Schweizer Monat, April 2022, with Markus Brunnermeier. PDF.

We describe challenges the digital money revolution poses for central banks and predict that more and more monetary authorities will introduce CBDCs.

Schweizer Monat, April 2022, with Markus Brunnermeier. PDF.

We describe challenges the digital money revolution poses for central banks and predict that more and more monetary authorities will introduce CBDCs.

Neue Zürcher Zeitung, February 17, 2022. PDF.

Wirtschaft Regional, January 7, 2022. PDF.

Interview on private and public money, digital payments, Bitcoin, cash.

In the FT, Hannah Murphy reports about Facebook’s launch of Libra.

Lots of skepticism in the comments section.

And Hannah Murphy reports that

[p]ositive Money, a consumer campaign group, attacked the proposal. “Our money is increasingly in the hands of a small number of banks and payment companies, and we should avoid ceding further control to unaccountable corporate interests. Facebook’s plans pose alarming implications for privacy and power in the economy,” said David Clarke, the head of policy at the group.

In an NBER working paper and a column on VoxEU, Michael Bordo and Andrew Levin make the case for central bank issued digital currency (CBDC).

Bordo and Levin favor an account-based CBDC system (managed or supervised by the central bank) rather than central bank issued tokens in the blockchain.

They emphasize the Friedman rule and the fact that interest paying CBDC affords the possibility to satisfy the rule:

These … goals – … a stable unit of account and an efficient medium of exchange – seemed to be irreconcilable due to the impracticalities of paying interest on paper currency, and hence Friedman advocated a steady deflation rather than price stability. But the achievement of both goals has now become feasible using a well-designed CBDC.

Interest paying CBDC would imply—payments to account holders. Bordo and Levin do not discuss the political economy implications. They are also silent about the transition from the current system with deposits to a new system with interest bearing CBDC in which demand for deposits would drastically fall.

Bordo and Levin favor abolishing cash to render monetary policy most powerful. Eliminating the option to withdraw cash would also eliminate the lower bound on nominal interest rates and would render unnecessary any “inflation buffer” of 2 percent or so. Monetary policy thus could move from positive inflation targets to a price level target.

Their paper contains a long list of useful references.

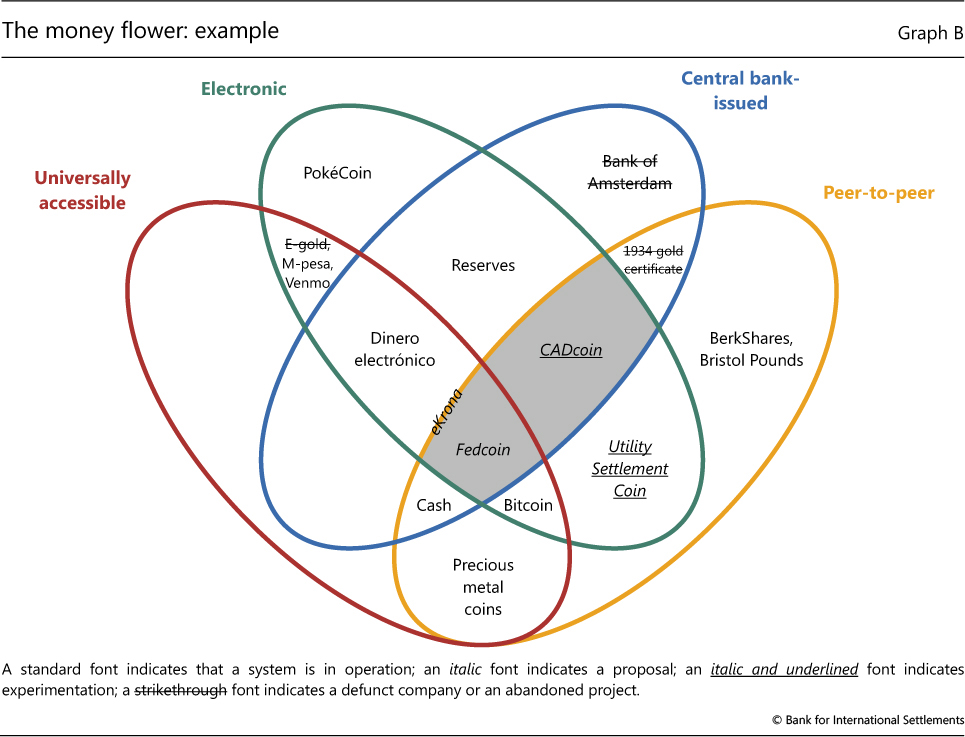

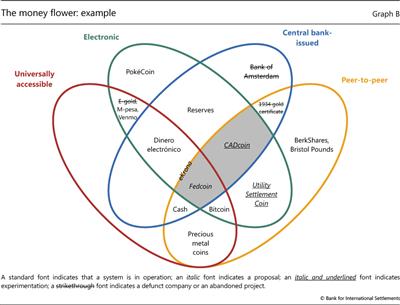

In a BIS Quarterly Review article, Morten Bech and Rodney Garratt offer a taxonomy of money, with special emphasis given to central bank issued digital and crypto currency. They stress four dimensions:

issuer (central bank or other); form (electronic or physical); accessibility (universal or limited); and transfer mechanism (centralised or decentralised). The taxonomy defines a CBCC as an electronic form of central bank money that can be exchanged in a decentralised manner known as peer-to-peer, meaning that transactions occur directly between the payer and the payee without the need for a central intermediary. This distinguishes CBCCs from other existing forms of electronic central bank money, such as reserves, which are exchanged in a centralised fashion across accounts at the central bank.

On Alphaville, Izabella Kaminska asks why a central bank would want to issue cryptocurrency rather than conventional digital currency.

… if anonymity is not the objective of issuing a centrally supervised cryptocurrency, what really is the point of using blockchain or crypto technology? Just issue a conventional digital currency and be done with it. If, on the other hand, anonymity is the objective of issuing a centrally supervised cryptocurrency, how can this be justified by a central bank in light of years of regulatory policy focused on making sure cashflows are more easily tracked and monitored … The idea it should be the central bank unwinding this trend is utterly bizarre.

And:

… the only incentive central banks really have for introducing cryptocurrencies is in performing a giant monetary bait and switch. “Hey guys! We’re offering this amazing anonymous central bank currency which is as strong and stable as the dollar and yet just as anonymous as bitcoin!!! Come, all you illicit users of physical cash, come use our amazing new currency! We swear it’s absolutely anonymous and will never lead to prosecutions. Honest!!”

Her post relates to a recent BIS Quarterly Review article by Morten Bech and Rodney Garratt.

The Swiss National Bank held its annual general meeting of shareholders (web TV). In response to one of the questions posed by shareholders Thomas Jordan suggested (2:58–2:59) that possibly a digital Swiss Franc might be introduced sometime in the future.

In the FT, Richard Milne reports about the Riksbank pondering to issue a digital currency.

There are considerable questions for Sweden’s central bank to answer about how a digital currency would work. Would individuals have an account at the Riksbank? Would transactions be traceable, unlike with cash? Would emoney earn interest?

Ms Skingsley said: “Personally I would like to design it in a way that is most like notes and coins.” That would mean no interest would be paid on it. But she added that the state had no interest in helping illegal activity, suggesting some form of traceability.

The Riksbank would also need to consider financial stability issues such as whether they would or should compete with commercial banks’ deposit base. Ms Skingsley said she was concerned that in times of financial instability citizens could transfer money to a state-backed electronic system, potentially increasing instability.

The blockchain technology opens up new possibilities for financial market participants. It allows to get rid of middle men and thus, to save cost, speed up clearing and settlement (possibly lowering capital requirements), protect privacy, avoid operational risks and improve the bargaining position of customers.

Internet based technologies have rendered it cheap to collect information and to network. This lies at the foundation of business models in the “sharing economy.” It also lets fintech companies seize intermediation business from banks and degrade them to utilities, now that the financial crisis has severely damaged banks’ reputation. But both fintech and sharing-economy companies continue to manage information centrally.

The blockchain technology undermines the middle-men business model. It renders cheating in transactions much harder and thereby reduces the value of credibility lent by middle men. The fact that counter parties do not know and trust each other becomes less of an impediment to trade.

The blockchain may lend credibility to a plethora of transactions, including payments denominated in traditional fiat monies like the US dollar or virtual krypto currencies like Bitcoin. An advantage of krypto currencies over traditional currencies concerns the commitment power lent by “smart contracts.” Unlike the money supply of fiat monies that hinges on discretionary decisions by monetary policy makers, the supply of krypto currencies can in principle be insulated against human interference ex post and at the same time conditioned on arbitrary verifiable outcomes (if done properly). This opens the way for resolving commitment problems in monetary economics. (Currently, however, most krypto currencies do not exploit this opportunity; they allow ex post interference by a “monetary policy committee.”) A disadvantage of krypto currencies concerns their limited liquidity and thus, exchange rate variability relative to traditional currencies if only few transactions are conducted using the krypto currency.

Whether blockchain payments are denominated in traditional fiat monies or krypto currencies, they are always of relevance for central banks. Transactions denominated in a krypto currency affect the central bank in similar ways as US dollar transactions, say, affect the monetary authority in a dollarized economy: The central bank looses control over the money supply, and its power to intervene as lender of last resort may be diminished as well. The underlying causes for the crowding out of the legal tender also are familiar from dollarization episodes: Loss of trust in the central bank and the stability of the legal tender, or a desire of the transacting parties to hide their identity if the central bank can monitor payments in the domestic currency but not otherwise.

Blockchain facilitated transactions denominated in domestic currency have the potential to affect central bank operations much more directly. To leverage the efficiency of domestic currency denominated blockchain transactions between financial institutions it is in the interest of banks to have the central bank on board: The domestic currency denominated krypto currency should ideally be base money or a perfect substitute to it, directly exchangeable against central bank reserves. For when perfect substitutability is not guaranteed then the payment associated with the transaction eventually requires clearing through the traditional central bank managed clearing mechanism and as a consequence, the gain in speed and efficiency is relinquished. Of course, building an interface between the blockchain and the central bank’s clearing system could constitute a first step towards completely dismantling the latter and shifting all central bank managed clearing to the former.

Why would central banks want to join forces? If they don’t, they risk being cut out from transactions denominated in domestic currency and to end up monitoring only a fraction of the clearing between market participants. Central banks are under pressure to keep “their” currencies attractive. For the same reason (as well as for others), I propose “Reserves for All”—letting the general public and not only banks access central bank reserves (here, here, here, and here).

In the FT, Philip Stafford reports about a digital currency initiative by the Bank of Canada and commercial banks. It

will involve issuing, transferring and settling central bank assets on a distributed ledger via a token named CAD-Coin.

But:

The Bank of Canada said the experiment was a proof-of-concept and confined to interbank payment systems. … “None of our experiments are to develop central-bank issued e-money for use by the general public.”