectations yields the following responses to an increase in the nominal interest rate:

John writes:

As you can see, we still have a completely positive response. Inflation ends up moving one for one with the rate change. Consumption booms and then slowly reverts to zero. …

The positive consumption response does not survive with more realistic or better grounded Phillips curves. With the standard forward looking new Keynesian Phillips curve inflation looks about the same, but output goes down throughout the episode: you get stagflation.

A November 2015 paper on the topic by James Bullard.

A critique by Mariana García-Schmidt and Michael Woodford in an NBER working paper. Abstract:

We illustrate a pitfall that can result from the common practice of assessing alternative monetary policies purely by considering the perfect foresight equilibria (PFE) consistent with the proposed rule. In a standard New Keynesian model, such analysis may seem to support the “Neo-Fisherian” proposition according to which low nominal interest rates can cause inflation to be lower. We propose instead an explicit cognitive process by which agents may form their expectations of future endogenous variables. Under some circumstances, a PFE can arise as a limiting case of our more general concept of reflective equilibrium, when the process of reflection is pursued sufficiently far. But we show that an announced intention to fix the nominal interest rate for a long enough period of time creates a situation in which reflective equilibrium need not resemble any PFE. In our view, this makes PFE predictions not plausible outcomes in the case of such policies. Our alternative approach implies that a commitment to keep interest rates low should raise inflation and output, though by less than some PFE analyses apply.

On his blog, Stephen Williamson addresses “Neo-Fisherian Denial.” Williamson starts with the model analyzed by Cochrane (see above) featuring a Mickey Mouse Phillips curve. He argues:

[This] NK model actually doesn’t conform to conventional central banking beliefs about how monetary policy works. What’s going on? … an increase in the current nominal interest rate will increase the real interest rate, everything else held constant. This implies that future consumption (output) must be higher than current consumption, for consumers to be happy with their consumption profile given the higher nominal interest rate. But, it turns out that this is achieved not through a reduction in current output and consumption, but through an increase in future output and consumption. This serves, through the Phillips curve mechanism, to increase future inflation relative to current inflation. Then, along the path to the new steady state, output and inflation increase.

Williamson recalls the “perils” of Taylor rules. And he addresses the critique by Garcia-Schmidt and Woodford:

Some people (e.g. Garcia-Schmidt and Woodford) have argued that Neo-Fisherian results go out the window in NK models under learning rules. As was shown above, these models are always fundamentally Fisherian in that any monetary policy rule has to somehow adhere to Fisherian logic on average – basically the long-run nominal interest rate is the inflation anchor. But there can also be learning rules that give very Fisherian results. …

Williamson also argues that other (non-Keynesian) monetary models give neo-Fisherian results as well.

A few years ago, also on his blog, Stephen Williamson argued that lowering the interest rate (by engaging in QE) might also affect the real interest rate:

… short-run liquidity effects are short-lived. Further, my work shows that there is another liquidity effect, associated with the interest bearing liquid assets, that causes the long run real rate to increase as a result of QE. … which implies lower inflation.

Further, there are other forces in play … The destruction of private sources of collateral and the shaky state of sovereign governments in parts of the world gave U.S. government debt a large liquidity premium – i.e. those things reduced real interest rates. As those effects go away over time, real rates of return will rise, shifting up the long-run Fisher relation, and reducing inflation if the Fed keeps the nominal interest rate at the zero lower bound.

In a paper, Peter Rupert and Roman Sustek dig deeper. In the abstract they write:

The monetary transmission mechanism in New-Keynesian models is put to scrutiny, focusing on the role of capital. We demonstrate that, contrary to a widely held view, the transmission mechanism does not operate through a real interest rate channel. Instead, as a first pass, inflation is determined by Fisherian principles, through current and expected future monetary policy shocks, while output is then pinned down by the New-Keynesian Phillips curve. The real rate largely only reflects consumption smoothing. In fact, declines in output and inflation are consistent with a decline, increase, or no change in the ex-ante real rate.

Addendum (May 11–12, 2016): In the abstract of their NBER working paper, Julio Garín, Robert Lester and Eric Sims write:

Increasing the inflation target in a textbook New Keynesian (NK) model may require increasing, rather than decreasing, the nominal interest rate in the short run. We refer to this positive short run co-movement between the nominal interest rate and inflation conditional on a nominal shock as Neo-Fisherianism. We show that the NK model is more likely to be Neo-Fisherian the more persistent is the change in the inflation target and the more flexible are prices. Neo-Fisherianism is driven by the forward-looking nature of the model. Modifications which make the framework less forward-looking make it less likely for the model to exhibit Neo-Fisherianism. As an example, we show that a modest and empirically realistic fraction of “rule of thumb” price-setters may altogether eliminate Neo-Fisherianism in the textbook model.

In his 2008 textbook, Jordi Gali discusses the role of the persistence of monetary policy shocks (page 51). If it is sufficiently persistent, a contractionary monetary policy shock raises the real rate (and lowers output) but decreases the nominal rate, due to the

decline in inflation and the output gap more than offsetting the direct effect [of the shock].

In the New York Times, Eric Maskin and Amartya Sen explain Condorcet’s

system for electing candidates who truly command majority support. In this system, a voter has the opportunity to rank candidates.

Maskin and Sen’s fictitious example of the American primaries illustrates the difference between a plurality system (as used in the primaries) and a majority system a la Condorcet (where the winner is the one who defeats any other candidate in pairwise comparison). They also point out that

Kenneth Arrow’s famous “impossibility theorem” demonstrates that there is no perfect voting system, and majority rule is no exception. Specifically, as Condorcet himself noted, a majority winner might fail to exist … Such an outcome is quite unlikely in practice, but if it were to arise, a tiebreaking procedure would be needed.

Last year, the IMF has joined the MOOC movement. On edX, the online education platform founded by Harvard University and MIT, the IMF contributes a set of “IMFx” courses developed by its Institute for Capacity Development. Courses cover

The Economist recounts the reasons why the quality of GDP measurement is lacking and why GDP measures cannot answer all the questions they are used to address.

In his blog, John Cochrane points to SoFi, a FinTech company, as proof that banking services can be delivered by institutions without the traditional characteristics of a bank.

SoFi finances loans by selling equity. The loans are securitized and the cash is reinvested in loans. As John points out:

- A “bank” (in the economic, not legal sense) can finance loans, raising money essentially all from equity and no conventional debt. And it can offer competitive borrowing rates — the supposedly too-high “cost of equity” is illusory.

- There is no necessary link between the business of taking and servicing deposits and that of making loans. Banks need not (try to) “transform” maturity or risk.

- To the extent that the bank wants to boost up the risk and return of its equity, it can do so by securitizing loans rather than by borrowing. (Securitized loans are not leverage — there is no promise of your money back when you want it. Investors bear any losses immediately and without recourse.)

- Equity-financed banking can emerge without new regulations, or a big new Policy Initiative. It’s enough to have relief from old regulations (“FDIC-free”).

- Since it makes no fixed-value promises, this structure is essentially run free and can’t cause or contribute to a financial crisis.

In his slides, Charles Wyplosz presents a narrative that emphasizes vulnerabilities and institutional failures.

A conference at the University of Chicago’s Becker Friedman Institute addressed the status of the Fiscal Theory of the Price Level and the theory’s implications for current policy. Slides and papers are available on the conference website. Given that the conference was meant to resuscitate research on the FTPL and that the participants were selected accordingly, many contributions appear rather mainstream.

Chris Sims worries about indeterminacy of the price level if monetary policy is constrained by the ZLB and fiscal policy is passive.

Stephen Williamson argues that it is possible, in a simple model, to separate central bank determination of inflation and the price level from fiscal policy. As he writes on his blog:

The key thing here is that the central bank determines prices and inflation without any fiscal support. If the idea you got from the FTPL is that fiscal policy is necessary to determine the price level and inflation, that’s not correct. …

So, the conclusions are:

- FTPL forces us to think seriously about fiscal/monetary interaction, and that’s very important. But fiscal support is not necessary for monetary policy to work, nor is it useful to think of fiscal policy determining inflation on its own – the central bank can indeed be independent.

- Fiscal/monetary interaction becomes really important when we start thinking about the liquidity properties of government debt.

- Helicopter drops? Forget it. This is not some cure-all for a low-inflation problem.

- QE can be harmful, as it soaks up useful collateral and replaces it with inferior assets.

- Neo-Fisherian denial is not good for you. Central banks that want to increase inflation need to increase nominal interest rates.

John Cochrane argues that to get the cyclical properties of inflation “right” one should focus on the discount factor in the core FTPL equation, not the primary government surplus. The discount factor might also be affected by monetary policy. See also his blog post.

Harald Uhlig remains very skeptical and points to the lack of evidence favoring the FTPL. On his first slide, he asks:

- What does FTPL want to be?

– A theory that can be consistent with the data? OK

– An equation needed to complete a system? OK

– A theoretical or extreme possibility? OK

– A set of predictions, which occasionally work in exotic circumstances (“Brazil”)? PERHAPS

– A set of predictions, which help often (“Taylor coeff < 1”)? ?

– A useful framework for practitioners? ?

– The miracle cure for the failures of other inflation theories? ?

– A framework for the key interplay of fiscal and monetary policy? ?- Where is the “smoking gun”? What set of facts “scream” FTPL? Specific predictions?

- Why is sovereign default off the table? Sure, a central bank can accommodate by inflating away debt … is that all?

- The US, Japan, the Eurozone have a near-deflation problem (is it?). Do you advocate “irresponsible” fiscal policies to solve this?

- What advice would you give the sunspot-branch of macro?

In Taxing the Rich: A History of Fiscal Fairness in the United States and Europe, Kenneth Scheme and David Stasavage

explore the intellectual and political debates surrounding the taxation of the wealthy while also providing the most detailed examination to date of when taxes have been levied against the rich and when they haven’t. Fairness in debates about taxing the rich has depended on different views of what it means to treat people as equals and whether taxing the rich advances or undermines this norm. Scheve and Stasavage argue that governments don’t tax the rich just because inequality is high or rising—they do it when people believe that such taxes compensate for the state unfairly privileging the wealthy. Progressive taxation saw its heyday in the twentieth century, when compensatory arguments for taxing the rich focused on unequal sacrifice in mass warfare. Today, as technology gives rise to wars of more limited mobilization, such arguments are no longer persuasive. [Text from the Publisher’s website.]

Summary by Bryan Caplan:

Democracies have no inherent tendency to “soak the rich.”

Instead, democracies adopt high, progressive taxation in the face of compelling “compensatory” arguments for redistribution.

Only major wars of mass mobilization make compensatory arguments compelling.

Modern military technology has made majors wars of mass mobilization obsolete.

Therefore, tax the rich policies are a thing of the past, at least for developed countries. They won’t be coming back

In the NZZ, Thomas Fuster reports about a consequence of the introduction of new banknotes in Switzerland: Old notes become invalid after a transition period of 20 years.

Nach der Emission des letzten Notenwerts einer neuen Serie kündigt die Schweizerische Nationalbank (SNB) jeweils den Rückruf der alten Serie an. Danach können die Banknoten zwar noch während zwanzig Jahren bei den Kassenstellen oder Agenturen der Nationalbank zum Nennwert umgetauscht werden. In der Folge sind die Noten aber wertlos – oder haben bestenfalls noch Sammlerwert. Eine solche Guillotine fällt das nächste Mal am 30. April 2020. Nach diesem Datum wird die Ende der 1970er Jahre ausgegebene sechste Banknotenserie, von der Ende vergangenen Jahres noch immer 1,14 Mrd. Fr. im Umlauf waren, ihren Geldwert verlieren.

In an earlier post (April 2015) I wrote:

The Economist reports about Nevada shell companies. In its eternal struggle against the Republic of Argentina, Elliott Management is inquiring about several shell companies in the state. They are suspected to own funds that might have been stolen from the Republic. The hedge fund reasons that it is entitled to those funds because they belong to Argentina, and Argentina owes 2 billion dollars to Elliott according to earlier court rulings. Elliott sued in Nevada for information on the shell companies and has been partially successful.

Now, The Economist reports about some unforeseen consequences of the earlier ruling and the “Panama Papers affair”:

Until now, getting information on clients of law firms in Panama has been [difficult]. … But sleuths may soon find it a lot easier, thanks to a court ruling in, of all places, Las Vegas.

In 2014 Elliott, a fund that owned debt on which Argentina had defaulted, sued in Nevada to compel Mossack’s local affiliate to provide information on shell companies, in the hope of discovering Argentine assets to seize. The affiliate, MF Nevada, claimed—implausibly—that it was independent of Mossack. …

A judge in Las Vegas ruled in March 2015 that Mossack and MF Nevada were one and the same. That put a crack in the wall of secrecy around American shell companies. But its full significance is only now becoming apparent: it means that, under an American law about assisting with foreign legal proceedings, any investigator anywhere in the world can subpoena Mossack, through the Nevada subsidiary, for information that could be relevant to cases in any country. …

Faced with the power of American subpoenas, Mossack’s head office will find it much harder to stonewall foreign requests for information. Ignoring them could mean being found in contempt of court. That would leave it open to penalties designed to compel it to comply, including asset seizures, in other countries where it operates.