Wirtschaft Regional, January 7, 2022. PDF.

Interview on private and public money, digital payments, Bitcoin, cash.

Wirtschaft Regional, January 7, 2022. PDF.

Interview on private and public money, digital payments, Bitcoin, cash.

Swissinfo, December 14, 2020. HTML, podcast.

We talk about CBDC, the Swiss National Bank, whether CBDC would render it easier to implement helicopter drops, and how central bank profits should be distributed.

On Coin Center’s blog, Matthew Green and Peter van Valkenburgh write:

Censorship resistance is the only way to guarantee that a digital asset truly is “bearer” and can be sent directly from one person to another without reliance on a third party. Cryptocurrencies achieve this property by making network participants (miners) compete for the power to add transactions to the ledger. Even if some miners wish to censor a transaction, we assume that others will not, particularly if it means they are forgoing fee revenue. A centralized digital dollar would not have competitive mining but if the role of the ledger-keeper was reduced to verifying zero-knowledge proofs then any refusal to perform that verification risks indiscriminately censoring users throughout the economy. If the Treasury became corrupt, it could degrade the performance of the network system-wide, but it would be difficult to selectively block certain individuals or surveil their activities.

None of these protections, however, are guaranteed, and new technologies always present unpredictable risks and unintended consequences. We must, therefore, preserve and defend physical cash and should never celebrate its demise. Cash, along with cryptocurrencies, is essential as a payment method of last resort that cannot be surveilled or controlled by corrupt governments or unscrupulous corporations.

The Central Bank of the Bahamas introduces CBDC, according to a press release (December 2019).

The intended outcome of Project Sand Dollar is that all residents in The Bahamas would have use of a central bank digital currency, on a modernized technology platform, with an experience and convenience—legally and otherwise—that resembles cash. It is expected that this will allow for reduced service delivery costs, increased transactional efficiency, and an improved overall level of financial inclusion. The anonymity feature of cash is not being replicated, although the Sand Dollar infrastructure would incorporate strict attention to confidentiality and data protection.

In the FT, Benjamin Parkin reports about the transformation of India’s payments landscape.

Behind the boom is an innovation launched by the Indian government in 2016: the unglamorous sounding Unified Payments Interface, or UPI, which allows immediate mobile payments directly between bank accounts.

Conceived as a public utility, the service is transforming India’s cash-dependent economy into fertile soil for mobile-money apps. … Both the volume and value of transactions had more than doubled in a year.

On swissinfo.ch, Fabio Canetg explains how the Swiss National Bank prevents banks from hoarding cash rather than holding reserves at the central bank (which pay negative interest). He points to the following sentence in the SNB’s December 2014 press release (my emphasis) and he speculates that banks could, in principle, implement similar schemes to keep depositors from withdrawing cash:

The threshold currently corresponds to 20 times the minimum reserve requirement for the reporting period 20 October 2014 to 19 November 2014 (static component), minus any increase/plus any decrease in the amount of cash held (dynamic component). The change in the amount of cash held is calculated as the difference between the average cash holdings during the most recent reporting period for which the minimum reserve requirement is determined prior to the reference date (cf. section 5 below) and the cash holdings of the corresponding reporting period in a given reference period.

On his blog, JP Koning argues that very short conversion periods rendered it unattractive for Swedes to hold cash. He also suggests that it were the banks that pushed for the short periods.

While digital payments share some of the blame for the obsolescence of paper kronor, the Riksbank is also responsible. The Riksbank betrayed the Swedish cash-using public this decade by embarking on an aggressive note switch. Had it chosen a more customer friendly approach, Swedes would be holding a much larger stock of banknotes than they are now. As long as other countries don’t enact the same policies as Sweden, they needn’t worry about precipitous declines in cash demand.

Recently, the trend decline of kronor cash holdings has reverted. Across the board, the use case for cash seems to change (see also this post).

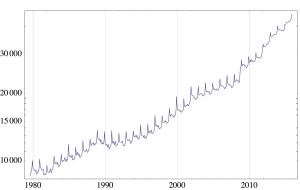

… even as developed countries are seeing fewer transactions completed using cash, the quantity of banknotes outstanding has jumped. This increase in cash outstanding, which generally exceeds GDP growth, is mostly due to an increase in demand for large-value denominations, as the chart below illustrates:

On his blog, JP Koning reports that

[b]oth the Christmas bump and the sawtooth pattern arising from monthly payrolls are less noticeable than previous years. But these patterns remain more apparent for Canadian dollars than U.S. dollars. Not because Canadians like cash more than Americans. We don’t, and are probably further along the path towards digital payments then they are. Rather, the percentage of U.S. dollars held overseas is much larger than Canadian dollars, so domestic usage of U.S. cash for transactions purposes gets blurred by all its other uses.

In the FAZ, Philip Plickert reports that Deutsche Bundesbank changed its terms of business. Starting August 25, the Bundesbank may refuse cash transactions with a bank if the Bundesbank fears that, counter to the bank’s assurances, the cash transaction might help the bank or its customers evade sanctions or restrictions with the aim to impede money laundering or terrorism finance.

Conveniently, this will allow the Bundesbank to reject a request by European-Iranian Handelsbank to withdraw several hundred Euros.

Die staatliche Europäisch-Iranische Handelsbank (EIHB) in Hamburg hatte Anfang Juli bei der Bundesbank beantragt, mehr als 300 Millionen Euro in bar abzuheben. Nach Informationen der F.A.Z. war sogar von 350 bis 380 Millionen Euro die Rede. Dem Vernehmen nach soll es sich um Guthaben der iranischen Zentralbank bei der EIHB handeln. … Derzeit prüft die Finanzaufsicht Bafin, ob die EIHB die Vorschriften zur Prävention von Geldwäsche und Terrorfinanzierung einhält. Diese Prüfung könne sich hinziehen, heißt es in Berlin aus dem Finanzministerium. Bis die Bafin ihr Urteil abgibt, dürften die geänderten AGB der Bundesbank greifen.

The US has pressured the German government to prevent the cash withdrawal. And the Bundesbank closely cooperates with the Federal Reserve.

In ihren geänderten Geschäftsbedingungen ist explizit die Rede davon, dass auch die „drohende Beendigung von wichtigen Beziehungen zu Zentralbanken und Finanzinstitutionen dritter Länder“ ein Ablehnungsgrund für Bargeldgeschäfte sein könne.

In July, JP Koning had blogged about the bank’s request. His conclusion was:

There are sound political and moral reasons for both censoring Iran and not censoring it. Moral or not, my guess is that most nations will breathe a sigh of relief if German authorities see it fit to let the €300 million cash withdrawal go through. It would be a sign to all of us that we don’t live in a unipolar monetary world where a single American censor can prevent entire nations from making the most basic of cross-border payments. Instead, we’d be living in a bipolar monetary world where censorship needn’t mean being completely cutoff from the global payments system.

The sooner the Bundesbank prints up and dispatches the €300 million, the better for us all.

In an earlier column, Koning had described the difficulties for financial institutions worldwide to circumvent U.S. financial sanctions.

Kontantupproret (“cash rebellion”) in Sweden—not everybody is pleased with the prospect of a cashless society.

David Crouch reports in The Guardian.

On VoxEU, Clemens Jobst and Helmut Stix argue that

… cash balances for transactions comprise only a modest share of overall cash demand (a rough estimate of 15% might be a good guess across richer economies). … changes in currency in circulation are dominated by motives like hoarding. While transaction demand is reasonably well researched … still too little is known about non-transaction demand in general, and recent increases in particular.

On his blog, JP Koning offers two explanations for the surprisingly high rupee notes redemption rate—nearly 99%—after last year’s demonetization experiment: Money laundering, and a partial amnesty.

Indians who had large quantities of illicit cash were able to contract with those who had room below their ceiling to convert illicit rupees on their behalf …

Two weeks after the initial … announcement, the government introduced a formal amnesty for demonetized banknote holders. Any deposit of cash above the ceiling would only be taxed at 50%, assuming it was declared. If not declared, the funds might still get through the note blockade undetected, although if apprehended an 85% penalty was to be levied. These new options were better than throwing away one’s stash altogether and suffering a sure 100% loss …

As a consequence, the windfall for the government likely was smaller than expected. But poorer Indians may still have benefited, by selling their services in the money laundering scheme.

In the FT, Sam Fleming and Demetri Sevastopulo report that the White House considers Marvin Goodfriend for the Federal Reserve’s Board of Governors.

He has criticised the Fed’s crisis-era balance sheet expansion, saying the central bank should generally not purchase mortgage-backed securities, and has advocated the use of monetary policy rules to guide policy, as has Mr Quarles. …

At the same time, however, Mr Goodfriend has been willing to contemplate the use of deeply negative rates to stimulate growth — something that the Fed has thus far not embarked upon. In 1999 he wrote that negative rates were a feasible option, years before central banks started actually experimenting with them.

To implement negative rates while preserving cash, Goodfriend has advocated a flexible exchange rate between deposits and cash. On Alphaville, Matthew Klein quotes from a recent paper of Goodfriend’s:

The zero bound encumbrance on interest rate policy could be eliminated completely and expeditiously by discontinuing the central bank defense of the par deposit price of paper currency. … the central bank would no longer let the outstanding stock of paper currency vary elastically to accommodate the deposit demand for paper currency at par. …

The reason to abandon the pegged par deposit price of paper currency is analogous to the … reasons for abandoning the gold standard and fixed exchange rate: it is to let fluctuations in the deposit demand for paper currency be reflected in the deposit price of paper currency so as not to destabilize the general price level … the flexible deposit price of paper currency would behave as it actually did when the payment of paper currency for deposits was restricted in the United States during the banking crises of 1873, 1893, and 1907.

On his blog, JP Koning provides an account of recent monetary policy in Zimbabwe:

On his blog, JP Koning discusses the case of Somalia which has managed without central bank issued money for decades.

Old, legitimate notes and newer, counterfeit notes trade at the same price which equals the cost of producing counterfeits.

See also this previous post.

On Moneyness, JP Koning argues that India’s demonetization experiment could have proceeded more smoothly if bank notes had been overstamped rather than immediately withdrawn.

On Alt-M, Larry White discusses three aspects of the Indian “demonetization” experiment.

The transition from old notes blocks “honest” currency transactions, reduces income, and harms the poor who don’t have access to alternative means of payment. Because not all old notes will be redeemed, the transition into new notes will generate seignorage revenue for the government on the order of USD 40 billion, according to White’s estimates. Not all groups or industries get access to the new notes at the same time; this changes the terms of trade (Cantillon effects).

India follows suggestions to fight tax evasion by taking high denomination notes out of circulation … and introducing new ones. Until the end of the year, Indians may exchange the old banknotes against new ones, at banks or post offices, by identifying themselves. On his blog, J P Koning discusses earlier demonetization episodes in Iraq and Sweden.

India’s move does not exactly follow the well publicized suggestions currently debated. But it might work.

On his blog, J P Koning discusses Kenneth Rogoff’s proposal to abolish high denomination notes (discussed earlier). Koning concludes:

I agree with Rogoff’s general point that it makes sense to burden cash users with ever more work since this burden disproportionately falls on heavy users like criminals. But Rogoff hasn’t yet convinced me that the status quo policy of gradually increasing the workload involved in cash usage (via inflation) needs to be sped up by a sudden removal of every bill above the $10. After all, the Swedes are setting an example of how a policy of gradualism can be twinned with tax policy in order to get some of the very effects that Rogoff advocates, namely pulling people out of the underground economy into the legal economy.

Koning refers to Martin Enlund’s post on the Nordea blog; Enlund suggests that decreased cash demand in Sweden may partly be due to policy reforms that rendered tax evasion less attractive.

Figure from Enlund blog:

On his blog, Ben Bernanke discusses the merits of the Fed’s strategy to slowly reduce the size of its balance sheet to pre crisis levels. Bernanke (with reference to a paper by Robin Greenwood, Samuel Hanson and Jeremy Stein) suggests that this strategy should be reconsidered:

First, the large balance sheet provides lots of safe and liquid assets for financial markets. This might strengthen financial stability. (DN: In my view, there are also reasons to expect the opposite.)

Second, a larger balance sheet can help improve the workings of the monetary transmission mechanism, in particular if non-banks can deposit funds at the Fed. Currently, the Fed accepts funds from private-sector institutional lenders such as money market funds, through the overnight reverse repurchase program (RRP). (DN: I agree. As I have argued elsewhere, access to central bank balance sheets should be broadened.)

Third, with a large balance sheet and thus, large bank reserve holdings to start with, it could be easier to avoid “stigma” in the next financial crisis when banks need to borrow cash from the Fed but prefer not to in order not to signal weakness. (DN: Like the first, this third argument emphasizes banks’ needs. In my view, monetary policy should not emphasize these needs too much because it is far from clear whether bank incentives are sufficiently aligned with the interests of society at large.)

Bernanke also discusses the reasons why the Fed does want to reduce the balance sheet size.

First, in a financial panic, programs like the RRP could result in market participants depositing more and more funds at the Fed until the interbank market would be drained of liquidity. But these programs could be capped.

Second, a large balance sheet increases the risk of large fiscal losses for the Fed and thus, the public sector. Losses could trigger a legislative response and undermine the Fed’s policy independence. But these risks could be kept in check if the Fed invested in government paper that constitutes a close substitute to cash, such as three year government debt. (DN: But why, then, shouldn’t financial market participants hold three year government debt rather than reserves at the Fed? Because cash is much more liquid than government debt … But what does this mean?)

The Economist reports about initiatives by commercial and central banks that aim at adopting the blockchain technology.

For commercial banks, distributed ledgers promise various advantages—but they also cause problems:

Instead of having to keep track of their assets in separate databases, as financial firms do now, they can share just one. Trades can be settled almost instantly, without the need for lots of intermediaries. As a result, less capital is tied up during a transaction, reducing risk. Such ledgers also make it easier to comply with anti-money-laundering and other regulations, since they provide a record of all past transactions (which is why regulators are so keen on them).

… Yet … [o]ne stumbling block is what geeks call “scalability”: today’s distributed ledgers cannot handle huge numbers of transactions. Another is confidentiality: encryption techniques that allow distributed ledgers to work while keeping trading patterns, say, private are only now being developed. … Such technical hurdles can be overcome only with a high degree of co-operation …

Meanwhile, central banks plan digital currencies built around the same technology.

Like bitcoin, these would be built around a database listing who owns what. Unlike bitcoin’s, though, these “distributed ledgers” would … be tightly controlled by the issuers of the currency.

The plans involve letting individuals and firms open accounts at the central bank …

Central banks … could save on printing costs if people held more bits and fewer banknotes. Digital currency would be tougher to forge, though a successful cyber-attack would be catastrophic. Digital central-bank money could even, in theory, replace cash. …

Better yet, whereas bundles of banknotes can be moved without trace, electronic payments cannot. … The technology first developed to free money from the grip of central bankers may soon be used to tighten their control.

On his blog, Urs Birchler offers different perspectives on the question whether the Swiss National Bank (SNB) is obliged to pay out banks’ reserves in cash.

In a blog post, Gilles Saint-Paul describes how organized crime exploits the arbitrage opportunities that (bad) regulation creates.

He predicts that eliminating cash transactions by decree, along the lines of policy proposals currently en vogue, will lead organized crime to establish alternative, sound mediums of exchange that the general public might adopt.

In a Vox column, Jeremy Bulow and Ken Rogoff argue that perceptions of Greek net debt repayments over the last years are wrong.

[C]ontrary to widespread popular opinion, the net flow of funds (new loans and subsidies minus repayments) went from the Troika to Greece from 2010 to mid-2014, with a modest flow in the other direction after Greece stalled on its structural reforms.

They also make some other points: