SRF, Tagesgespräch, June 16, 2016. HTML with link to MP3.

- Half-hour-long interview on the Swiss news channel.

- Topics include monetary policy, exchange rates, financial stability, Brexit.

SRF, Tagesgespräch, June 16, 2016. HTML with link to MP3.

Finanz und Wirtschaft, April 30, 2016. PDF. Ökonomenstimme, May 6, 2016. HTML.

The winners and losers of the current monetary environment are not that easy to identify. Investors holding long-term, non-indexed debt gain as unexpectedly low inflation shifts wealth from borrowers to lenders. Governments suffer from increased real debt burdens and reduced revenue due to effectively lower capital income tax rates. Policies that succeed in affecting the real exchange rate entail redistribution.

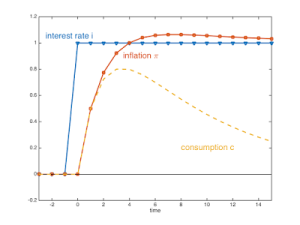

On his blog, John Cochrane offers a stripped down model and some intuition for why inflation would rise after an increase in the interest rate. The model features the usual Euler (IS) equation and a Mickey Mouse Phillips curve—inflation is proportional to consumption (or output). The intuition:

During the time of high real interest rates — when the nominal rate has risen, but inflation has not yet caught up — consumption must grow faster [the Euler equation, DN]. … Since more consumption pushes up prices, giving more inflation, inflation must also rise during the period of high consumption growth.

Also:

I really like that the Phillips curve here is so completely old fashioned. This is Phillips’ Phillips curve, with a permanent inflation-output tradeoff. That fact shows squarely where the neo-Fisherian result comes from. The forward-looking intertemporal-substitution IS equation is the central ingredient.

A slightly more plausible model with an accelerationist Phillips curve and very slowly adjusting adaptive expectations yields the following responses to an increase in the nominal interest rate:

John writes:

As you can see, we still have a completely positive response. Inflation ends up moving one for one with the rate change. Consumption booms and then slowly reverts to zero. …

The positive consumption response does not survive with more realistic or better grounded Phillips curves. With the standard forward looking new Keynesian Phillips curve inflation looks about the same, but output goes down throughout the episode: you get stagflation.

A November 2015 paper on the topic by James Bullard.

A critique by Mariana García-Schmidt and Michael Woodford in an NBER working paper. Abstract:

We illustrate a pitfall that can result from the common practice of assessing alternative monetary policies purely by considering the perfect foresight equilibria (PFE) consistent with the proposed rule. In a standard New Keynesian model, such analysis may seem to support the “Neo-Fisherian” proposition according to which low nominal interest rates can cause inflation to be lower. We propose instead an explicit cognitive process by which agents may form their expectations of future endogenous variables. Under some circumstances, a PFE can arise as a limiting case of our more general concept of reflective equilibrium, when the process of reflection is pursued sufficiently far. But we show that an announced intention to fix the nominal interest rate for a long enough period of time creates a situation in which reflective equilibrium need not resemble any PFE. In our view, this makes PFE predictions not plausible outcomes in the case of such policies. Our alternative approach implies that a commitment to keep interest rates low should raise inflation and output, though by less than some PFE analyses apply.

On his blog, Stephen Williamson addresses “Neo-Fisherian Denial.” Williamson starts with the model analyzed by Cochrane (see above) featuring a Mickey Mouse Phillips curve. He argues:

[This] NK model actually doesn’t conform to conventional central banking beliefs about how monetary policy works. What’s going on? … an increase in the current nominal interest rate will increase the real interest rate, everything else held constant. This implies that future consumption (output) must be higher than current consumption, for consumers to be happy with their consumption profile given the higher nominal interest rate. But, it turns out that this is achieved not through a reduction in current output and consumption, but through an increase in future output and consumption. This serves, through the Phillips curve mechanism, to increase future inflation relative to current inflation. Then, along the path to the new steady state, output and inflation increase.

Williamson recalls the “perils” of Taylor rules. And he addresses the critique by Garcia-Schmidt and Woodford:

Some people (e.g. Garcia-Schmidt and Woodford) have argued that Neo-Fisherian results go out the window in NK models under learning rules. As was shown above, these models are always fundamentally Fisherian in that any monetary policy rule has to somehow adhere to Fisherian logic on average – basically the long-run nominal interest rate is the inflation anchor. But there can also be learning rules that give very Fisherian results. …

Williamson also argues that other (non-Keynesian) monetary models give neo-Fisherian results as well.

A few years ago, also on his blog, Stephen Williamson argued that lowering the interest rate (by engaging in QE) might also affect the real interest rate:

… short-run liquidity effects are short-lived. Further, my work shows that there is another liquidity effect, associated with the interest bearing liquid assets, that causes the long run real rate to increase as a result of QE. … which implies lower inflation.

Further, there are other forces in play … The destruction of private sources of collateral and the shaky state of sovereign governments in parts of the world gave U.S. government debt a large liquidity premium – i.e. those things reduced real interest rates. As those effects go away over time, real rates of return will rise, shifting up the long-run Fisher relation, and reducing inflation if the Fed keeps the nominal interest rate at the zero lower bound.

In a paper, Peter Rupert and Roman Sustek dig deeper. In the abstract they write:

The monetary transmission mechanism in New-Keynesian models is put to scrutiny, focusing on the role of capital. We demonstrate that, contrary to a widely held view, the transmission mechanism does not operate through a real interest rate channel. Instead, as a first pass, inflation is determined by Fisherian principles, through current and expected future monetary policy shocks, while output is then pinned down by the New-Keynesian Phillips curve. The real rate largely only reflects consumption smoothing. In fact, declines in output and inflation are consistent with a decline, increase, or no change in the ex-ante real rate.

Addendum (May 11–12, 2016): In the abstract of their NBER working paper, Julio Garín, Robert Lester and Eric Sims write:

Increasing the inflation target in a textbook New Keynesian (NK) model may require increasing, rather than decreasing, the nominal interest rate in the short run. We refer to this positive short run co-movement between the nominal interest rate and inflation conditional on a nominal shock as Neo-Fisherianism. We show that the NK model is more likely to be Neo-Fisherian the more persistent is the change in the inflation target and the more flexible are prices. Neo-Fisherianism is driven by the forward-looking nature of the model. Modifications which make the framework less forward-looking make it less likely for the model to exhibit Neo-Fisherianism. As an example, we show that a modest and empirically realistic fraction of “rule of thumb” price-setters may altogether eliminate Neo-Fisherianism in the textbook model.

In his 2008 textbook, Jordi Gali discusses the role of the persistence of monetary policy shocks (page 51). If it is sufficiently persistent, a contractionary monetary policy shock raises the real rate (and lowers output) but decreases the nominal rate, due to the

decline in inflation and the output gap more than offsetting the direct effect [of the shock].

In his blog, Ben Bernanke discusses the merits of longer-term interest rate targeting as a monetary policy tool.

A lot would depend on the credibility of the Fed’s announcement. If investors do not believe that the Fed will be successful at pushing down the two-year rate … they will immediately sell their securities of two years’ maturity or less to the Fed. … the Fed could end up owning most or all of the eligible securities, with uncertain consequences for interest rates overall. On the other hand, if the Fed’s announcement is fully credible, the prices of eligible securities might move immediately to the targeted levels, and the Fed might achieve its objective without acquiring many securities at all.

… A policy of targeting longer-term rates is related to quantitative easing in that both involve buying potentially large quantities of securities. An important difference is that one sets a quantity and the other sets a price. … Concerns about “losing control of the balance sheet” were a factor behind the Fed’s choice of quantitative easing over rate targets while I was chairman.

Conceivably, QE and rate-pegging could be used together … with QE working through reduced risk premiums while the rate peg operates indirectly by affecting the expected path of short-term interest rates. … The principal limitations of rate pegs are similar to those of forward guidance: Both tools are relatively less effective at affecting interest rates at longer maturities, and even at shorter horizons both must be consistent with a credible or “time-consistent policy” path for short-term interest rates.

On his blog, Urs Birchler offers different perspectives on the question whether the Swiss National Bank (SNB) is obliged to pay out banks’ reserves in cash.

In his blog, John Cochrane registers disagreement with Larry Summers and reiterates his own argument that in a liquidity trap, interest rate policy does not have a liquidity effect and thus, only a long-run “expected inflation” or “Fisher” effect:

When the liquidity effect is absent, the expected inflation effect is all that remains. Inflation must follow interest rates.

The German Ministry of Finance has decided (p. 55, nr. 129a) that for tax purposes, negative interest rates are not to be treated as the opposite of positive interest rates. Instead they are considered fees. This treatment lowers taxable income to a lesser extent than would be the case under a symmetric treatment.

Finanz und Wirtschaft, January 20, 2016. PDF. Ökonomenstimme, January 21, 2016. HTML.

The public’s perception of central banks has changed during the crisis—and has created expectations that cannot be met. Beyond the buzzwords, the fundamental options for monetary policy makers are the same as always.

In the 17th Geneva Report on the World Economy (Low for Long? Causes and Consequences of Persistently Low Interest Rates), Charles Bean, Christian Broda, Takatoshi Ito and Randall Kroszner take up the theme of a recent report by the White House Council of Economic Advisors (see previous blog post). In the abstract, some of the authors’ conclusions are summarized as follows:

… aggregate savings propensities should fall back as the bulge of high-saving middle-aged households moves through into retirement and starts to dissave; this process has already begun. And though Chinese financial integration still has some way to run, the net flow of Chinese savings into global financial markets has already started to ebb as the pattern of Chinese growth rotates towards domestic demand rather than net exports. Finally, the shifts in portfolio preferences may partially unwind as investor confidence slowly returns. But … the time scale over which such a rebound in real interest rates will be manifest is highly uncertain and will be influenced by longer-term fiscal and structural policy choices.

One chapter in the report discusses the Japanese experience.

A report by the White House Council of Economic Advisors surveys long-term interest rates. The “key takeaways” include:

Real and nominal interest rates in the United States have been on a steady decline since the mid-1980s. Declining interest rates are a global phenomenon. … [F]orecasters largely missed the secular decline of the last three decades.

The Ramsey growth model implies a link between labor productivity growth, per capita consumption growth and the real (inflation-adjusted) interest rate. Historically, periods of low real long-term interest rates have tended to coincide with low labor productivity growth. Projections of labor productivity growth, while imprecise, suggest 10-year real interest rates in the range of 1.5 to 3.5 per cent.

Asset-pricing models that incorporate risk suggest that the long-run nominal interest rate is the sum of expected future short-term real rates, expected future inflation rates, and a term premium. The 10-year rate in ten years that forward transactions in nominal Treasuries imply is currently 3.1 percent. Forward transactions in the market for TIPS suggest a long-term real rate just above 1.00 percent in ten years. Adding the CPI inflation rate implied by the Federal Reserve’s PCE inflation target would imply a forward nominal interest rate of 3.25 percent. The term premium in nominal Treasuries is currently estimated to be near zero, with a 2005-2014 mean of 1 percent. These components together suggest a 10-year nominal interest rate in the range of 3.1 (forward Treasuries) to 4.6 percent (based on FOMC forecasts of the long-run federal funds rate).

In a world with financially integrated national capital markets, the general level of world interest rates is determined by the equality of the global supply of saving and global investment demand. Capital markets of advanced economies are now tightly integrated while emerging market economies are becoming increasingly integrated into the global financial system. Low-income economies remain partially segmented from the global capital market. As a consequence of increasing international market integration, long-term real and nominal interest rates are increasingly moving in tandem and have declined along with U.S. rates. Nominal interest rates also tend to be correlated across countries though differences in inflation expectations can produce differences in nominal rates. In a world with uncertainty, global long-term real and nominal interest rates will include risk premiums that can reflect country-specific risk factors. Strong economic linkages, however, reinforce substantial correlation in countries’ long-term bond risk premiums.

Long-term interest rates are lower now than they were thirty years ago, reflecting an outward shift in the global supply curve of saving relative to global investment demand. It remains an open question whether the underlying factors producing current low rates are transitory, or imply long-run equilibrium long-term interest rates lower than before the financial crisis. Factors that are likely to dissipate over time—and therefore could lead to higher rates in the future—include current fiscal, monetary, and exchange rate policies; low-inflation risk as reflected in the term premium; and private-sector deleveraging in the aftermath of the global financial crisis. Factors that are more likely to persist—suggesting that low interest rates could be a long-run phenomenon—include lower forecasts of global output and productivity growth, demographic shifts, global demand for safe assets outstripping supply, and the impact of tail risks and fundamental uncertainty.

In a recent NBER working paper (“Discounting Pension Liabilities: Funding Versus Value”), Jeffrey Brown and George Pennacchi discuss the appropriate choice of discount factor to discount pension liabilities. They conclude that it depends.

… if the objective is to measure pension under- or over- funding, a default-free discount rate should always be used, even if the liabilities are themselves not default-free. If, instead, the objective is to determine the market value of pension benefits, then it is appropriate that discount rates incorporate default risk.

… the use of a default-free discount rate is informative to participants who want to know how much money the plan would need to be assured that the plan will be able to pay promised benefits. This would also be a relevant measure if the plan wished to offload its liabilities to an insurance company that intends to make good on the future benefit payments.

… there are also cases for which the market value of the liability is important. Current or potential plan participants might want to know the market value of pension liabilities (rather than the promised value) when they are making decisions about the value of pension benefits…

… the market value of the liability can have odd properties as a system of funding measurement: specifically, the size of the total (funded plus unfunded) liability can vary with the degree of funding, and that funding levels asymptotically approach 100 percent as assets approach zero.

Brown and George Pennacchi also discuss how the appropriate discount rate may be measured and how cost-of-living adjustments may be accounted for.

In a Federal Reserve Bank of New York staff report, Rodney Garratt, Antoine Martin, James McAndrews and Ed Nosal argue in favor of “Segregated Balance Accounts” (SBAs):

SBAs are accounts that a bank or depository institution (DI) could establish at its Federal Reserve Bank using funds borrowed from a lender. … the funds deposited in an SBA would be fully segregated from the other assets of the bank … only the lender of the funds could initiate a transfer out of an SBA; consequently, the borrowing bank could not use the reserves that fund an SBA for any purpose other than paying back the lender. … the loan made by the lender to the bank would be collateralized by the reserve balances in the SBA account.

The authors argue that SBAs could foster competition in money markets and

help strengthen the floor on overnight interest rates that is created by the payment of interest on excess reserves.

The proposal is related to topics I discussed in previous blog posts:

Ben Bernanke argues in his blog that it is not clear whether monetary policy fosters inequality. And if it did, other policy instruments should be used to address the resulting problems.

James McAndrews of the Federal Reserve Bank of New York doubts the merits of negative interest rates. He lists the following types of complications:

- Avoidance

- Legal and operational frictions

- Economic frictions

- Pass-through to market rates, and retail v. wholesale

- Effects of negative rates on the health of financial intermediaries

- Signal of deflation

- Public acceptance

SRF, Echo der Zeit, May 18, 2015. AUDIO, HTML.

Imperial College London (the business school’s Brevan Howard Centre), CEPR and the Swiss National Bank organized a conference on this topic in London.

Most of the speakers agreed that giving central banks the option to move interest rates much further into negative territory would be valuable; and that deposit rates lower than minus half a percent p.a. are difficult to sustain without triggering major cash withdrawals. There was less agreement on how to avoid such withdrawals. Some favored phasing out cash, as this would also render tax evasion and money laundering more difficult; others were unwilling to sacrifice the privacy benefits of cash. But many speakers emphasized that there are other possibilities to achieve the same objective. (See my earlier blog post.)

In a Vox column, Ken Rogoff argues that the world economy experiences a “debt supercycle” rather than the onset of secular stagnation in the West.

Rogoff argues that macroeconomic developments since the financial crisis are in line with historical experience, as documented in his book “This Time is Different” (with Carmen Reinhart): A large fall in output followed by a sluggish recovery; deleveraging; protracted higher unemployment; and a strong rise of the government debt quota are typical after a boom and bust of house prices and credit.

According to Rogoff, policy makers should have implemented more heterodox policies including debt write-downs; bank restructurings coupled with recapitalisations; and temporarily higher inflation targets. Rogoff supports the (in his view, orthodox) fiscal policy responses that were adopted but criticizes that many countries tightened prematurely.

Rogoff acknowledges that secular forces shape the macroeconomy, in particular population ageing; the stabilization of the female labor force participation rate; the growth slowdown in Asia; and the slowdown or acceleration (?) of technological progress. But

[t]he debt supercycle model matches up with a couple of hundred years of experience of similar financial crises. The secular stagnation view does not capture the heart attack the global economy experienced; slow-moving demographics do not explain sharp housing price bubbles and collapses.

Rogoff doesn’t accept low interest rates as an argument in favor of the secular stagnation view. Rather than reflecting demand deficiencies, low interest rates (if measured correctly—Rogoff expects a utility based interest rate measure to be higher) could reflect regulation (favoring low-risk borrowers and “knocking out other potential borrowers who might have competed up rates”) and to some extent central bank policies.

Rogoff argues that the global stock market boom poses a problem for the secular stagnation view. He proposes changed perceptions about the likelihood and cost of extreme events (Barro, Weitzman) as factors to explain both low real interest rates and the stock market boom (after an initial asset price collapse during the crisis).

Regarding policy prescriptions to expand public investment in light of the low interest rates, Rogoff notes that

it is highly superficial and dangerous to argue that debt is basically free. To the extent that low interest rates result from fear of tail risks a la Barro-Weitzman, one has to assume that the government is not itself exposed to the kinds of risks the market is worried about, especially if overall economy-wide debt and pension obligations are near or at historic highs already. [Moreover] one has to worry whether higher government debt will perpetuate the political economy of policies that are helping the government finance debt, but making it more difficult for small businesses and the middle class to obtain credit.

Rogoff considers rising inequality to be problematic (and a possible factor for higher savings rates):

Tax policy should be used to address these secular trends, perhaps starting with higher taxes on urban land, which seems to lie at the root of inequality in wealth trends

He concludes that the case for a debt supercycle is stronger than for secular stagnation:

[T]he US appears to be near the tail end of its leverage cycle, Europe is still deleveraging, while China may be nearing the downside of a leverage cycle.

In a Vox column, Michal Kobielarz, Burak Uras and Sylvester Eijffinger argue that the re-emergence of spreads between peripheral and core Eurozone countries at the beginning of the Greek crisis reflected contagion fears. They write:

… we explicitly model the endogenous bailout decision of the European Monetary Union. We assume that:

- A country that defaults on its sovereign debt can no longer remain in the EMU, unless it is bailed out;

- The union values each country’s membership and, therefore, suffers a loss if a country exits; and

- The marginal loss associated with allowing a country to leave the union is highest if that particular country is the first to leave (first-exit effect).

… once the first country is gone, letting a second country default and leave the union is not that costly anymore.

James Hamilton, Ethan Harris, Jan Hatzius and Kenneth West have computed historical time series for real interest rates in several countries (paper, blog post). The authors argue that there is significant uncertainty surrounding the equilibrium real rate—but no strong evidence for “secular stagnation.” They also argue that the uncertainty calls for inertial monetary policy. The paper includes many figures, for instance on this page a figure about US and UK real rates.

The Economist argues that negative interest rates appear not to spur inflation or growth but to weaken exchange rates. And they put pressure on banks.

The Swiss National Bank imposes negative interest rates on sight deposit account balances. The press release explains the details, including the calculation of exemption thresholds.

In the first and third of his Munich Lectures in Economics (and in an earlier oped in the FT), Kenneth Rogoff argued in favour of phasing out cash, at least high denominations and in some developed economies, see my post. Rogoff emphasised two beneficial consequences. First, the abolition of the zero lower bound on nominal interest rates and thus, the relaxation of a constraint on monetary policy. And second, the abolition of a means of payment that guarantees anonymity and thus, facilitates criminal transactions, money laundering, tax evasion and the like.

Both Rogoff and other academics have discussed the topic before. More than in academic papers, the end of cash has been the subject of intense debate in the blogosphere. By far the clearest discussion I know (and a very comprehensive one) is due to Willem Buiter in a blog post I summarise here. But the list of authors that have contributed to the discussion is much longer. Here is a selective overview:

When evaluating the merit of these discussions, it is important to distinguish between (i) introducing government provided electronic money and (ii) doing so in combination with an abolition of currency. Consider first the former option, namely to have the government grant the broad access to central bank reserves. This could be useful as it opened up the possibility to eliminate the risk of bank runs and as a consequence, abolish the fragile and costly system of deposit “insurance.” If, that is, most savers opted to move their deposits to the central bank rather than keeping them with commercial banks. If they didn’t, then governments would most likely feel obliged to continue bailing out depositors in failing commercial banks.

Another advantage of introducing government provided electronic money would be to eliminate a disgraceful contradiction in public policy. Mostly for reasons related to the deterrence of tax evasion, governments increasingly force citizens to use electronic means of payment although these are not legal tender and declare the use of currency illegal although currency is legal tender. In effect, governments force citizens to use liabilities of private companies for their transactions and in doing so, expose citizens to various financial risks. (These risks are partly borne by the public sector, due to deposit insurance, but that insurance creates other problems.) This absurd situation would end if the government provided a legal tender for electronic payments.

But granting the public access to central bank reserves could also create new problems. Inducing savers to move their deposits from commercial banks to the central bank would undermine a central activity of the former, namely deposit financed credit creation. Douglas Diamond and Philip Dybvig (1983) have shown in a classic article that the insurance characteristics of a deposit contract help improve outcomes relative to a situation without such a contract. How large are those benefits? And how large are they relative to the social costs of bank deposits, namely inefficiencies due to deposit insurance (moral hazard) and costs of run-induced fire sales and defaults?

There are other open questions. One concerns the transition from the current system where savers hold deposits at commercial banks, to a new system where they hold central bank reserves. Would the central bank assist commercial banks and convert deposits into reserve holdings? And if not, how could runs be avoided?

In addition, questions of a more technical nature would have to be addressed. Should banks (in the interbank market of reserves) and the general public (when paying their bills) use the same payment system? Or should the existing system linking the central bank and commercial banks be kept separate from a new, to be designed, system that serves consumers? How would monetary policy in this new world look like and how would the monetary transmission mechanism work? Would the central bank lend funds to households, and would it set the same policy rates for banks and the general public?

Turn next to the more ambitious proposal, namely to augment the introduction of government provided electronic money with an abolition of currency. This suggestion is more problematic, because the promised benefits are likely overstated and the costs misjudged. Consider first the benefits. As far as the relaxation of the zero lower bound is concerned, the fundamental objective—to lower real interest rates in order to incentivise earlier consumption and investment—cannot only be achieved through monetary policy but also by tax policy. A trend increase in consumption or value added tax rates acts like a low or negative real interest rate. And even if the objective is to relax constraints on monetary policy rather than relying on fiscal policy, this is feasible without eliminating cash altogether (and without moving to a higher inflation target which is costly for other reasons). As explained by Buiter, all that is needed is a floating exchange rate between reserves and cash. Killing currency amounts to an overkill unless one fears negative consequences due to such a floating exchange rate (see, e.g., Goodfriend, 2009, fn. 23).

As far as the second objective—limiting tax evasion as well as criminal and black economy transactions—is concerned, the elimination of currency is not a sufficient measure. True, those seeking anonymity would need to incur additional costs to secure it. But these additional costs would likely be mostly fixed costs (e.g., fees for incorporating a shell company in Nevada and hiring a lawyer). The implicit tax on black market activity due to the abolition of currency thus would be a regressive one and the revenues it generated would likely be smaller than hoped for. Professional criminals directing large operations could easily afford the higher cost of securing anonymity while the tax dodging middle class plumber in a badly run country could not.

Turning to the disadvantages, eliminating currency has severe consequences for privacy. (Buiter’s suggestion of ‘cash-on-a-chip cards’ could limit those consequences somewhat.) This point is widely acknowledged in the debate but it is not given sufficient weight. Related, forcing savers to hold means of payment—and a significant share of their savings—exclusively with a branch of the government (the central bank) might cause concern, particularly in countries with a history of expropriation.

Finally, there is a completely different reason to be worried about the prospect of putting an end to currency; when pointed to the proposal under question, some mothers I talked to immediately articulated it: In a world without physical money it is harder to acquire basic financial literacy skills. This might appear like a third-order problem, but is it?

John Cochrane argues in the Wall Street Journal that deflation fears are overblown. His main points are: