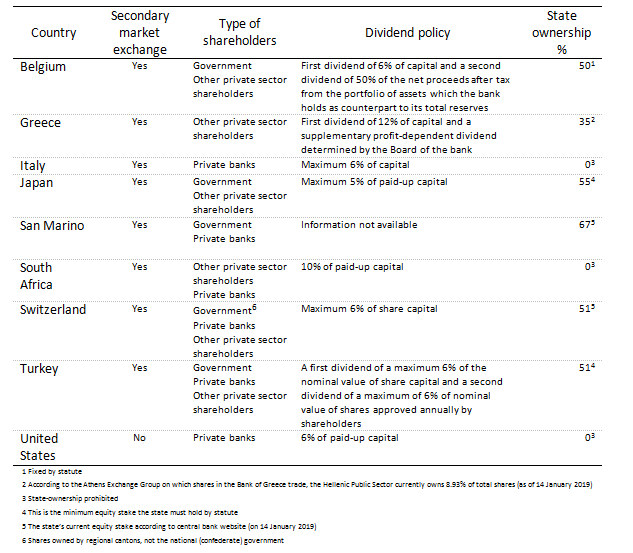

On Bank Underground, David Bholat and Karla Martinez Gutierrez described (in October 2019) the ownership structures of central banks across the world. From their post:

Figure 4: Institutional detail on central banks not fully owned by governments

On Bank Underground, David Bholat and Karla Martinez Gutierrez described (in October 2019) the ownership structures of central banks across the world. From their post:

Figure 4: Institutional detail on central banks not fully owned by governments

CEPR Discussion Paper 12755, February 2018. PDF. (Personal copy.)

This paper reviews theoretical results on financial policy. We use basic accounting identities to illustrate relations between gross assets and liabilities, net debt positions and the appropriation of (primary) budget surplus funds. We then discuss Ramsey policies, answering the question how a committed government may use financial instruments to pursue its objectives. Finally, we discuss additional roles for financial policy that arise as a consequence of political frictions, in particular lack of commitment.

Journal of International Economics 99(S1), March 2016, with Harris Dellas. PDF.

We develop a sovereign debt model with heterogeneous creditors (private and official) where the probability of default depends on both the level and the composition of debt. Higher exposure to official lenders improves incentives to repay due to more severe sanctions but it is also costly because it lowers the value of the sovereign’s default option. The model can account for the co-existence of private and official lending, the time variation in their shares in total debt as well as the low rates charged on both. It also produces intertwined default and debt-composition choices.

In a Vox blog post (that complements another post on Greece), Jeremy Bulow and Ken Rogoff review the academic discussion on a long-standing question—why sovereigns repay their external debt.

Bulow and Rogoff distinguish between

[t]he ‘reputation approach’ pioneered by Eaton and Gersovitz (1981) which builds on Hellwig (1977);

and the ‘direct punishments’ bargaining-theoretic approach of Bulow and Rogoff (1988b, 1989a) which in turn builds on Cohen and Sachs (1986).

They argue that the latter approach—attributing enforceable rights in foreign country courts to creditors—better explains observed outcomes.

[The] direct punishment/bargaining approach lends itself very naturally to incorporating moral hazard; …

reputation models suggest [counter factually] that the governing law of the debt is irrelevant;

[i]n standard reputation for repayment models, write-downs are decided unilaterally—creditors’ particular concerns do not really matter; …

[t]he interests and welfare of unrelated third parties does not matter in standard reputation models; …

[r]eputational debtors borrow in bad times and re-pay in good times, for purposes of income smoothing; [d]efaults, if they are to take place, occur in good times … In reality, many countries borrow as much as they can whenever they can. … Debt crises occur when countries do badly and creditors decide they want to reduce their loan exposure. To some extent, this issue can be addressed by assuming that income shocks are permanent and not transitory, but it remains difficult to rationalise country borrowing only on the threat of lost consumption smoothing. …

[c]reditor identity doesn’t matter; …

[u]nder … general assumptions, the existence of [the option to put savings abroad] leads to the unravelling of any purely reputational equilibrium.

Bulow and Rogoff add that

[a]nother important issue … is that in practice, sovereign debt renegotiations focus very much on the flow of repayments, and much less on how the stock of debt evolves. This is precisely because all sides realise that any future promises can be renegotiated.

S. M. Ali Abbas, Laura Blattner, Mark De Broeck, Asmaa El-Ganainy and Malin Hu report in Vox about their debt structure database spanning the period 1900–2011 and covering Australia, Austria, Belgium, Canada, France, Germany, Ireland, Italy, the Netherlands, Spain, Sweden, the UK, and the US. Data is disaggregated along the following dimensions: Currency; maturity (of local currency debt); marketability; holders (non-residents, national central bank, domestic commercial banks, rest).

Their main findings are:

They suggest that countries mainly followed two strategies to reduce debt quotas. One, based on fiscal consolidation and moderate inflation, going hand in hand with long maturities. The other, based on high inflation and reliance on debt holdings by captive domestic investors, going hand in hand with shorter maturities.

Link to the data.