In several blog posts (here and here), John Cochrane mulls over the Fisher equation and the stability properties of the variables in the equation:

I think I can boil down the issue to this question: If the central bank pegs the nominal rate at a fixed value, is the economy eventually stable, converging to the interest rate peg minus the real rate? Or is it unstable, careening off to hyperinflation or deflationary spiral?

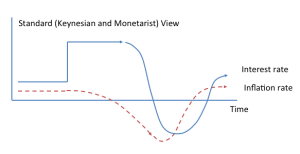

He offers a series of instructive graphs to illustrate the inflation dynamics under the assumption that inflation dynamics are (i) stable (Neo-Fisherian view) or (ii) unstable (standard view):

Interest rate increase pushes up inflation, maybe with a delay.

Inflation shock eventually dies out even if interest rate does not respond.

Interest rate increase pushes down inflation, on an accelerating path …

… unless monetary policy steps in and undoes the initial tightening.

Inflation shock does not die out …

… unless the interest rate responds.

Which model is the right one? The US, Japan and other countries have been at the zero lower bound for a while—without an explosion in inflation. John Cochrane interprets this fact as evidence in favour of stability. And he offers this nice analogy:

Think of holding a broom upside down. That’s the standard view of interest rates (on the broom handle) and inflation (the broom). Anytime the Fed sees inflation moving, it needs to quickly move interest rates even more to keep inflation from toppling over — the Taylor rule. To raise inflation, the Fed needs first to lower interest rates, get the broom to start toppling in the inflation direction, then swiftly raise rates, finally raising them even more to re-stabilize the broom.

The neo-Fisherian view says the Fed is holding the broom right side up, though perhaps in a gale. To move the bottom to the left, move the top to the left, and wait. But alas, the broom sweeper has thought it was unstable all these years, so has been moving the handle around a lot.