In Christos V. Gortsos and Rolf Sethe, editors: Central Bank Digital Currencies, EIZ Publishing, ch. 3, Zurich, October 2023. PDF.

Tag Archives: Euro

Financial Sanctions, the USD, and the EUR

On Moneyness, JP Koning discusses the ability or not of the U.S. treasury to enforce financial sanctions overseas. Focusing on the Iran sanctions that ran from 2010 to 2015 (with strong international support) and are scheduled to be reimposed soon (without such support) Koning compares the U.S. sanctions regime to an exclusivity agreement that a large retailer imposes on a manufacturer.

Foreign banks in places like Europe were free to continue providing transactions services to Iran, but if they did so they would not be able to maintain correspondent accounts at U.S. banks. To ensure these rules were enforced, U.S. banks were to be fined and U.S. bank executives incarcerated if found guilty of providing accounts to offenders. Fearful bank executives were very quick to comply by carefully vetting those that they offered correspondent banking services to.

Having a U.S. correspondent account is very important to a non-US bank. If a European bank has a corporate customer who wants to make a U.S. dollar payment, the bank’s correspondent relationship with a U.S. bank allows it to effect that payment. Since the revenues from U.S. dollar payments far exceeds revenues from providing Iranian agencies and corporations with payments services, a typical European bank would have had no choice but to abandon Iran in order to keep its U.S. correspondent account.

But what would happen if Iran were to invoice in EUR rather than USD and make payments using an account at a European bank, bank X say, without direct links to the U.S. and no U.S. correspondent account? The answer to that question depends on whether the U.S. treasury would be prepared to sanction a third financial institution, bank Y say, that collaborates with bank X (or a business partner of bank X) and relies on a U.S. correspondent account. In the most extreme scenario bank Y would be the European Central Bank.

One scheme would be to set up a single sanctions-remote bank that conducts all Iranian business. To defang the U.S. Treasury’s threat “do business with us, or them, but not both!”, this bank should not be dependent on U.S. dollar business. Without a U.S. correspondent, the Treasury’s threat to disconnect it from the correspondent network packs no punch. … Crude oil buyers from all over Europe could have their banks wire payments to [bank X’s] account via the ECB’s large value payments sytem, Target2. [Bank X] could also open accounts for companies in India, China, and elsewhere who want to buy Iranian crude oil with euros.

… There is also the extreme possibility that the U.S. would impose travel bans on the ECB itself, in an effort to force ECB officials to remove [bank X] from Target2. Here is one such threat: “Treasury this week designated the governor of Iran’s central bank—does any European country think Treasury can’t designate their own central bank governor too?” Look, the idea of preventing Mario Draghi from travelling to the U.S., or blocking his U.S. assets, sounds so unhinged that it’s not even worth entertaining.

The reason Iran and its trading partners were not able to break sanctions between 2010 and 2015, according to Koning, is that Europe (specifically the German chancellor Angela Merkel) supported the U.S. administration and imposed its own sanctions on bank X, cutting it off the SWIFT and Target2 networks.

Re-Denomination Risk in France and Italy

On the FT Alphaville blog, Mark Weidemaier and Mitu Gulati argue that re-denomination risk in the Euro zone is most prominent in France and Italy. Bonds with CACs trade at higher prices.

Most French and Italian [but not Greek] debt is governed by local law. … the governments could pass legislation redenominating their bonds from euros to francs or lira.

… [But] some French and Italian bonds — bonds issued after January 1, 2013, with maturities over a year — have Collective Action Clauses (CACs). … Importantly, these CACs require a super-majority of investors (in principal amount) to approve any changes to the currency of the bond.

… But it’s also possible a local law bond is no different than a local law bond with a CAC. After all, both are ultimately subject to the whims of the local legislature, and the courts may side with them.

The markets seem to have a view, though: CAC bonds in the countries with heightened redenomination risk seem to be valued significantly more.

Re-denomination Constitutes Default

In a letter to the editor of The Economist, Moritz Kraemer, sovereign chief ratings officer of S&P Global Ratings, clarifies what it would mean for France to re-denominate French debt:

Buttonwood wondered whether Marine Le Pen’s plan to re-denominate French government euro bonds into new francs might constitute a sovereign default (January 14th). There is no ambiguity here: it would. If an issuer does not adhere to the contractual obligations to its creditors, including payment in the currency stipulated, S&P Global Ratings would declare a default. Our current AA rating on France suggests, however, that such a turn of events is highly unlikely.

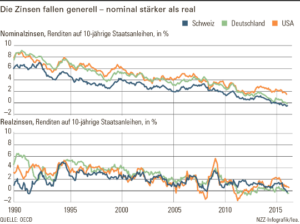

Nominal and Real Interest Rates over the Medium Term

From the NZZ:

“Dirk Niepelt über die Folgen eines Brexit für die Schweiz (What Brexit Means for Switzerland),” SRF, 2016

SRF, Tagesgespräch, June 16, 2016. HTML with link to MP3.

- Half-hour-long interview on the Swiss news channel.

- Topics include monetary policy, exchange rates, financial stability, Brexit.

Covered Interest Parity and the Risk-Taking Channel

In a speech, Hyun Song Shin points out that CIP increasingly fails to hold: the Dollar interest rate implied by FX swaps vis-a-vis the Euro, Yen, Pound or Swiss Franc is “too high.” Moreover, the deviation is negatively correlated with the Dollar’s spot exchange rate: When the Dollar appreciates, the deviation from CIP widens.

Shin argues that bank behavior explains the deviation:

… the US dollar is used widely throughout the global banking system, even when neither the lender nor the borrower is a US resident. … The consequence of the dollar’s international role in transactions is that the global banking system runs on dollars.

… key feature of the risk-taking channel is that when the dollar depreciates, banks lend more in US dollars to borrowers outside the United States. Similarly, when the dollar appreciates, banks lend less, or even shrink outright the lending of dollars. In this sense, the value of the dollar is a barometer of risk-taking and global credit conditions.

… The breakdown of covered interest parity is a symptom of tighter dollar credit conditions putting a squeeze on accumulated dollar liabilities built up during the previous period of easy dollar credit. During the period of dollar weakness, global banks were able to supply hedging services to institutional investors at reasonable cost, as cross-border dollar credit was growing strongly and easily obtained. However, as the dollar strengthens, the banking sector finds it more challenging to roll over the dollar credit previously supplied.

One way to summarise the finding is that there is a “triangle” that links a stronger dollar, more subdued dollar cross-border flows, and a widening of the cross-currency basis against the dollar.

With the Euro’s rising role as an international funding currency CIP deviations also show up for the Euro.

… the risk-taking channel for the euro is starting to show the tell-tale negative relationship between a weaker currency value and expanding cross-border lending in that currency; it was not there before the crisis, but has emerged since the crisis.

The upshot:

The financial channel of exchange rates operates when currency appreciation elicits valuation changes on borrower balance sheets. …

When we do international finance, we often buy into the “triple coincidence” where the GDP area, decision-making unit and currency area are one and the same … Currency appreciation or depreciation then acts on the economy through changes in net exports. [But that’s misleading.]

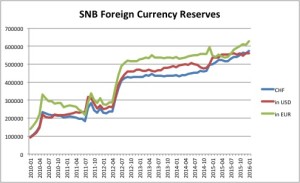

SNB Foreign Currency Reserves

Rising.

Source: SNB. The series “in EUR” is based on the author’s calculations.

Note: The exchange rate floor vis-a-vis the Euro was in place from 6 September 2011 until 15 January 2015.

Money, Interest Rates, Exchange Rates and Inflation in Switzerland

European Unity and the Principle of Unity of Liability and Control

In its recent special report entitled „Consequences of the Greek Crisis for a More Stable Euro Area,“ the German Council of Economic Experts has stressed the dangers due to institutional deficiencies and discretionary decision making in the Euro area. The executive summary concludes with the statement:

The institutional framework of the single currency area can only ensure stability if it follows the principle of unity of liability and control. Reforms that stray from this guiding principle plant the seeds of further crises and may damage the process of European integration.

Europe, Monetary Union and Fiscal Union

In a recent blog post, John Cochrane criticizes the common wisdom that, on economic grounds, the Euro was a bad idea for Europe.

He responds to an earlier New York Times article by Greg Mankiw who argued that conventional wisdom: A monetary union requires (1) cross-subsidization/insurance across regions (“fiscal union”) or (2) significant labor mobility across regions. The US has both, Europe does not; Europe therefore needs regional monetary policy instruments and fluctuating exchange rates to dampen the consequences of adverse regional economic shocks.

Cochrane retorts

I am a big euro fan. … I am also a big meter fan. I don’t think each country needs its own measure of length, or to shorten it when local clothiers are having trouble and would like to raise cloth prices.

Cochrane takes aim at the “deeply old-Keynesian” notion that small regions with fewer inhabitants than the Los Angeles metro area (Greece or Ireland say) are exposed to regional “demand” shocks which require regional fiscal or monetary policy responses. In his view, these are small open economies, and demand shocks arise externally.

Cochrane questions the characterization of the US as “fiscal union.”

In the US, we have Federal contributions to social programs such as unemployment insurance. Europe has the common agricultural policy and many other subsidies. We do not have systematic, reliably countercyclical, timely, targeted, and temporary local fiscal stimulus programs. Just how big is the local cyclical variation in state or local level government spending or transfers? (And why does fiscal union matter so much anyway? If you’re a Keynesian, then local borrow and spend fiscal stimulus should be plenty. The union matters only when countries near sovereign default and can’t borrow.) … Yes, both US and Europe have some pretty large cross-subsidies. But most of these are permanent. … Monetary policy has at best short-run effects, so the argument for currency union has to be about local cyclical, recession-related variation in economic fortunes, not permanent transfers.

He also points out that US monetary union far precedes US “fiscal union.” (And he questions the notion that “tight fiscal policy” lies at the root of Greece’s problems and easy monetary policy would have helped.)

Regarding labor mobility, Cochrane emphasizes again that it is cyclical labor mobility which should matter according to the conventional wisdom. He doubts that there are large differences in cyclical labor mobility between the US and Europe.

Not only are the gains from monetary decentralization in Europe small, according to Cochrane, but the benefits from monetary centralization are large, because of gains in credibility.

When Greece and Italy joined the euro, they basically said, defaulting and inflating now will be extremely costly. They were rewarded for the precommitment with very low interest rates. They blew the money, and are now facing the high costs they signed up for. But that just shows how real the precommitment was.

And Cochrane makes the point that policy should address underlying frictions:

The case for separate currencies is to protect the economy from sticky wages, sticky prices, and sticky people. But none of these stickinesses are written in stone. A plausible answer to my question about pre-new deal US is that prices and wages were not sticky (whatever that means) before the era of regulation. Well, that is a loss, and only very imperfectly addressed by artful devaluation of the currency. Not every block can have its own currency, so local and industry variation within a country remains hobbled by sticky prices, wages, and people. If sticky wages, prices and people are the central economic problem, we ought to have a lot of policies to unstick them. We do the opposite, and Europe even more so. The very social programs that Greg implicitly praises for fiscal stimulus tie people to location and undermine labor market flexibility.

He concludes:

So I think a lot of the conventional view seems to think implicitly of fairly closed economies, operating in parallel. But Europe’s economies are open. Moreover, the whole point of the eurozone is to open them further. Small open economies are much worse candidates for their own currency.

The Euro/Swiss Franc Exchange Rate

Was it wise for the Swiss National Bank (SNB) to abandon the exchange rate floor vis-a-vis the Euro (EUR) half a year ago (see the blog entry on the decision and on the critique by Willem Buiter)?

Here are some considerations to keep in mind.

- Is the Swiss France (CHF) overvalued? The following graph plots the nominal and real exchange rates since 1981 (the real rate is computed based on Swiss and Euro area producer price indices, 2010=100; data file).

Relative to the long-term average, the CHF currently is overvalued in real terms by 14%. In December 2014, it was overvalued by 4%; and in August 2011, by 11%. But in December 2007, it was undervalued by 21%. According to the real exchange rate metric, importers (households) thus suffered more in 2007 than exporters suffer today. For a related assessment based on consumer (Big Mac) prices, see this blog post. - The real exchange rate is just one metric to assess whether a currency is overvalued. There are many others, see for example this IMF paper or this book. Also, foreign exchange market participants are willing to buy and hold CHFs and EURs at the going market rate; they seem to think that the price is right.

- If the price were right and policy weakened the CHF, then Switzerland would trade off “competitiveness” of the export sector on the one hand, and expected capital losses on the country’s EUR holdings that would have to be purchased to temporarily strengthen the EUR on the other. Back-of-the-envelope calculations by my colleague Harris Dellas suggest that weakening the CHF would not be worth it, financially speaking.

- Even if, for whatever reason, society favored a weaker CHF it is not clear that the SNB should intervene. The SNB should only act if its mandate of pursuing price stability calls for such action. In the short run, a weaker CHF would indeed help to push the inflation rate in the desired range. In the longer run, however, a further lengthening of the SNB’s balance sheet (resulting from forex market interventions) could undermine the SNB’s flexibility, in particular if political constraints were to bind.

- This does not rule out, however, that other institutions in Switzerland could or should enter the exchange rate business. In principle, fiscal policy makers could institute a sovereign wealth fund that is financed by issuing CHF bonds and invested in EUR assets. Fiscal policy makers could also try to redistribute from those currently benefiting to those suffering from the CHF/EUR exchange rate. Export subsidies could be an instrument. They would be hard to implement though if one wanted to account for intermediate inputs.

- That Switzerland has an independent currency is a choice that reflects repeated, in depth deliberations. Advantages of pursuing an independent monetary policy include the option value to pursue price stability even if other currency blocs don’t; and the ensuing credibility benefits for Switzerland as a whole. Disadvantages include temporary, but potentially long-lasting real exchange rate misalignments that strain some groups (e.g., workers in the export sector) while benefiting others (e.g., consumers). These advantages and disadvantages do not come as a surprise; Switzerland has chosen them.

Last Exit Before Grexit?

Nicolai Kwasniewski reports in Der Spiegel about the last (?) chance for Greece to avoid Grexit.

- By Wednesday night, Greece has to submit a request for an ESM program.

- After discussing the request, Euro finance ministers will ask the “institutions” to evaluate it and to assess whether the stability of the Euro zone is under threat (a prerequisite for ESM funding), the program is sustainable etc.

- Greece has to submit detailed reform proposals until Thursday. To be acceptable, they will have to satisfy stricter requirements than those the Greek voters recently rejected.

- Euro finance ministers will evaluate the proposals on Saturday.

- EU prime ministers and presidents have the last word on Sunday.

Peter Spiegel, Anne-Sylvaine Chassany and Duncan Robinson report in the FT.

Arguments in Favor of ELA to Greece

Martin Hellwig argues in the Handelsblatt that the ECB should not cut Emergency Liquidity Assistance (ELA) to the Greek central bank. He makes the following points:

- In 2010, the ECB pressured Ireland to guarantee bank liabilities (vis-a-vis other European banks) by threatening to cut ELA. Such blackmailing is inconsistent with the ECB’s task to safeguard cash and payment systems.

- The same applies to Greece now. As lender of last resort, the ECB should provide funding to Greek banks even (or exactly) when they don’t have access to markets, as long as they are solvent. In principle, the banks may use central bank funding for whatever purpose they see fit; right now, however, the ECB has put restrictions on Greek banks’ purchases of Greek government bonds.

- Are the Greek banks solvent? There are certainly liquidity problems, due to heavy withdrawals triggered by fears that the Greek government may convert Euro into Drachma denominated deposits. Solvency problems are only very recent, due to the economic malaise.

At this point Hellwig stops arguing based on the European treaties.

- Instead, he suggests that the solvency rule could be waived in situations like currently in Greece or in Germany in 1931.

- He concedes that a freezing of ELA could be considered a precautionary measure against Grexit—an event that is not anticipated in the European treaties.

- But it could also be considered a measure that forces Greece into economic turmoil; the Greek banks into insolvency; and Greece out of the Euro area against its will.

The Greek Bank Holiday and Capital Controls

Saturday, 27 June 2015 and earlier:

- In a Medium blog post, Karl Whelan provides an excellent discussion of the policy mistakes that worsened the Greek debt crisis.

- Hans-Werner Sinn’s “The Greek Tragedy.”

- Alex Barker discusses in the FT the options for Greece’s banking system.

Sunday, 28 June:

- Christian Rickens comments in Der Spiegel that the upcoming Greek referendum is the price to pay for five years of cowardice, both on the part of the Greek government and its European partners.

- The FT summarizes the main policy decisions during the last days that led the Greek economy to “hit a roadblock.”

- The Economist writes that “[I]n these circumstances a cap on ELA must mean tough restrictions on deposit withdrawals both in cash and through transfers abroad.” It draws parallels to Cyprus in March 2013 where banks closed for two weeks and where capital controls were recently lifted.

- Ekathimerini reports about the decision to close the banks and instate capital controls. It quotes the Greek prime minister as saying that “[Rejection] of the Greek government’s request for a short extension of the program was an unprecedented act by European standards, questioning the right of a sovereign people to decide. … This decision led the ECB today to limit the liquidity available to Greek banks and forced the Greek central bank to suggest a bank holiday and restrictions on bank withdrawals. … One thing is clear: the refusal of a short extension, and the attempt to nullify a democratic procedure is an act deeply offensive and shameful for the democratic traditions of Europe.”

Monday–Tuesday, 29–30 June:

- Claire Phipps summarizes in The Guardian the main elements of the ‘Bank Holiday break’ decree that the Greek prime minister and president enacted during the night, in response to “the extremely urgent and unforeseen need to protect the Greek financial system and the Greek economy due to the lack of liquidity caused by the Eurogroup’s decision on June 27 to refuse the extension of the loan agreement with Greece”.

- Philip Stafford and Roger Blitz speculate in the FT about the implications of Grexit. (See also the earlier post on Lex Monetae.)

- The FT’s liveblog.

- In the FT, Martin Sandbu convincingly addresses questions on the bigger picture, including political aspects of the crisis.

- Anil Kashyap has published “A Primer on the Greek Crisis.”

- In the FT, Shawn Donnan discusses the consequences of a Greek default against the IMF.

- Der Spiegel reviews how the international press assigns responsibility for the crisis.

Wednesday, 1 July:

- In the FT, Peter Spiegel outlines the way forward to a new “Greek” bailout.

- The Economist’s Free Exchange blogger on the limited experience with capital controls (Iceland, Cyprus, now Greece).

Note: This post has been updated repeatedly.

Greece is not Ireland

In a Credit Writedowns blog post, Frederick Sheehan collected quotes that relate to the European debt crisis (he writes that Dennis Gartman first compiled the list). Some highlights:

“For a small, open economy like Cyprus, Euro adoption provides protection from international financial turmoil.”

– Jean-Claude Trichet, President, European Central Bank, January 2008

“Spain is not Greece”

– Elena Salgado, Spanish Finance Minister, February 2010

“Portugal is not Greece”

– The Economist, 22 April 2010

“Ireland is not in Greek territory”

– Brian Lenihan, Irish Finance Minister

“Greece is not Ireland”

– George Papandreou, Greek Finance Minister, 22 November 2010

“Spain is neither Ireland nor Portugal”

– Elena Salgado, Spanish Finance Minister, 16 November 2010

“Neither Spain nor Portugal is Ireland”

– Angel Gurria, Secretary-General, OECD, 18 November 2010

“Spain is not Uganda”

– Mariano Rajoy, Spanish Prime Minister, 9 June 2010

“Italy is not Spain”

– Ed Parker, Managing Director, Fitch, 12 June 2012

“When it becomes serious, you have to lie.”

– Jean-Claude Juncker, President, Euro Group, April 2011

“The worst is now over—the situation is stabilizing.”

– Mario Draghi, President, European Central Bank, March 2012

“Uganda does not want to be Spain”

– Asuman Kiyingi, Uganda’s Foreign Minister, 13 June 2012

Populist Dishonesty?

Marc Champion comments in Ekathimerini that the planned referendum question in Greece disguises the relevant trade-offs.

Not once in his address on the referendum did Tsipras mention the common currency. When the Associated Press asked Syriza cabinet minister Panagiotis Lafazanis whether the nirvana of reconstruction and progress he described as following from a “no” vote to the bailout would involve leaving the euro, he said: “It is you [the media] who pose this dilemma.”

“On the Credibility of the Euro/Swiss Franc Floor: A Financial Market Perspective”

Markus Hertrich and Heinz Zimmermann argue in a working paper that after August 2014, financial markets priced in a significant probability that the Swiss National Bank would abolish the exchange rate floor vis-a-vis the Euro. Hertrich and Zimmermann write in the abstract:

We observe a drastic increase in the break-probabilities after August 2014, reaching a level of nearly 50%, which was the level before the announcement of the details of the “Draghi put” in September 2012. The credibility of the SNB in maintaining the floor, as seen from the option market, was thus substantially lower than publicly claimed.

The Euro Area as a System of Currency Boards?

Willem Buiter argues in a Citi research note that due to limited risk sharing, the system of Euro area national central banks has morphed into a system of currency boards.

Contagion in the Euro Area

In a Vox column, Michal Kobielarz, Burak Uras and Sylvester Eijffinger argue that the re-emergence of spreads between peripheral and core Eurozone countries at the beginning of the Greek crisis reflected contagion fears. They write:

… we explicitly model the endogenous bailout decision of the European Monetary Union. We assume that:

- A country that defaults on its sovereign debt can no longer remain in the EMU, unless it is bailed out;

- The union values each country’s membership and, therefore, suffers a loss if a country exits; and

- The marginal loss associated with allowing a country to leave the union is highest if that particular country is the first to leave (first-exit effect).

… once the first country is gone, letting a second country default and leave the union is not that costly anymore.

Germany and the Euro

In an FT oped, Thomas Mayer summarized a rather typical “German” perspective on European monetary policy. In his view, a sound euro needs either full political union or just stringent rules that are enforced. Helmut Kohl promised the former. When it didn’t happen, ECB independence and the Maastricht treaty should substitute. Ex post, Germany should have asked for more, in particular resolution and exit procedures (and, one may add, it should have played by the rules itself). The crises in the Eurozone illustrated governance problems. Merkel feared Grexit and tried to reestablish the rules. She

built a pan-European “shadow state” — a web of pacts to ensure that countries followed policies consistent with sound money.

It has not worked. From Greece to France, countries resist any infringement on their sovereignty and refuse to act in a way that is consistent with a hard currency policy. The ECB is forced to loosen its stance. Worse, it has allowed monetary policy to become a back channel for transfering economic resources between eurozone members, which politicians have refused to allow through fiscal mechanisms they control. This is Germany’s worst nightmare.

How will the situation be resolved? A century ago, Eugen Böhm-Bawerk, the Austrian economist and finance minister, proclaimed laws of economics to be a higher authority than political power. Some Germans say that a hard currency is an essential part of their economic value system. If both are right, politicians will be powerless to prevent Germany’s departure from a monetary union that is at odds with the country’s economic convictions.

Real Exchange Rates

The Economist published its most recent Bic Mac index. The Swiss Franc is overvalued by 56% and the Euro undervalued by 11%.

The Economist’s Big Mac Index site provides more details and the dataset.

Long-Term CHF Strength

The two figures illustrate the Swiss Franc’s long-term strength vis-a-vis the dollar, the French Franc, the German Mark and the Euro.

Source: FRED (St Louis Fed): XLS.

1.20 No Longer

The Swiss National Bank announced that it discontinues the exchange rate floor of CHF 1.20 vis-a-vis the Euro and lowers interest rates, to -0.75%. Markets are surprised. Michael Hunter writes in the FT:

The move came as a surprise since Thomas Jordan, SNB chairman, said as recently as December that Switzerland’s defence of the SFr1.20 rate against the euro was “absolutely necessary”.

A graph of the exchange rate series (source):