The average tax wedge in OECD countries has been stable over the last 15 years, at roughly 36 percent. OECD data.

From The Economist, a decomposition in the cross section:

The average tax wedge in OECD countries has been stable over the last 15 years, at roughly 36 percent. OECD data.

From The Economist, a decomposition in the cross section:

In the FAZ, Tim Kanning reports about highly specialized Fintech companies increasingly forming cooperations to better cater to customer needs. Portals rely on services by specialist providers.

A report by Open Europe argues that for the UK the cost of Brexit would be minor. The benefits might be minor as well. For interest groups could make it hard to reap the potential benefits of newly gained flexibility.

… the path to prosperity outside the EU lies through: free trade and opening up to low cost competition, maintaining relatively high immigration (albeit with a different mix of skills), and pushing through deregulation and economic reforms in areas where the UK has historically been sub-par compared to international partners. … whether there is appetite for such changes in the UK is unclear.

… implications for the type of relationship the UK should seek with the EU post-Brexit. Realising the potential economic gains we’ve identified – notably via immigration and deregulation – means a relatively high degree of flexibility from the EU. The confines of a Norwegian or Swiss-style arrangement would not deliver this. As such, the best option would be for the UK to pursue a comprehensive bilateral free trade agreement, aimed at maintaining as much of the current market access as possible while also adopting a broader liberalisation agenda over the longer term.

Update: The Economist reports about other cost/benefit estimates.

In his blog, Ben Bernanke discusses the merits of “helicopter drops” as a monetary policy tool.

[A] “helicopter drop” of money is an expansionary fiscal policy—an increase in public spending or a tax cut—financed by a permanent increase in the money stock.

… the Fed credits the Treasury … in the Treasury’s “checking account” at the central bank, and those funds are used to pay for the new spending and the tax rebate.

… it should influence the economy through a number of channels, making it extremely likely to be effective—even if existing government debt is already high and/or interest rates are zero or negative. … the channels would include:

- the direct effects of the public works spending on GDP, jobs, and income;

- the increase in household income from the rebate, which should induce greater consumer spending;

- a temporary increase in expected inflation, the result of the increase in the money supply. Assuming that nominal interest rates are pinned near zero, higher expected inflation implies lower real interest rates, which in turn should incentivize capital investments and other spending; and

- the fact that, unlike debt-financed fiscal programs, a money-financed program does not increase future tax burdens.

[Debt financed spending programs lack channels 3 and 4.]

[Helicopter drops are subject to various] practical challenges of implementation, including integrating them into operational monetary frameworks and assuring appropriate governance and coordination between the legislature and the central bank.

Key figures from The Panama Papers.

The Economist reviews a new book—“Peak”—by Anders Ericsson and Robert Pool:

Most notable is the “10,000 hour rule”: the idea that anyone can become an expert if they put in the time, a theme popularised by writers like Malcolm Gladwell.

At the heart of Mr Ericsson’s thesis is that there is no such thing as natural ability. Not for Mozart, nor for Garry Kasparov. Traits favourable to a task, such as perfect musical pitch, help at the outset but confer no advantage at higher levels. Rather, after a basic ability, it all comes down to effort.

Such mastery is possible because of what Mr Ericsson calls “deliberate practice”. This is focused training with an expert who can push an individual to a higher understanding of the craft. The key ingredient is mental representations: the ability to perform a task excellently without needing deliberate thought because similar situations have been so well practised that they seem second nature.

A new book on inequality by Branko Milanovic adopts an international perspective. The Economist reviews the book:

Like Mr Piketty, he begins with piles of data assembled over years of research. He sets the trends of different individual countries in a global context. Over the past 30 years the incomes of workers in the middle of the global income distribution—factory workers in China, say—have soared, as has pay for the richest 1% (see chart). At the same time, incomes of the working class in advanced economies have stagnated. This dynamic helped create a global middle class. It also caused global economic inequality to plateau, and perhaps even decline, for the first time since industrialisation began. …

Mr Milanovic suggests that both [Kuznets and Piketty] are mistaken. Across history, he reckons, inequality has tended to flow in cycles: Kuznets waves.

In the FT, Martin Wolf argues that a significant part of the (British) welfare state is about insurance rather than redistribution:

Evidence for this comes from another IFS study … This examined the effects of the tax and benefit systems on people born between 1945 and 1954 …

First, income is far less unequal over lifetimes than in any given year. This is because a big proportion of inequality is temporary … Second, largely as a result, more than half of the redistribution achieved by taxes and benefits is over lifetimes rather than among different people. Third, in the course of adult life, only 7 per cent of individuals receive more in benefits than they pay in taxes, even though 36 per cent of people receive more in benefits than they pay in taxes in any given year. Finally, in-work benefits are just as good as out-of-work benefits at helping people who remain poor throughout their lives but they do less damage to incentives to work. Higher rates of income tax, meanwhile, target the “lifetime rich” relatively well because mobility at the top is relatively modest.

Marcel Fratzscher also wrote a book on the topic, focusing on Germany. He argues that the “Verteilungskampf” (redistributive struggle) intensifies and that equality of opportunity is being lost. In the FAZ, Jan Hauser summarizes a critique of the book by another Berlin based professor, Klaus Schroeder, who argues that the text is very short on substance.

The Economist reports about “outcome switching”—promoting empirical evidence collected in the context of a specific hypothesis test (that didn’t succeed) as support for a different hypothesis.

Outcome switching is a good example of the ways in which science can go wrong. This is a hot topic at the moment, with fields from psychology to cancer research going through a “replication crisis”, in which published results evaporate when people try to duplicate them.

The Economist reports that regulation catches up with peer-to-peer lending:

Meanwhile, a case working its way through the courts may subject P2P loans to state usury laws, from which banks with a national charter are exempt. That would prevent the P2P firms from lending to the riskiest borrowers in much of America. In addition, the Consumer Financial Protection Bureau, a federal agency, announced this month that it would begin accepting complaints about P2P consumer lending.

Rates of delinquency are rising as well.

The Economist reports about initiatives by commercial and central banks that aim at adopting the blockchain technology.

For commercial banks, distributed ledgers promise various advantages—but they also cause problems:

Instead of having to keep track of their assets in separate databases, as financial firms do now, they can share just one. Trades can be settled almost instantly, without the need for lots of intermediaries. As a result, less capital is tied up during a transaction, reducing risk. Such ledgers also make it easier to comply with anti-money-laundering and other regulations, since they provide a record of all past transactions (which is why regulators are so keen on them).

… Yet … [o]ne stumbling block is what geeks call “scalability”: today’s distributed ledgers cannot handle huge numbers of transactions. Another is confidentiality: encryption techniques that allow distributed ledgers to work while keeping trading patterns, say, private are only now being developed. … Such technical hurdles can be overcome only with a high degree of co-operation …

Meanwhile, central banks plan digital currencies built around the same technology.

Like bitcoin, these would be built around a database listing who owns what. Unlike bitcoin’s, though, these “distributed ledgers” would … be tightly controlled by the issuers of the currency.

The plans involve letting individuals and firms open accounts at the central bank …

Central banks … could save on printing costs if people held more bits and fewer banknotes. Digital currency would be tougher to forge, though a successful cyber-attack would be catastrophic. Digital central-bank money could even, in theory, replace cash. …

Better yet, whereas bundles of banknotes can be moved without trace, electronic payments cannot. … The technology first developed to free money from the grip of central bankers may soon be used to tighten their control.

In the Pro Market blog, (previous) industry insiders describe the extent of rent seeking activities in

In his blog, Ben Bernanke discusses the merits of longer-term interest rate targeting as a monetary policy tool.

A lot would depend on the credibility of the Fed’s announcement. If investors do not believe that the Fed will be successful at pushing down the two-year rate … they will immediately sell their securities of two years’ maturity or less to the Fed. … the Fed could end up owning most or all of the eligible securities, with uncertain consequences for interest rates overall. On the other hand, if the Fed’s announcement is fully credible, the prices of eligible securities might move immediately to the targeted levels, and the Fed might achieve its objective without acquiring many securities at all.

… A policy of targeting longer-term rates is related to quantitative easing in that both involve buying potentially large quantities of securities. An important difference is that one sets a quantity and the other sets a price. … Concerns about “losing control of the balance sheet” were a factor behind the Fed’s choice of quantitative easing over rate targets while I was chairman.

Conceivably, QE and rate-pegging could be used together … with QE working through reduced risk premiums while the rate peg operates indirectly by affecting the expected path of short-term interest rates. … The principal limitations of rate pegs are similar to those of forward guidance: Both tools are relatively less effective at affecting interest rates at longer maturities, and even at shorter horizons both must be consistent with a credible or “time-consistent policy” path for short-term interest rates.

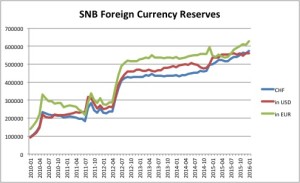

Rising.

Source: SNB. The series “in EUR” is based on the author’s calculations.

Note: The exchange rate floor vis-a-vis the Euro was in place from 6 September 2011 until 15 January 2015.

In a Study Center Gerzensee working paper, Pinar Yesin argues that the IMF’s Equilibrium Real Exchange Rate model (ERER) helps predict medium term exchange rate changes. The reduced form equation relates the real effective exchange rate to macroeconomic fundamentals.

… one of the models, namely the ERER model, outperforms not only the other two in predicting future exchange rate movements, but also the (average) IMF assessment. … the IMF assessments are better at predicting future exchange rate movements in advanced economies than in emerging market economies. Controlling for the exchange rate regime does not yield different results. … the IMF assessments have higher predictive performance in open economies than in closed economies. … safe haven currencies close the misalignment gap predicted by the models faster than other currencies.

… To assess exchange rates only a modified version of the ERER model is being used since 2012. The modified versions of the MB and ES models, while still being utilized, do not have a direct link to the exchange rate anymore. That is, the IMF ceased making a direct link from equilibrium current accounts to equilibrium exchange rates for now.

On VoxEU, representatives of the German Council of Economic Experts outline the German crisis narrative. In disagreement with the ‘consensus view’ outlined in Baldwin et al. (2015) the German economists including Lars Feld, Christoph Schmidt, Isabel Schnabel and Volker Wieland do not want to

implicate the ‘intra-Eurozone capital flows that emerged in the decade before the crisis’ as the ‘real culprits’. … [Rather] it is the government failures and the failures in regulation and supervision leading to those excessive developments that should take centre-stage in the Crisis narrative.

Consequently, their assessment of the policy response to the crisis is positive:

While the alleged consensus summary concludes that ‘the whole situation was made much worse by poor crisis management’, our view is that the ‘loans for reforms’ rationale underlying the rescue approach was not only sensible, since it was the only way to successfully address the underlying causes of the Crisis. It also worked and substantially improved matters.

Sensibly, the writers favor the

objective of retaining the unity of liability and control in all relevant fields of economic policy.

They promote the ‘Maastricht 2.0’ framework proposed earlier by the German Council.

In his blog, John Cochrane discusses plausible features of habit models (that some other models share):

Consumption moves more with income in bad times.

In bad times, consumers start to pay inordinate attention to rare bad states of nature.

[The habit model] also gives a natural account of endogenous time-varying attention to rare events.

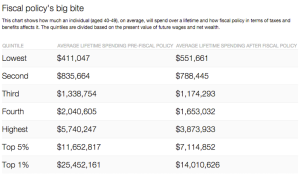

In a New Republic blog, Alan Auerbach and Larry Kotlikoff discuss lifetime spending inequality. Due to taxes and income variability over the life cycle, this is much smaller than wealth or income inequality.

Auerbach and Kotlikoff write:

The top 1 percent of 40-49 year-olds face a net tax, on average, of 45 percent. … For the bottom 20 percent, the average net tax rate is negative 34.2 percent. …

Our standard means of judging whether a household is rich or poor is based on current income. But this classification can produce huge mistakes. … For example, only 68.2 percent of 40-49 year-olds who are actually in the third resource quintile using our data would be so classified based on current income.

The Economist reports about the “ostensibly free online services” provided by Robinhood, a share-trading app.

Instead of taking commissions from customers, Robinhood receives them from the trading venues to which it steers their orders, a controversial but common practice. It also earns returns from the cash clients leave in their accounts, and plans soon to offer margin trading—the buying of stock with borrowed money—for which it will charge a fee.

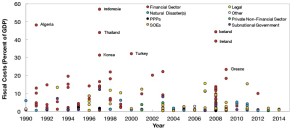

On VoxEU, Elva Bova, Marta Ruiz Arranz, Frederik Toscani and Elif Ture discuss contingent liabilities. Their figure 2 illustrates contingent liability realizations by type and year:

On his blog, Urs Birchler offers different perspectives on the question whether the Swiss National Bank (SNB) is obliged to pay out banks’ reserves in cash.

is a decentralized platform that runs smart contracts: applications that run exactly as programmed without any possibility of downtime, censorship, fraud or third party interference.

These apps run on a custom built blockchain, an enormously powerful shared global infrastructure that can move value around and represent the ownership of property. This enables developers to create markets, store registries of debts or promises, move funds in accordance with instructions given long in the past (like a will or a futures contract) and many other things that have not been invented yet, all without a middle man or counterparty risk.

In his blog, John Cochrane registers disagreement with Larry Summers and reiterates his own argument that in a liquidity trap, interest rate policy does not have a liquidity effect and thus, only a long-run “expected inflation” or “Fisher” effect:

When the liquidity effect is absent, the expected inflation effect is all that remains. Inflation must follow interest rates.

The Economist reports about a US study on shady financial advisors. Over a ten year period, 7% of financial advisors were disciplined for misconduct. Typically, they took a pay cut and moved on to the next firm. A third became repeat offenders. BrokerCheck, run by the US Financial Industry Regulatory Authority, lets you check your local broker.

A report in The Economist confirms what some economists always knew: The findings of laboratory experiments conducted by economists are not very reliable—but much more so than those conducted in medicine, psychology or genetics.

In the FT, John Plender reviews Mervyn King’s “The End of Alchemy: Money, Banking and the Future of the Global Economy.” King diagnoses two problems underlying the crisis. First,

Interest rates today, he says, are too high to permit rapid growth of demand in the short run but too low to be consistent with a proper balance between spending and saving in the long run. The disequilibrium persists, as does a misallocation of capital to unproductive investments.

The second problem relates to the financial system and

the alchemy that runs through the financial system, whereby governments pretend that paper money can be turned into gold on demand and banks pretend that the short-term deposits used to finance long-term investments can be returned whenever depositors want their money back. …

King argues that Bagehot’s famous dictum on central bank crisis management — lend freely on good collateral at penalty rates — is out of date because bank balance sheets today are much larger and have fewer liquid assets than in the 19th century. Central banks are thus condemned in a crisis to take bad collateral in the shape of risky, illiquid assets on which they will lend only a proportion of the value, known as a haircut.

King suggests this lender of last resort role should be replaced by … a pawnbroker for all seasons. In effect, he offers an elegant refinement of the concept of “narrow banking”, which seeks to ensure that all deposits are covered by safe, liquid assets. In his system, banks would decide how much of their asset base to lodge in advance at the central bank to be available for use as collateral. For each asset, the central bank would calculate a haircut to decide how much to lend against it. Together with banks’ cash reserves at the central bank, this collateral would be required to exceed total deposits and short-term borrowings.

This central bankerly pawnbroking would facilitate the supply of liquidity, or emergency money, within a framework that eliminates the incentive for bank runs. It amounts to a form of insurance whereby the central bank can lend in a crisis on terms already agreed and paid for upfront …

The system would displace what King regards as a flawed risk-weighted capital regime ill-suited to addressing radical uncertainty. Today’s liquidity regulation would also become redundant. But banks would still need an equity buffer, with King seeing an equity base of 10 per cent of total assets as “a good start”, against the 3-5 per cent common today.

The current shortfall of fully liquid assets against deposits — the alchemical gap — could be eliminated progressively over 20 years, during which time the expectation would grow that banks would no longer be bailed out. The system would apply to all financial intermediaries …

Update: The Economist‘s reviewer writes:

… Lord King wants banks to buy “liquidity insurance”. In normal times banks would pledge collateral to the central bank, which would agree to lend a certain amount against it, if necessary. Banks would thus know in advance precisely how much help they could get in the event of a meltdown, making them behave responsibly when times were good.