Premiere: November 26, 1942 in New York.

Premiere: November 26, 1942 in New York.

It’s the time of the year when financial advisors feel obliged to produce forecasts for the coming year. This is often a waste of time, for the writers and the readers.

In the Wall Street Journal, James Mackintosh writes that

[f]orecasting is difficult, but this year showed exactly how pointless it can be: Markets performed opposite of virtually all predictions.

Previous blog post.

In the New York Times, Susan Dynarski argues that students learn less when they use laptops, tablets and the like during lectures.

… a growing body of evidence shows that over all, college students learn less when they use computers or tablets during lectures. They also tend to earn worse grades. The research is unequivocal: Laptops distract from learning, both for users and for those around them. It’s not much of a leap to expect that electronics also undermine learning in high school classrooms or that they hurt productivity in meetings in all kinds of workplaces.

She points to studies arguing that “laptop note takers’ tendency to transcribe lectures verbatim rather than processing information and reframing it in their own words is detrimental to learning” and “multitasking on a laptop poses a significant distraction to both users and fellow students.”

Previous blog post.

In The Guardian, Philip Oltermann speculates about a new romanticist era in Germany, exemplified by Simon Strauss’ “Sieben Nächte.”

Caspar David Friedrich: Winter Landscape, 1811.

On Noahpinion.

In an interview with The Independent, Jean Tirole discusses monopolies, regulation, the role of the state, the “Nobel syndrome,” and much more.

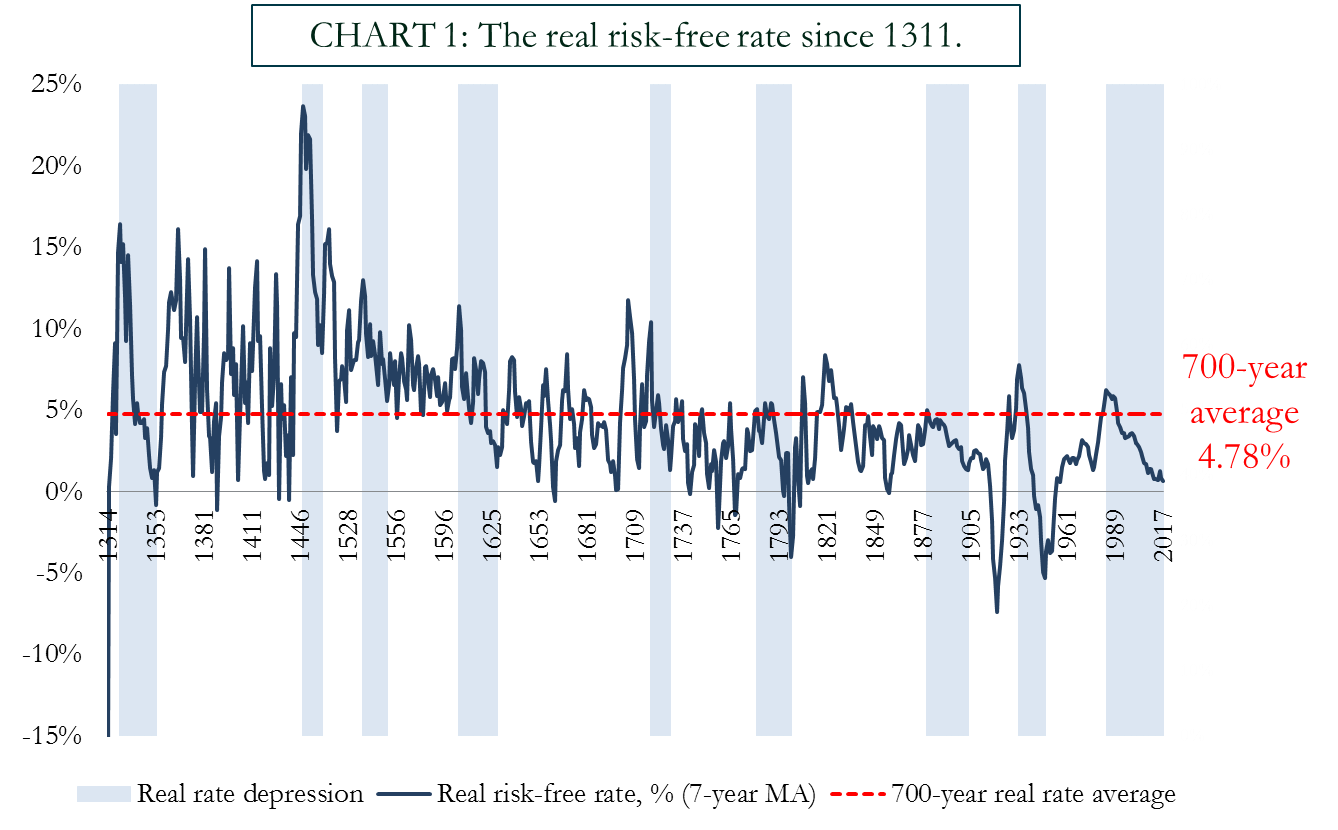

On Bank Underground, Paul Schmelzing looks at real interest rates over the last 700 years and finds that

… the past 30-odd years more than hold their own in the ranks of historically significant rate depressions. But the trend fall seen over this period is a but a part of a much longer ”millennial trend”. It is thus unlikely that current dynamics can be fully rationalized in a “secular stagnation framework”.

High rates of tax evasion are not necessarily a consequence of high tax rates. In an NBER working paper, Annette Alstadsæter, Niels Johannesen, and Gabriel Zucman provide estimates of countries’ wealth holdings in “tax havens.” Based on BIS statistics the authors find that:

In the Boston Review, Dani Rodrik discusses neoliberalism and argues that

mainstream economics shades too easily into ideology, constraining the choices that we appear to have and providing cookie-cutter solutions.

Rodrik emphasizes that sound economics implies context specific policy recommendations.

And therein lies the central conceit, and the fatal flaw, of neoliberalism: the belief that first-order economic principles map onto a unique set of policies, approximated by a Thatcher–Reagan-style agenda.

But he also stresses that the

principles [of economics] are not entirely content free. China, and indeed all countries that managed to develop rapidly, demonstrate their utility once they are properly adapted to local context. Conversely, too many economies have been driven to ruin courtesy of political leaders who chose to violate them.

In Rodrik’s view

[e]conomists tend to be very good at making maps, but not good enough at choosing the one most suited to the task at hand.

I have argued elsewhere that the main job of economists is to create maps, not to choose among them. See also the earlier post on Ariel Rubinstein’s excellent discussion of Rodrik’s recent book.

Jointly with the Council on Economic Policies and the Swiss National Bank, the Study Center Gerzensee organized a conference on Aggregate and Distributive Effects of Unconventional Monetary Policies. The program can be viewed here.

From About this Report:

[T]he U.S. Global Change Research Program (USGCRP) oversaw the production of this stand-alone report of the state of science relating to climate change and its physical impacts. …

The USGCRP is made up of 13 Federal departments and agencies that carry out research and support the Nation’s response to global change. The USGCRP is overseen by the Subcommittee on Global Change Research (SGCR) of the National Science and Technology Council’s Committee on Environment, Natural Resources, and Sustainability (CENRS), which in turn is overseen by the White House Office of Science and Technology Policy (OSTP). The agencies within USGCRP are the Department of Agriculture, the Department of Commerce (NOAA), the Department of Defense, the Department of Energy, the Department of Health and Human Services, the Department of the Interior, the Department of State, the Department of Transportation, the Environmental Protection Agency, the National Aeronautics and Space Administration, the National Science Foundation, the Smithsonian Institution, and the U.S. Agency for International Development.

From the Executive Summary:

… it is extremely likely that human activities, especially emissions of greenhouse gases, are the dominant cause of the observed warming since the mid-20th century. For the warming over the last century, there is no convincing alternative explanation supported by the extent of the observational evidence. …

The magnitude of climate change beyond the next few decades will depend primarily on the amount of greenhouse gases (especially carbon dioxide) emitted globally. Without major reductions in emissions, the increase in annual average global temperature relative to preindustrial times could reach 9°F (5°C) or more by the end of this century. With significant reductions in emissions, the increase in annual average global temperature could be limited to 3.6°F (2°C) or less.

In the New York Times, Lisa Friedman and Glenn Thrush write that the report contradicts positions of the Trump administration on climate change.

While there were pockets of resistance to the report in the Trump administration, according to climate scientists involved in drafting the report, there was little appetite for a knockdown fight over climate change among Mr. Trump’s top advisers …

The White House put out a statement Friday that seemed to undercut the high level of confidence of the report’s findings. …

Responsibility for approving the report fell to Gary D. Cohn, director of the National Economic Council, who generally believes in the validity of climate science and thought the issue would have been a distraction from the tax push, according to an administration official with knowledge of the situation.

An excellent conference organized by the Monetary Law Forum Switzerland focused on blockchain use cases from a central bank perspective. Program, links to slides.

I discussed the macroeconomic perspective and argued for “reserves for all.”

Some related links: Nivaura and Allen & Overy (backing Nivaura). OTC Swiss Blockchain, by Roman Bischoff.

How light emissions across the globe changed between 2012 and 2016. Link to a navigable map.

University of Copenhagen, Department of Economics Discussion Paper 17-18, July 2017, with Martin Gonzalez-Eiras. PDF.

We propose a theory of tax centralization and intergovernmental grants in politico-economic equilibrium. The cost of taxation differs across levels of government because voters internalize general equilibrium effects at the central but not at the local level. The equilibrium degree of tax centralization is determinate even if expenditure-related motives for centralization considered in the fiscal federalism literature are absent. If central and local spending are complements, intergovernmental grants are determinate as well. Our theory helps to explain the centralization of revenue, introduction of grants, and expansion of federal income taxation in the U.S. around the time of the New Deal. Quantitatively, the model can account for the postwar trend in federal grants, and a third of the dramatic increase in the size of the federal government in the 1930s.

Jointly with the Journal of Economic Dynamics and Control, the St. Louis Fed, the University of Bern and the Swiss National Bank, the Study Center Gerzensee organized a conference on Fiscal and Monetary Policies. The program can be viewed here.

Greg Mankiw offers a simple example to establish that a reduction in the tax rate on capital income (in a closed economy) raises wages in the long run. John Cochrane patiently typed the solution. And Larry Summers argues on his blog that US realities are not well captured by Mankiw’s example.

On his blog, John Cochrane argues that banks could, and should be 100% equity financed. His points are:

(1) There are plenty of safe assets—government debt—out there and banks do not need to “create” additional safe assets—deposits.

I share this view partly. First, I don’t know what amount of safe assets are sufficient from a social point of view. Second, I don’t consider government debt to be a safe asset. Third, debt has safety and liquidity properties. The question is not only whether assets/liabilities provide sufficient safety but also whether they serve as means of payment in the same way that base money and deposits do. The key question then is: Do we need inside money? I don’t think that macroeconomics has a convincing answer to this question at this point. But I note that some preeminent macroeconomists (NK) argue that banks can create means of payment better than some governments. If this is true then John’s first argument partly misses the point (although he addresses a related point later).

In spite of these reservations, I share John’s view that in the aggregate, safety cannot be created by means of financial intermediation. Projects and claims to future tax revenue generate returns. The financial system can slice and distribute these returns in different ways (creating safer claims by rendering other claims less safe) but it cannot create safety in the aggregate.

(2) Households and firms no longer need assets (i.e., liabilities of financial institutions) with a fixed nominal value in order to make payments.

I agree. As John writes:

In the past, the only way that a security could be “liquid” is if it promised a fixed payment. You couldn’t walk in to a drugstore in 1935, or 1965, and trade an S&P500 index share for a candy bar. Now you can. (And as soon as it is cleared by blockchain, it will be even faster and cheaper than credit cards.) There is no reason your debit card cannot be linked to an asset whose value floats over time.

(3) If society really needs more “safe” claims such claims can be created on banks rather than in banks. As John writes:

Let the banks issue 100% equity. Then, let most of that equity be held by a mutual fund, ETF, or bank holding company, and let those issue deposits, long term debt, and a small amount of additional equity. Now I have “transformed” risky assets into riskfree debt via leverage. But the leverage is outside the bank.

I agree. In an article (2013) I have described a proposal by BIS economists that relies on equity financed banks and levered bank holding companies to help solve the too-big-to-fail problem.

(4) Why should less “safe” bank liabilities lead to a credit crunch?

I share John’s puzzlement with the often heard claim that fewer bank deposits would go hand in hand with less credit. I believe that this claim mostly reflects confusion about the interplay between national saving and investment on the one hand, and bank balance sheets on the other. There is no mechanical link between the two but of course, there are many indirect links.

All in all, I am as skeptical as John about the view that bank created money obviously is important. I think that bank created money has some useful roles to play but they are more subtle. At the same time, I believe that bank created money is likely to stay with us even if it is not socially useful. Proposals to ban inside money therefore are unlikely to succeed (see my writing on Vollgeld).

On Alphaville, Matthew Klein points out that covered interest parity (dollar vs. yen) is alive and kicking again. It wasn’t during much of 2016. The Reserve Bank of Australia exploited the arbitrage opportunity.

NBER Working Paper 23864, September 2017, with Tamon Asonuma and Romain Ranciere. PDF. (Local copy.)

Rejecting a common assumption in the sovereign debt literature, we document that creditor losses (“haircuts”) during sovereign restructuring episodes are asymmetric across debt instruments. We code a comprehensive dataset on instrument-specific haircuts for 28 debt restructurings with private creditors in 1999–2015 and find that haircuts on shorter-term debt are larger than those on debt of longer maturity. In a standard asset pricing model, we show that increasing short-run default risk in the run-up to a restructuring episode can explain the stylized fact. The data confirms the predicted relation between perceived default risk, bond prices, and haircuts by maturity.

In an NBER working paper and a column on VoxEU, Michael Bordo and Andrew Levin make the case for central bank issued digital currency (CBDC).

Bordo and Levin favor an account-based CBDC system (managed or supervised by the central bank) rather than central bank issued tokens in the blockchain.

They emphasize the Friedman rule and the fact that interest paying CBDC affords the possibility to satisfy the rule:

These … goals – … a stable unit of account and an efficient medium of exchange – seemed to be irreconcilable due to the impracticalities of paying interest on paper currency, and hence Friedman advocated a steady deflation rather than price stability. But the achievement of both goals has now become feasible using a well-designed CBDC.

Interest paying CBDC would imply—payments to account holders. Bordo and Levin do not discuss the political economy implications. They are also silent about the transition from the current system with deposits to a new system with interest bearing CBDC in which demand for deposits would drastically fall.

Bordo and Levin favor abolishing cash to render monetary policy most powerful. Eliminating the option to withdraw cash would also eliminate the lower bound on nominal interest rates and would render unnecessary any “inflation buffer” of 2 percent or so. Monetary policy thus could move from positive inflation targets to a price level target.

Their paper contains a long list of useful references.

On Alphaville, Izabella Kaminska questions the utility settlement coin project (for an update on the project, see Martin Arnold’s recent FT article). She suspects that

USC isn’t really a blockchain project as much as a market infrastructure project — even if it leans on blockchain jargon for the purpose of gaining popular momentum. …

On paper, the technology promises to un-encumber cash collateral by creating a much more reliable form of distributed settlement, requiring a fraction of the collateral needed to operate a comparable centralised system.

She points to possible conflicts of interests. The project could just aim at convincing regulators that settlement processes are robust.

Hence most blockchain ventures today equate to nothing more than a lobbying effort by banks to get decentralized settlement approved again, ideally without any of the associated collateral headaches.

Can a USC-type project operate without support by the central bank? Kaminska says no since only the central bank can credibly monitor whether the promised backing of USC by base money actually is observed.

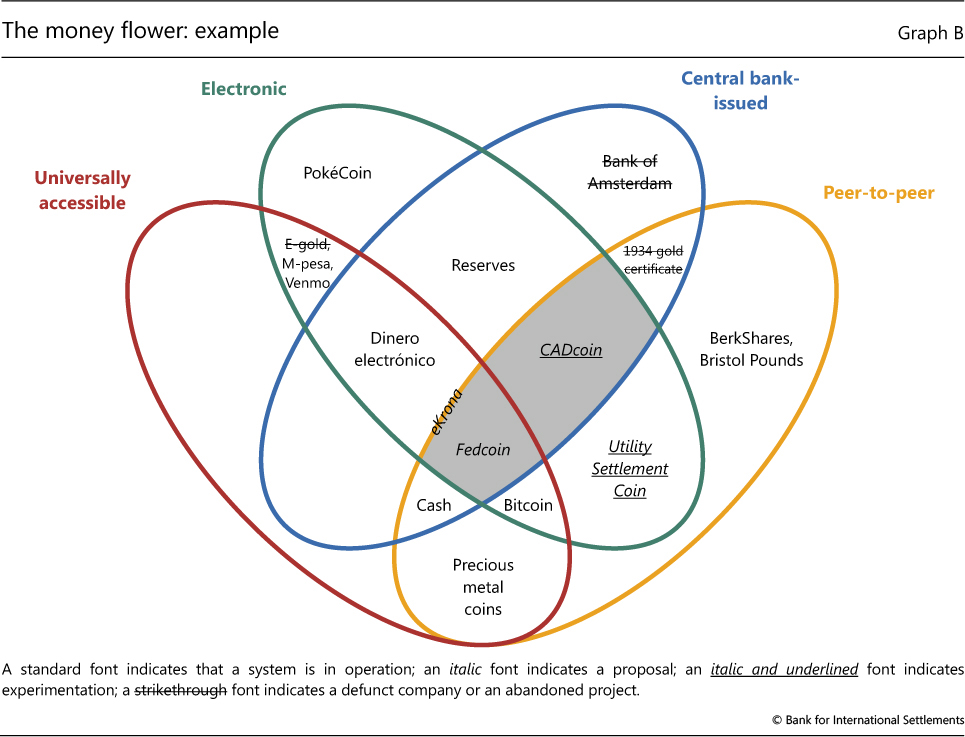

In a BIS Quarterly Review article, Morten Bech and Rodney Garratt offer a taxonomy of money, with special emphasis given to central bank issued digital and crypto currency. They stress four dimensions:

issuer (central bank or other); form (electronic or physical); accessibility (universal or limited); and transfer mechanism (centralised or decentralised). The taxonomy defines a CBCC as an electronic form of central bank money that can be exchanged in a decentralised manner known as peer-to-peer, meaning that transactions occur directly between the payer and the payee without the need for a central intermediary. This distinguishes CBCCs from other existing forms of electronic central bank money, such as reserves, which are exchanged in a centralised fashion across accounts at the central bank.

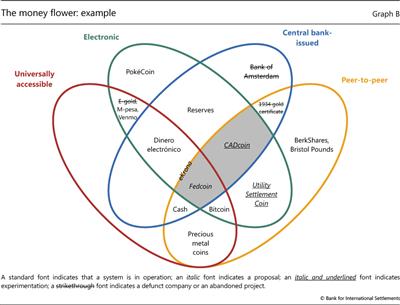

On Alphaville, Izabella Kaminska asks why a central bank would want to issue cryptocurrency rather than conventional digital currency.

… if anonymity is not the objective of issuing a centrally supervised cryptocurrency, what really is the point of using blockchain or crypto technology? Just issue a conventional digital currency and be done with it. If, on the other hand, anonymity is the objective of issuing a centrally supervised cryptocurrency, how can this be justified by a central bank in light of years of regulatory policy focused on making sure cashflows are more easily tracked and monitored … The idea it should be the central bank unwinding this trend is utterly bizarre.

And:

… the only incentive central banks really have for introducing cryptocurrencies is in performing a giant monetary bait and switch. “Hey guys! We’re offering this amazing anonymous central bank currency which is as strong and stable as the dollar and yet just as anonymous as bitcoin!!! Come, all you illicit users of physical cash, come use our amazing new currency! We swear it’s absolutely anonymous and will never lead to prosecutions. Honest!!”

Her post relates to a recent BIS Quarterly Review article by Morten Bech and Rodney Garratt.

On VoxEU, David Blanchflower and Andrew Oswald argue that it exists.

Overall, we think there is a great deal of evidence – though we have critics, especially among a small group of social psychologists – that humans experience a midlife psychological ‘low’. The midlife decline in wellbeing is apparently substantial and not minor … It should perhaps be emphasised that the midlife low is not affected by regression-equation controls for having young children, nor by changing the exact nature of the dependent variable.