A new report by the Institut für Schweizer Wirtschaftspolitik describes who receives them. Report (in German).

A new report by the Institut für Schweizer Wirtschaftspolitik describes who receives them. Report (in German).

VoxEU, February 5, 2021. HTML.

Based on CEPR DP 15457, I assess possible implications of the introduction of retail CBDC for bank profits. The model implies annual implicit subsidies to U.S. banks of up to 0.8 percent of GDP during the period 1999-2017.

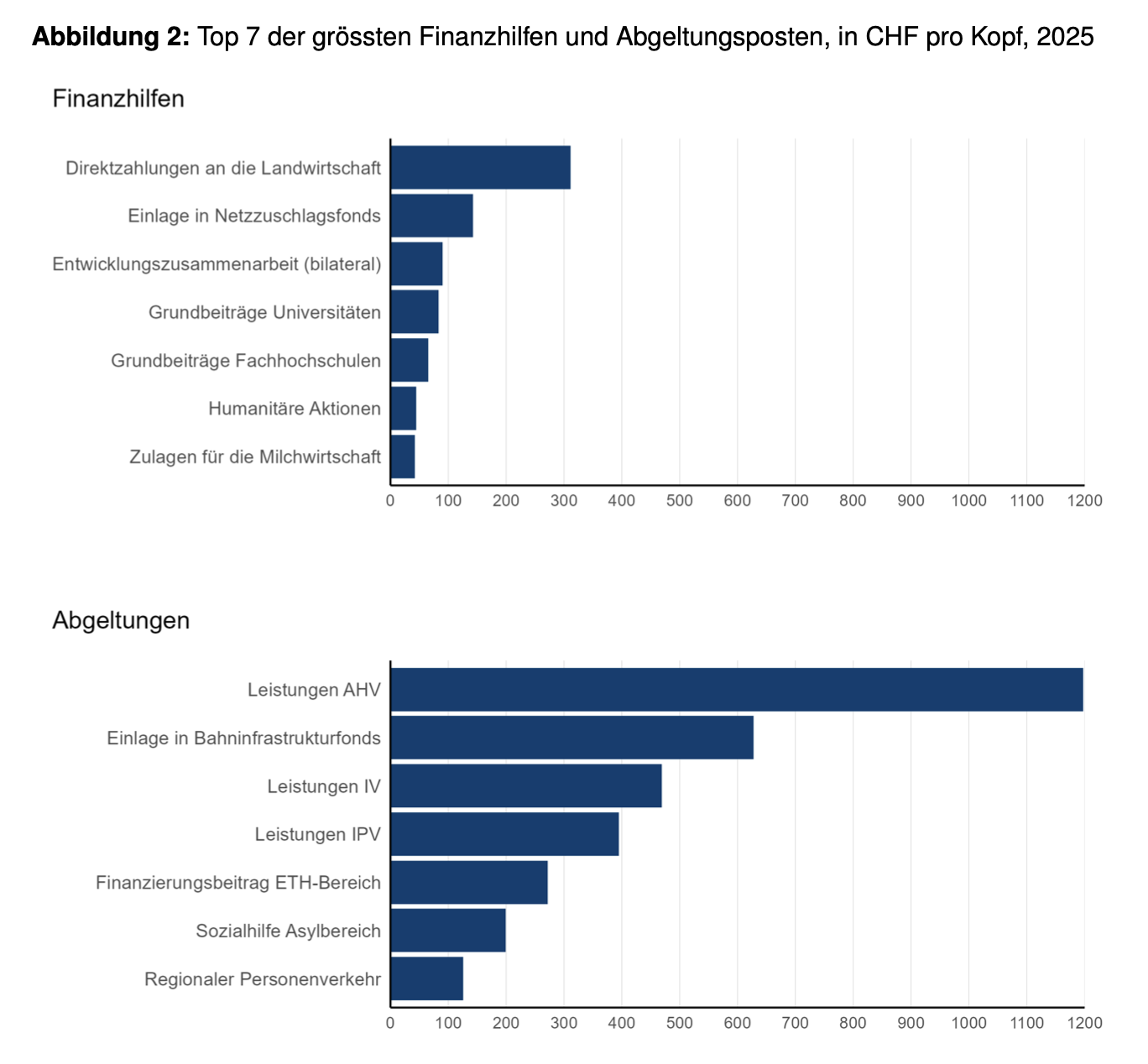

Farmers in Switzerland receive about CHF 2.7 billion in direct financial support annually. Total financial support by the federal and cantonal governments equals more than CHF 4 billion. But according to a report published by Zurich based think tank Avenir Suisse, this financial support constitutes just a minor part of the transfers from society at large to farmers, due to explicit and implicit subsidies, privileges, and—most importantly—negative externalities.

A list of privileges compiled by Avenir Suisse.

Avenir Suisse estimates the value added of Swiss agriculture to be hugely negative.

Die heutige Schweizer Landwirtschaft resultiert in einer negativen Wertschöpfung von minus 15,8 Mrd. Fr. pro Jahr. Damit kostet sie uns umgerechnet rund 1,8 Mio. Fr. pro Stunde.

In the NZZ, Nicole Rütti reports.

On VoxEU, Mary Amiti, Emmanuel Farhi, Gita Gopinath, and Oleg Itskhoki discuss a border adjustment tax and its consequences.

… a border adjustment tax … would make export sales deductible from the corporate tax base, while expenditure on imported goods would not be deductible … Therefore, if the border adjustment extends to all imports and exports, it is akin to a combination of a uniform import tariff and an export subsidy on all international trade …

… it would limit the incentives for profit shifting across countries by means of transfer pricing towards lower tax jurisdictions … the border adjustment tax is a destination-based tax, linking the tax jurisdiction to the location of consumption, rather than the location of production.

Under certain circumstances … the border adjustment tax has no effects on economic outcomes … Lerner (1936) symmetry [implies] … that a uniform tariff on all imports is equivalent to a uniform tax of the same magnitude on all exports. As a corollary … a combination of a uniform import tariff and an export subsidy of the same magnitude … [has] no effect on imports, exports and other economic outcomes … results in an increase in the home relative wage and domestic cost of production by the amount of the tariff. … the relative cost of domestic production increases proportionally with the cost of imports, as well as with the subsidy to exports, leaving no relative price affected, nor the real wage. … As a result, tax policies that feature a border adjustment, such as the value added tax (VAT), do not have to systematically promote or demote trade.

Amiti, Farhi, Gopinath, and Itskhoki discuss several conditions for neutrality:

If the conditions for neutrality are met the border adjustment tax generates no international transfer. The fiscal implications depend on the sign of the trade balance. A home country exchange rate appreciation (that keeps relative trade prices and flows unchanged) generates a lump-sum transfer from households to the public sector when households hold net external assets which they use to pay for imports. When households have net external debt and thus, export on net, then the fiscal implications are reversed.

Since the US has currently a negative net foreign asset position, the US must run a cumulative trade surplus in the future. … the overall transfer would be away from the government budget and towards the private sector …

When some gross positions are denominated in domestic currency an appreciation transfers wealth internationally.

Since for the United States, the foreign assets are mostly in foreign currency, while foreign liabilities are almost entirely in dollars, this would generate a massive transfer to the rest of the world and a capital loss for the US of the order of magnitude of 10% of the US annual GDP or more.

US imports and exports are predominantly invoiced in dollars. With sticky pricing a border adjustment tax would raise the relative cost of imported inputs and consumer prices.

US exports … will likely fall together with US imports in the short run, with no clear effect on the trade balance. As trade prices adjust over time, both imports and exports will recover, resulting in a neutral long-run effect of the border adjustment tax on trade.

In December 2016, the Swiss Federal Council concluded that in international comparison, government support for the Swiss agricultural sector is very high. But critics point out that the government report might understate the social cost of government support. In a separate study the lobby group `Vision Landwirtschaft’ had presented estimates according to which the Swiss agricultural sector adds negative value, on the order of 1 billion CHF per year.

NZZ reports by Désirée Föry: February 9, 2017 and April 2, 2017.

The Economist reports about the political economy aspects of America’s semi-nationalized mortgage industry.

In the Journal of Economic Perspectives, Tyler Cowen and Alex Tabarrok question whether NSF funds are allocated efficiently. They write:

First, a key question is not whether NSF funding is justified relative to laissez-faire, but rather, what is the marginal value of NSF funding given already existing government and nongovernment support for economic research? Second, we consider whether NSF funding might more productively be shifted in various directions that remain within the legal and traditional purview of the NSF. Such alternative focuses might include data availability, prizes rather than grants, broader dissemination of economic insights, and more. …

Public goods theory tells us that the National Science Foundation should support activities that are especially hard to support through traditional university, philanthropic, and private-sector sources. This insight suggests a simple test: to the extent that the NSF allocates funds to genuine public goods as opposed to subsidies on the margin, we ought to see a large difference in the kinds of projects the NSF supports compared to what the “market” sector supports. But what stands out from lists of prominent NSF grants … is how similar they look to lists of “good” research produced by today’s status quo.

In the NZZ,