John Keitz compares the use of public transportation across US cities. Public transportation is used more intensively in densely populated urban areas.

ECB Balance Sheet Policy

A blog post in Sober Look discusses recent ECB actions and the outlook.

“Toward a Run-Free Financial System”

In the tenth chapter of “Across the Great Divide: New Perspectives on the Financial Crisis,” John Cochrane argues that at its core, the financial crisis was a run and thus, policy responses should focus on mitigating the risk of runs (blog posts by Cochrane on the same topic can be found here and here). Some excerpts:

… demand deposits, fixed-value money-market funds, or overnight debt … [should be] backed entirely by short-term Treasuries. Investors who want higher returns must bear price risk. …

Banks can still mediate transactions, of course. For example, a bank-owned ATM machine can deliver cash by selling your shares in a Treasury-backed money market fund … Banks can still be broker-dealers, custodians, derivative and swap counterparties and market makers, and providers of a wide range of financial services, credit cards, and so forth. They simply may not fund themselves by issuing large amounts of run-prone debt.

If a demand for separate bank debt really exists, the equity of 100 percent equity-financed banks can be held by a downstream institution or pass-through vehicle that issues equity and debt tranches. That vehicle can fail and be resolved in an hour …

Rather than outlawing short-term debt, Cochrane suggests to levy corrective taxes on run-prone liabilities. Moreover:

… technology allows us to overcome the long-standing objections to narrow banking. Most deeply, “liquidity” no longer requires that people hold a large inventory of fixed-value, pay-on-demand, and hence run-prone securities.

… electronic transactions can easily be made with Treasury-backed or floating-value money-market fund shares, in which the vast majority of transactions are simply netted by the intermediary. … On the supply end, $18 trillion of government debt is enough to back any conceivable remaining need for fixed-value default-free assets.

Cochrane rejects the claim that the need for money-like assets can only be met by banks that “transform” maturity or liquidity. He argues that current regulation reflects a history of piecemeal responses that triggered the need for additional measures; and he points out that the shadow banking system creates run risks because a “broker-dealer may have used your securities as collateral for borrowing” to fund proprietary trading.

Cochrane debunks crisis lingo and clarifies links between aggregate variables:

The only way to consume less and invest less is to pile up government debt. So a “flight to quality” and a “decline in aggregate demand” are the same thing.

He questions the need for fixed value securities other than short-term government debt as means of payment or savings vehicle; offers a short history of financial regulation; and deplores regulatory discretion.

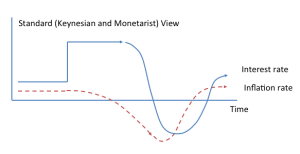

Do Higher Nominal Interest Rates Raise Inflation?

In several blog posts (here and here), John Cochrane mulls over the Fisher equation and the stability properties of the variables in the equation:

I think I can boil down the issue to this question: If the central bank pegs the nominal rate at a fixed value, is the economy eventually stable, converging to the interest rate peg minus the real rate? Or is it unstable, careening off to hyperinflation or deflationary spiral?

He offers a series of instructive graphs to illustrate the inflation dynamics under the assumption that inflation dynamics are (i) stable (Neo-Fisherian view) or (ii) unstable (standard view):

Interest rate increase pushes up inflation, maybe with a delay.

Inflation shock eventually dies out even if interest rate does not respond.

Interest rate increase pushes down inflation, on an accelerating path …

… unless monetary policy steps in and undoes the initial tightening.

Inflation shock does not die out …

… unless the interest rate responds.

Which model is the right one? The US, Japan and other countries have been at the zero lower bound for a while—without an explosion in inflation. John Cochrane interprets this fact as evidence in favour of stability. And he offers this nice analogy:

Think of holding a broom upside down. That’s the standard view of interest rates (on the broom handle) and inflation (the broom). Anytime the Fed sees inflation moving, it needs to quickly move interest rates even more to keep inflation from toppling over — the Taylor rule. To raise inflation, the Fed needs first to lower interest rates, get the broom to start toppling in the inflation direction, then swiftly raise rates, finally raising them even more to re-stabilize the broom.

The neo-Fisherian view says the Fed is holding the broom right side up, though perhaps in a gale. To move the bottom to the left, move the top to the left, and wait. But alas, the broom sweeper has thought it was unstable all these years, so has been moving the handle around a lot.

“How Is the System Safer? What More Is Needed?”

In the ninth chapter of “Across the Great Divide: New Perspectives on the Financial Crisis,” Martin Baily and Douglas Elliott argue that significant progress has been made in safeguarding financial stability:

- Due to higher bank capital requirements, the FDIC can intervene before equity is wiped out.

- Liquidity requirements work in the same direction and render fire sales less likely.

- Easier resolution of distressed financial institutions helps to shield taxpayers when a bank fails.

- Better macro prudential oversight helps to manage systemic risks.

The authors discuss these dimensions in much detail.

“Mistakes Made and Lessons (Being) Learned”

In the seventh chapter of “Across the Great Divide: New Perspectives on the Financial Crisis,” Peter Fisher argues that the Fed’s mandate should be reviewed:

- The Fed did not address leverage early enough. In the future, monetary policy should weigh financial stability objectives more strongly—at the cost of employment and inflation objectives.

- Moral hazard should be addressed before, not during the crisis.

- “Since the end of the financial crisis, the Fed is making the mistake of conceiving of its mandate over too short—and too narrow—a horizon. This permits the Fed to avoid articulating the difficult intertemporal trade-offs that it is making.”

- The Fed’s mandate is not crystal clear and has been interpreted differently over the years. In light of the new experiences, it should be clarified or adjusted.

“The Federal Reserve’s Role: Actions Before, During, and After the 2008 Panic in the Historical Context of the Great Contraction”

In chapter six of “Across the Great Divide: New Perspectives on the Financial Crisis,” Michael Bordo argues that the Fed misinterpreted the experience of the Great Depression when acting during the financial crisis. Insolvency rather than illiquidity fears were central to the great recession.

“Causes of the Financial Crisis and the Slow Recovery”

In the third chapter of “Across the Great Divide: New Perspectives on the Financial Crisis,” John Taylor argues that monetary policy, regulatory policy, and an ad hoc bailout policy caused the financial crisis:

- Monetary policy was too loose before the crisis.

- “[R]egulators permitted violations from existing safety and soundness rules.”

- An “on-again, off-again bailout policy … created more instability.”

The policy responses during the crisis saw more—counter productive—temporary and discretionary measures. Taylor argues that the Reinhart-Rogoff “weak recovery is normal” and the Summers “secular stagnation” views are inconsistent with the data.

“How Efforts to Avoid Past Mistakes Created New Ones: Some Lessons from the Causes and Consequences of the Recent Financial Crisis”

In the first chapter of “Across the Great Divide: New Perspectives on the Financial Crisis,” Sheila Bair and Ricardo Delfin argue that regulatory responses to past crises sow the seeds of the next ones:

- The “Greenspan put” fostered risk-taking and overconfidence.

- Low interest rates and the search for yield led to a lowering of lending standards and stronger demand for mortgages; a rise in housing wealth accompanied falling household incomes. The Fed’s strong policy response to the Great Recession may create new risks.

- The 1980s savings and loans crisis led to stronger reliance on the originate to distribute model and securitisation of mortgages. Market participants lost sight of the risks. Regulatory incentives led banks to take the securitised loans back on their balance sheets and additional sources of maturity mismatch arose from strong reliance on short-term funding.

- The “self-correcting markets myth” led Congress to deregulate financial services. The Gramm-Leach-Bliley Act fostered competition and consolidation; the Commodity Futures Modernization Act loosened oversight over the OTC derivatives market. Financial regulators also relaxed restrictions; Basel II replaced standardised regulator-set capital charges with internal models of banks.The Dodd-Frank Act reversed this trend, allowing for more discretion and micro-management.

- The pre-crisis incentives led to large, “too-big-to-fail” institutions and bred moral hazard. Dodd-Frank improve things, by establishing consolidated oversight, living will requirements, enhanced prudential standards and enabling the FDIC to resolve systemic entities that cannot be resolved safely in bankruptcy. Clearing houses may require more regulation.

Perspectives on the Financial Crisis

A Hoover Press book edited by Martin Baily and John Taylor collects articles about the financial crisis. The contributions in “Across the Great Divide: New Perspectives on the Financial Crisis” include (with links to PDF files):

- Introduction, Martin Neil Baily and John B. Taylor

- Chapter 1: How Efforts to Avoid Past Mistakes Created New Ones: Some Lessons from the Causes and Consequences of the Recent Financial Crisis, Sheila C. Bair and Ricardo R. Delfin

- Chapter 2: Low Equilibrium, Real Rates, Financial Crisis, and Secular Stagnation, Lawrence H. Summers

- Chapter 3: Causes of the Financial Crisis and the Slow Recovery: A Ten-Year Perspective, John B. Taylor

- Chapter 4: Rethinking Macro: Reassessing Micro-foundations, Kevin M. Warsh

- Chapter 5: The Federal Reserve Policy, Before, During, and After the Fall, Alan S. Blinder

- Chapter 6: The Federal Reserve’s Role: Actions Before, During, and After the 2008 Panic in the Historical Context of the Great Contraction, Michael D. Bordo

- Chapter 7: Mistakes Made and Lesson (Being) Learned: Implications for the Fed’s Mandate, Peter R. Fisher

- Chapter 8: A Slow Recovery with Low Inflation, Allan H. Meltzer

- Chapter 9: How Is the System Safer? What More Is Needed?, Martin Neil Baily and Douglas J. Elliot

- Chapter 10: Toward a Run-free Financial System, John H. Cochrane

- Chapter 11: Financial Market Infrastructure: Too Important to Fail, Darrell Duffie

- Chapter 12: “Too Big to Fail” from an Economic Perspective, Steve Strongin

- Chapter 13: Framing the TBTF Problem: The Path to a Solution, Randall D. Guynn

- Chapter 14: Designing a Better Bankruptcy Resolution, Kenneth E. Scott

- Chapter 15: Single Point of Entry and the Bankruptcy Alternative, David A. Skeel Jr.

- Chapter 16: We Need Chapter 14—And We Need Title II, Michael S. Helfer

- Remarks on Key Issues Facing Financial Institutions, Paul Saltzman

- Concluding Remarks, George P. Shultz

- Summary of the Commentary, Simon Hilpert

Myopia in East Asia

The Economist reports about a rising share of teenagers in East Asia that suffer from myopia.

The biggest factor in short-sightedness is a lack of time spent outdoors. Exposure to daylight helps the retina to release a chemical that slows down an increase in the eye’s axial length …

Once they start school, Chinese children spend about an hour a day outside, compared with three or four hours for Australian ones.

The ECB and Ireland: Bailout But no Bail-In

Vincent Boland and Peter Spiegel suggest in the FT that the ECB coerced Ireland into applying for a bailout in 2010, based on letters recently released by the ECB. The ECB, in contrast, argues that the bailout was unavoidable anyway, and that the Irish Minister for Finance shared this view. In a Q&A section on its website the ECB writes:

While the ECB always acted within its remit and in line with rules established for the whole of the euro area, there are limits to the support that the Eurosystem can provide to banks in the Member States. … First, collateral has to be adequate; and second, counterparts have to be financially sound and solvent. The letter dated 15 October 2010 from the former ECB President recalled these rules and their implications for Ireland. … [Another letter dated 19 November 2010] explained the conditions under which further provisions of ELA to Irish financial institutions could be authorised. In his already public reply of 21 November 2010, the Irish Minister for Finance stated that he fully understood the concerns raised by the ECB Governing Council.

The ECB also addresses the question why it opposed the bail-in of bondholders in 2010:

As regards the possible bailing-in of senior debt in late 2010, it is important to recall the words of EU leaders in a European Union statement of 29 October 2010 and during the G20 meeting in South Korea on 12 November, according to which burden-sharing of senior debt would not be applied until mid-2013. … Furthermore, the necessary EU governance tools to address the bail-in of creditors, which were set out in the Bank Recovery and Resolution Directive (BRRD) and have been fully endorsed by the ECB, were not available in late 2010. … any potential burden-sharing of senior debt in the immediate aftermath would first and foremost have had negative spillover effects on the financial stability of Ireland, as well as on other European countries.

Conference on “Asset Price Fluctuations and Economic Policy” at the Study Center Gerzensee

Jointly with the Journal of Monetary Economics and the Swiss National Bank, the Study Center Gerzensee organises a conference on asset price fluctuations. The program can be viewed here.

Luxembourg’s Tax Agreements with International Companies

The International Consortium of Investigative Journalists reports about the tax agreements between Luxembourg and major international companies that helped these companies avoid taxes. The Consortium’s key findings:

Pepsi, IKEA, AIG, Coach, Deutsche Bank, Abbott Laboratories and nearly 340 other companies have secured secret deals from Luxembourg that allowed many of them to slash their global tax bills.

PricewaterhouseCoopers has helped multinational companies obtain at least 548 tax rulings in Luxembourg from 2002 to 2010. These legal secret deals feature complex financial structures designed to create drastic tax reductions. The rulings provide written assurance that companies’ tax-saving plans will be viewed favorably by Luxembourg authorities.

Companies have channeled hundreds of billions of dollars through Luxembourg and saved billions of dollars in taxes. Some firms have enjoyed effective tax rates of less than 1 percent on the profits they’ve shuffled into Luxembourg.

Many of the tax deals exploited international tax mismatches that allowed companies to avoid taxes both in Luxembourg and elsewhere through the use of so-called hybrid loans.

In many cases Luxembourg subsidiaries handling hundreds of millions of dollars in business maintain little presence and conduct little economic activity in Luxembourg. One popular address – 5, rue Guillaume Kroll – is home to more than 1,600 companies.

Hybrid loans combine the advantages of interest bearing debt and dividend paying stock. Profits are treated as interest payments (deductible for tax purposes) in Luxembourg and as profits (eligible for tax exemption) in the parent company’s country.

Hayek’s “Why I am not a Conservative”

Cass Sunstein interprets Friedrich von Hayek’s “Why I am not a Conservative” in BloombergView.

According to Sunstein, Hayek endorsed Conservatives’ skepticism about rapid change and social engineering and appreciated their understanding of the value of institutions that grow out of decentralised interaction rather than centralised social design. At the same time, Hayek saw Conservatives as objecting to novelty as such and complained that they did not “welcome the same undesigned change from which new tools of human endeavor will emerge.” And he complained that they are far too fond of established authority (“The conservative does not object to coercion or arbitrary power so long as it is used for what he regards as the right purposes.”) and have difficulty cooperating with people who don’t share their moral values. Sunstein: Instead of conservatism, Hayek argued for a principled commitment to liberty, “directed against popular prejudices, entrenched positions and firmly established privileges.”

The IMF Favours Fiscal Stimulus over Prudent Fiscal Policy—Or Not?

Robin Harding reports in the Financial Times about the IMF’s critical review of its own policy recommendations in 2010. The IMF’s independent evaluation office commends the fund’s lending at the time but criticises the advice to cut budget deficits. However, important IMF officials dissent. According to the FT, (current, but not then) managing director Christine Lagarde notes that “[a]s the report acknowledges, this assessment is benefiting from hindsight.” And: “Considering the information and growth forecasts available in 2010, I strongly believe that advising economies with rapidly rising debt burdens to move toward measured consolidation was the right call to make.”

Liberal and Conservative Professions and Industries

Andy Kiersz and Hunter Walker report in Businessinsider about a Crowd Pack analysis of US federal campaign contributions.

As far as donors are concerned, the analysis suggests that the media, entertainment and tech industries as well as academics tend to support “liberal” candidates. The same holds true, somewhat less pronounced, for the pharmaceutical industry and lawyers.

In contrast, farmers as well as representatives of the building and construction, mining, oil, gas and coal and tobacco industries mostly support “conservative” candidates. Other industries appear very polarised.

ECB Takes up Banking Supervision

René Höltschi reviews in the NZZ how the ECB became European bank supervisor within just two years. The article also surveys the pillars of the European Banking Union—supervision, resolution and safety nets—and its fundament, the Single Rulebook.

Expat Country Ranking

Expats rank host countries for HSBC. Switzerland comes first.

Reserve Requirements

Pablo Federico, Carlos Vegh and Guillermo Vuletin discuss legal reserve requirements in an NBER working paper.

Their data set covers 15 industrial and 37 developing countries over the period 1970–2011. Developing countries typically actively manage legal reserve requirements in the sense of adjusting them at least once over the business cycle. Industrialised countries don’t. None of the latter has changed the requirements after 2004, and many have no requirements at all. Among the active countries, most conduct a counter cyclical reserve requirements policy, often in contrast to a more pro cyclical monetary policy along other dimensions.

Quantitative Easing

James Hamilton reviews the short- and long-term effects of the Fed’s quantitate easing in Econbrowser: Clear effect in the very short term, nothing as clear in the longer term.

Liquidity of Exchange-Traded Funds

The Economist explains how “authorised participants” provide liquidity for exchange-traded funds and why regulators are worried about the risk of fire sales.

Anonymous Internet

The Economist reviews the anonymous internet and the goods and services on sale thereon: Drugs, weapons, killings and the like.

Quantitative Easing

The Economist reviews the success or not of the Fed’s quantitative easing programs.

House Prices since 1870

Katharina Knoll, Moritz Schularick and Thomas Steger discuss data on long-run house price trends in Vox. House-price-to-income ratios have risen after World War II. Rising land prices played a crucial role.

This is their figure 2: