Discussion at the 2020 Bank of Canada Annual Economic Conference: The Future of Money and Payments: Implications for Central Banking. PDF.

Tag Archives: Currency

“Public versus Private Digital Money: Macroeconomic (Ir)relevance,” VoxEU, 2019

VoxEU, March 20, 2019, with Markus Brunnermeier. HTML.

Both proponents and opponents have suggested that CBDC would fundamentally change the macroeconomy, either for the better or the worse. We question this paradigm. We derive an equivalence result according to which the introduction of CBDC need not alter the allocation nor the price system. And we argue that key concerns put forward in discussions about CBDC are misplaced.

See also our VoxEU book chapter and my paper from last year.

“Central Bank Digital Currency: What Difference Does It Make?,” SUERF, 2018

December 2018. PDF. In: Ernest Gnan and Donato Masciandaro, editors, Do We Need Central Bank Digital Currency? Economics, Technology and Institutions, SUERF, The European Money and Finance Forum, Vienna, 2018.

A short version of the CEPR working paper.

“Central Bank Digital Currency: Why It Matters and Why Not,” VoxEU, 2018

VoxEU, August 20, 2018. HTML.

- To a first approximation, inside and outside money are substitutes—the introduction of CBDC does not change the equilibrium allocation.

- Bank incentives and central bank incentives might be affected though.

- CBDC could increase the incentive to extend credit but might undermine the political support for implicit financial assistance to banks.

Currency Status

On his blog (here and here), JP Koning discusses currency status:

… laws that … grant … currency status. … Say that person A is carrying some sort of financial instrument in their pocket and it is stolen. The thief uses it to buy something from person B, who accepts it without knowing it to be stolen property. If the financial instrument has not been granted currency status by the law, then person B will be liable to give it back to person A. If, however, the instrument is currency, then even if the police are able to locate the stolen instrument in person B’s possession, person B does not have to give up the stolen [instrument] to person A. We call these special instruments negotiable instruments.

Marvin Goodfriend, the Fed’s Board of Governors, and Negative Rates

In the FT, Sam Fleming and Demetri Sevastopulo report that the White House considers Marvin Goodfriend for the Federal Reserve’s Board of Governors.

He has criticised the Fed’s crisis-era balance sheet expansion, saying the central bank should generally not purchase mortgage-backed securities, and has advocated the use of monetary policy rules to guide policy, as has Mr Quarles. …

At the same time, however, Mr Goodfriend has been willing to contemplate the use of deeply negative rates to stimulate growth — something that the Fed has thus far not embarked upon. In 1999 he wrote that negative rates were a feasible option, years before central banks started actually experimenting with them.

To implement negative rates while preserving cash, Goodfriend has advocated a flexible exchange rate between deposits and cash. On Alphaville, Matthew Klein quotes from a recent paper of Goodfriend’s:

The zero bound encumbrance on interest rate policy could be eliminated completely and expeditiously by discontinuing the central bank defense of the par deposit price of paper currency. … the central bank would no longer let the outstanding stock of paper currency vary elastically to accommodate the deposit demand for paper currency at par. …

The reason to abandon the pegged par deposit price of paper currency is analogous to the … reasons for abandoning the gold standard and fixed exchange rate: it is to let fluctuations in the deposit demand for paper currency be reflected in the deposit price of paper currency so as not to destabilize the general price level … the flexible deposit price of paper currency would behave as it actually did when the payment of paper currency for deposits was restricted in the United States during the banking crises of 1873, 1893, and 1907.

“Kosten eines Vollgeld-Systems sind hoch (Costly Sovereign Money),” Die Volkswirtschaft, 2016

“Wer hat Angst vor Blockchain? (Who’s Afraid of the Blockchain?),” NZZ, 2016

NZZ, November 29, 2016. HTML, PDF. Longer version published on Ökonomenstimme, December 14, 2016. HTML.

Central banks are increasingly interested in employing blockchain technologies, and they should be.

- The blockchain threatens the intermediation business.

- Central banks encounter the blockchain in the form of new krypto currencies, and as the technology underlying new clearing and settlement systems.

- Krypto currencies bear the risk of “dollarization,” but in the major currency areas this risk is still small.

- New clearing and settlement systems benefit from central bank participation. But central banks benefit as well; those rejecting the new technology risk undermining the attractiveness of the home currency.

Bundesbank Considers Electronic Money

eKrona

In the FT, Richard Milne reports about the Riksbank pondering to issue a digital currency.

There are considerable questions for Sweden’s central bank to answer about how a digital currency would work. Would individuals have an account at the Riksbank? Would transactions be traceable, unlike with cash? Would emoney earn interest?

Ms Skingsley said: “Personally I would like to design it in a way that is most like notes and coins.” That would mean no interest would be paid on it. But she added that the state had no interest in helping illegal activity, suggesting some form of traceability.

The Riksbank would also need to consider financial stability issues such as whether they would or should compete with commercial banks’ deposit base. Ms Skingsley said she was concerned that in times of financial instability citizens could transfer money to a state-backed electronic system, potentially increasing instability.

“Central Banking and Bitcoin: Not yet a Threat,” VoxEU, 2016

VoxEU, October 19, 2016. HTML.

- Central banks are increasingly interested in employing blockchain technologies.

- The blockchain threatens the intermediation business.

- Central banks encounter the blockchain in the form of new krypto currencies, and as the technology underlying new clearing and settlement systems.

- Krypto currencies bear the risk of “dollarization,” but in the major currency areas this risk is still small.

- New clearing and settlement systems benefit from central bank participation. But central banks benefit as well; those rejecting the new technology risk undermining the attractiveness of the home currency.

- See the original blogpost.

How Does the Blockchain Transform Central Banking?

The blockchain technology opens up new possibilities for financial market participants. It allows to get rid of middle men and thus, to save cost, speed up clearing and settlement (possibly lowering capital requirements), protect privacy, avoid operational risks and improve the bargaining position of customers.

Internet based technologies have rendered it cheap to collect information and to network. This lies at the foundation of business models in the “sharing economy.” It also lets fintech companies seize intermediation business from banks and degrade them to utilities, now that the financial crisis has severely damaged banks’ reputation. But both fintech and sharing-economy companies continue to manage information centrally.

The blockchain technology undermines the middle-men business model. It renders cheating in transactions much harder and thereby reduces the value of credibility lent by middle men. The fact that counter parties do not know and trust each other becomes less of an impediment to trade.

The blockchain may lend credibility to a plethora of transactions, including payments denominated in traditional fiat monies like the US dollar or virtual krypto currencies like Bitcoin. An advantage of krypto currencies over traditional currencies concerns the commitment power lent by “smart contracts.” Unlike the money supply of fiat monies that hinges on discretionary decisions by monetary policy makers, the supply of krypto currencies can in principle be insulated against human interference ex post and at the same time conditioned on arbitrary verifiable outcomes (if done properly). This opens the way for resolving commitment problems in monetary economics. (Currently, however, most krypto currencies do not exploit this opportunity; they allow ex post interference by a “monetary policy committee.”) A disadvantage of krypto currencies concerns their limited liquidity and thus, exchange rate variability relative to traditional currencies if only few transactions are conducted using the krypto currency.

Whether blockchain payments are denominated in traditional fiat monies or krypto currencies, they are always of relevance for central banks. Transactions denominated in a krypto currency affect the central bank in similar ways as US dollar transactions, say, affect the monetary authority in a dollarized economy: The central bank looses control over the money supply, and its power to intervene as lender of last resort may be diminished as well. The underlying causes for the crowding out of the legal tender also are familiar from dollarization episodes: Loss of trust in the central bank and the stability of the legal tender, or a desire of the transacting parties to hide their identity if the central bank can monitor payments in the domestic currency but not otherwise.

Blockchain facilitated transactions denominated in domestic currency have the potential to affect central bank operations much more directly. To leverage the efficiency of domestic currency denominated blockchain transactions between financial institutions it is in the interest of banks to have the central bank on board: The domestic currency denominated krypto currency should ideally be base money or a perfect substitute to it, directly exchangeable against central bank reserves. For when perfect substitutability is not guaranteed then the payment associated with the transaction eventually requires clearing through the traditional central bank managed clearing mechanism and as a consequence, the gain in speed and efficiency is relinquished. Of course, building an interface between the blockchain and the central bank’s clearing system could constitute a first step towards completely dismantling the latter and shifting all central bank managed clearing to the former.

Why would central banks want to join forces? If they don’t, they risk being cut out from transactions denominated in domestic currency and to end up monitoring only a fraction of the clearing between market participants. Central banks are under pressure to keep “their” currencies attractive. For the same reason (as well as for others), I propose “Reserves for All”—letting the general public and not only banks access central bank reserves (here, here, here, and here).

Blockchains in Banking (Commercial and Central)

The Economist reports about initiatives by commercial and central banks that aim at adopting the blockchain technology.

For commercial banks, distributed ledgers promise various advantages—but they also cause problems:

Instead of having to keep track of their assets in separate databases, as financial firms do now, they can share just one. Trades can be settled almost instantly, without the need for lots of intermediaries. As a result, less capital is tied up during a transaction, reducing risk. Such ledgers also make it easier to comply with anti-money-laundering and other regulations, since they provide a record of all past transactions (which is why regulators are so keen on them).

… Yet … [o]ne stumbling block is what geeks call “scalability”: today’s distributed ledgers cannot handle huge numbers of transactions. Another is confidentiality: encryption techniques that allow distributed ledgers to work while keeping trading patterns, say, private are only now being developed. … Such technical hurdles can be overcome only with a high degree of co-operation …

Meanwhile, central banks plan digital currencies built around the same technology.

Like bitcoin, these would be built around a database listing who owns what. Unlike bitcoin’s, though, these “distributed ledgers” would … be tightly controlled by the issuers of the currency.

The plans involve letting individuals and firms open accounts at the central bank …

Central banks … could save on printing costs if people held more bits and fewer banknotes. Digital currency would be tougher to forge, though a successful cyber-attack would be catastrophic. Digital central-bank money could even, in theory, replace cash. …

Better yet, whereas bundles of banknotes can be moved without trace, electronic payments cannot. … The technology first developed to free money from the grip of central bankers may soon be used to tighten their control.

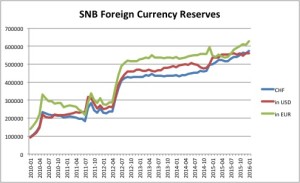

SNB Foreign Currency Reserves

Rising.

Source: SNB. The series “in EUR” is based on the author’s calculations.

Note: The exchange rate floor vis-a-vis the Euro was in place from 6 September 2011 until 15 January 2015.

Reserves for Everyone—Towards a New Monetary Regime?

In the first and third of his Munich Lectures in Economics (and in an earlier oped in the FT), Kenneth Rogoff argued in favour of phasing out cash, at least high denominations and in some developed economies, see my post. Rogoff emphasised two beneficial consequences. First, the abolition of the zero lower bound on nominal interest rates and thus, the relaxation of a constraint on monetary policy. And second, the abolition of a means of payment that guarantees anonymity and thus, facilitates criminal transactions, money laundering, tax evasion and the like.

Both Rogoff and other academics have discussed the topic before. More than in academic papers, the end of cash has been the subject of intense debate in the blogosphere. By far the clearest discussion I know (and a very comprehensive one) is due to Willem Buiter in a blog post I summarise here. But the list of authors that have contributed to the discussion is much longer. Here is a selective overview:

- As far as solutions to the zero lower bound problem are concerned, Buiter in his post referred to several academic contributions, namely Eisler (1932), Goodfriend (2000), Buiter and Panigirtzoglou (2001, 2003), Davies (2004) and Buiter (2004, 2007). Rogoff in his lectures referred to Silvio Gesell as well as writers in the blogosphere including Mankiw, Buiter and Kimball.

- Concerning the loss of tax revenue due to anonymous currency holdings, Rogoff referred to his own earlier work (Rogoff 1998).

- On April 19, 2009, Gregory Mankiw discussed the zero lower bound in the New York Times. He reported a proposal by a graduate student to relax the bound by taxing currency: The Fed should announce that all notes whose serial number ends in a particular digit would cease to be legal tender within a certain time period; and the digit should be determined by a lottery. (According to Buiter, Charles Goodhart made the same proposal earlier.)

- On May 7 and 19, 2009, Willem Buiter strongly argued in favour of negative nominal interest rates in his FT maverecon blog (see my post). He identified currency’s status as a bearer security as the cause of the zero lower bound and discussed three strategies to relax the bound: Abolishing currency; taxing it (difficult); and separating the medium-of-exchange role of money from the unit-of-account function by creating a unit of account dollar (think of reserves) on the one hand and a medium of exchange dollar (think of currency) on the other. The former would pay positive or negative interest, the latter would pay no interest. Both would trade at an exchange rate, and interest parity conditions would hold in equilibrium.

- Other FT bloggers took up Buiter’s proposal. An early post, on May 20, 2009, is due to Izabella Kaminska in FT Alphaville.

- On April 19, 2012, Matthew Yglesias argued in Slate that the abolition of the zero lower bound would facilitate expectations formation about monetary policy.

- On November 5, 2012, Miles Kimball took up the issue in a blog post. In another post, he discussed Marvin Goodfriend’s (2000) contribution to the debate.

- On April 15, 2013, Izabella Kaminska suggested in FT Alphaville that direct access of consumers and investors to government provided electronic money would allow central banks to bypass commercial banks, improve the monetary transmission mechanism and help end a shortage of safe assets.

- On April 16, 2013, Jean-François Groff argued in FT Alphaville that electronic money should be provided by the government instead of private companies (“digital legal tender”). Governments then could (re-)gain seignorage and consumers would benefit from lower fees and user costs.

- On July 27, 2014, John Cochrane discussed Sheila Bair’s opposition against letting the broader public hold reserves. On August 21, September 17 and September 22, 2014, he approvingly discussed (here, here and here) the Fed’s balance sheet policy from a financial stability/narrow banking perspective (see my post on narrow banking proposals). On November 21, 2014, he interpreted minutes of an FMOC meeting as suggestive evidence of plans to establish segregated cash accounts.

When evaluating the merit of these discussions, it is important to distinguish between (i) introducing government provided electronic money and (ii) doing so in combination with an abolition of currency. Consider first the former option, namely to have the government grant the broad access to central bank reserves. This could be useful as it opened up the possibility to eliminate the risk of bank runs and as a consequence, abolish the fragile and costly system of deposit “insurance.” If, that is, most savers opted to move their deposits to the central bank rather than keeping them with commercial banks. If they didn’t, then governments would most likely feel obliged to continue bailing out depositors in failing commercial banks.

Another advantage of introducing government provided electronic money would be to eliminate a disgraceful contradiction in public policy. Mostly for reasons related to the deterrence of tax evasion, governments increasingly force citizens to use electronic means of payment although these are not legal tender and declare the use of currency illegal although currency is legal tender. In effect, governments force citizens to use liabilities of private companies for their transactions and in doing so, expose citizens to various financial risks. (These risks are partly borne by the public sector, due to deposit insurance, but that insurance creates other problems.) This absurd situation would end if the government provided a legal tender for electronic payments.

But granting the public access to central bank reserves could also create new problems. Inducing savers to move their deposits from commercial banks to the central bank would undermine a central activity of the former, namely deposit financed credit creation. Douglas Diamond and Philip Dybvig (1983) have shown in a classic article that the insurance characteristics of a deposit contract help improve outcomes relative to a situation without such a contract. How large are those benefits? And how large are they relative to the social costs of bank deposits, namely inefficiencies due to deposit insurance (moral hazard) and costs of run-induced fire sales and defaults?

There are other open questions. One concerns the transition from the current system where savers hold deposits at commercial banks, to a new system where they hold central bank reserves. Would the central bank assist commercial banks and convert deposits into reserve holdings? And if not, how could runs be avoided?

In addition, questions of a more technical nature would have to be addressed. Should banks (in the interbank market of reserves) and the general public (when paying their bills) use the same payment system? Or should the existing system linking the central bank and commercial banks be kept separate from a new, to be designed, system that serves consumers? How would monetary policy in this new world look like and how would the monetary transmission mechanism work? Would the central bank lend funds to households, and would it set the same policy rates for banks and the general public?

Turn next to the more ambitious proposal, namely to augment the introduction of government provided electronic money with an abolition of currency. This suggestion is more problematic, because the promised benefits are likely overstated and the costs misjudged. Consider first the benefits. As far as the relaxation of the zero lower bound is concerned, the fundamental objective—to lower real interest rates in order to incentivise earlier consumption and investment—cannot only be achieved through monetary policy but also by tax policy. A trend increase in consumption or value added tax rates acts like a low or negative real interest rate. And even if the objective is to relax constraints on monetary policy rather than relying on fiscal policy, this is feasible without eliminating cash altogether (and without moving to a higher inflation target which is costly for other reasons). As explained by Buiter, all that is needed is a floating exchange rate between reserves and cash. Killing currency amounts to an overkill unless one fears negative consequences due to such a floating exchange rate (see, e.g., Goodfriend, 2009, fn. 23).

As far as the second objective—limiting tax evasion as well as criminal and black economy transactions—is concerned, the elimination of currency is not a sufficient measure. True, those seeking anonymity would need to incur additional costs to secure it. But these additional costs would likely be mostly fixed costs (e.g., fees for incorporating a shell company in Nevada and hiring a lawyer). The implicit tax on black market activity due to the abolition of currency thus would be a regressive one and the revenues it generated would likely be smaller than hoped for. Professional criminals directing large operations could easily afford the higher cost of securing anonymity while the tax dodging middle class plumber in a badly run country could not.

Turning to the disadvantages, eliminating currency has severe consequences for privacy. (Buiter’s suggestion of ‘cash-on-a-chip cards’ could limit those consequences somewhat.) This point is widely acknowledged in the debate but it is not given sufficient weight. Related, forcing savers to hold means of payment—and a significant share of their savings—exclusively with a branch of the government (the central bank) might cause concern, particularly in countries with a history of expropriation.

Finally, there is a completely different reason to be worried about the prospect of putting an end to currency; when pointed to the proposal under question, some mothers I talked to immediately articulated it: In a world without physical money it is harder to acquire basic financial literacy skills. This might appear like a third-order problem, but is it?

Currency, Electronic Money and the Zero Lower Bound

Willem Buiter argues in favour of negative nominal interest rates in his FT maverecon blog. He identifies the bearer security nature of currency (whose owner remains anonymous) as the fundamental cause of the zero lower bound on nominal interest rates and discusses three possible strategies to relax the lower bound.

First, to abolish currency. As a consequence, central bank seignorage might fall and criminals would need to find new stores of value that guarantee anonymity. Limited privacy could be preserved by ‘cash-on-a-chip cards’ and for practicality reasons, small denominations could be kept. The price of the remaining cash expressed in terms of electronic money would fluctuate, however.

Second, to tax currency. Since cash can be held anonymously, this poses difficult incentive problems. It could be done but would be complicated and costly.

Third, to unbundle two functions of money, namely the medium of exchange/means of payment function on the one hand and the numéraire/unit of account function on the other. Suppose that there are two dollars, one unit of account dollar or “dollar” and one medium of exchange dollar or “m-dollar” (Buiter talks of “rallods” rather than m-dollars). Central bank reserves constitute dollars and might pay positive or negative interest while cash constitutes m-dollars and does not pay interest (or at least not negative interest). Monetary policy is conducted as usual by setting interest rates on dollars. In addition, the stock of m-dollars is fixed by the central bank, letting the market determine the exchange rate between dollars and m-dollars; or the central bank fixes an exchange rate between the dollar and m-dollar and elastically supplies m-dollars at this rate. In either case, the exchange rate will typically differ from unity and vary over time, in contrast to the current situation. Zero interest on the m-dollar and non-zero (positive or negative) interest on the dollar are consistent with no-arbitrage as long as the appreciation or depreciation of m-dollars relative to dollars compensates for the interest rate differential. For instance, if the central bank sets a negative interest rate on dollars, then the price of m-dollars (which pay zero interest) expressed in terms of dollars must fall over time that is, m-dollars must depreciate relative to dollars.

According to Buiter the third strategy suffers from just one possible problem: If for some reason, the numéraire ‘followed the currency’ and people started to quote prices in m-dollars then nothing would have been gained. But he argues that the government has means to coordinate society on using a specific money as unit of account, for instance by requiring taxes to be paid in that money (that is, in dollars rather than m-dollars).

Buiter refers to contributions by Eisler (1932), Goodfriend (2000), Buiter and Panigirtzoglou (2001, 2003), Davies (2004), Buiter (2004, 2007) as well as Mankiw’s blog post (April 19) on a graduate student proposal to depreciate cash by means of a lottery.

In another blog post a few days later, Buiter offers further discussion and a rather sarcastic comment on option two:

Taxing currency will, I am afraid, remain rather intrusive and administratively cumbersome. This may of course recommend it to some of our leaders.

He also notes that Charles Goodhart has been talking for years about the lottery proposal by Gregory Mankiw’s graduate student. And he points out that this proposal is not fool proof: Even when a lottery rendered bank notes with a specific last digit in their serial number “officially” worthless people might still continue to value them; confiscation threats etc. might therefore be needed in addition to the lottery in order to sustain the scheme.