In a VoxEU post, Stefan Gerlach and Peter Kugler discuss the experience of Switzerland during the free banking era in the second half of the 19th century.

Tag Archives: Swiss National Bank

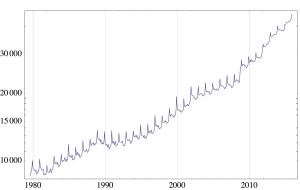

1000-Swiss-Franc Notes in Circulation

Central Bank Reserves: Debt vs. Equity

In jusletter.ch, Corinne Zellweger-Gutknecht argues that the legal status of central bank reserves is more equity- than debt-like—at least as far as the Swiss National Bank (SNB) is concerned. According to Zellweger-Gutknecht, reserves constitute debt only if the SNB is legally obliged to redeem them in exchange for central bank assets.

If the SNB purchases dollars against Swiss Francs in an open market operation, it creates reserves which are equity-like. But if it acquires dollars against Swiss Francs and is committed to engage in a reverse transaction in the future (a swap), then it (temporarily) creates reserves which are debt-like.

“Neue Geldpolitik, alte Optionen (New Monetary Policies, Old Policy Options),” FuW, 2016

Finanz und Wirtschaft, January 20, 2016. PDF. Ökonomenstimme, January 21, 2016. HTML.

The public’s perception of central banks has changed during the crisis—and has created expectations that cannot be met. Beyond the buzzwords, the fundamental options for monetary policy makers are the same as always.

Study Center in the “News”

On the blog insideparadeplatz, Marc Meyer criticizes the Swiss National Bank’s policies. He also proposes to convert the Study Center into a home for asylum seekers (since the academic staff and visitors are useless anyway) and to pay a large lump sum to each refugee. The motivation and the line of argument remain somewhat unclear.

“Soll die Nationalbank mehr riskieren? (A Riskier SNB?),” SRF, 2015

SRF, Rendez-vous, July 31, 2015. HTML and AUDIO.

- Risk and return but also liquidity.

SNB Balance Sheet

The Swiss National Bank has published information about its June 2015 balance sheet positions. The graph (excel file) depicts the evolution of foreign currency investments and sight deposits since 2010.

Source: SNB website.

“Der starke Franken (Strong Swiss Franc),” SRF, 2015

“Der starke Franken: Des einen Freud, des anderen Leid,” SRF 4 News, July 15, 2015. HTML, AUDIO.

- Who knows whether the Franc is overvalued.

- The SNB lost credibility in the short run (and this renders reinstating an exchange rate floor difficult), but not in the long run.

- Some of the current problems are problems of distribution. The SNB may not be the appropriate institution to address them.

- Switzerland wants an independent monetary policy. Here are some disadvantages.

The Euro/Swiss Franc Exchange Rate

Was it wise for the Swiss National Bank (SNB) to abandon the exchange rate floor vis-a-vis the Euro (EUR) half a year ago (see the blog entry on the decision and on the critique by Willem Buiter)?

Here are some considerations to keep in mind.

- Is the Swiss France (CHF) overvalued? The following graph plots the nominal and real exchange rates since 1981 (the real rate is computed based on Swiss and Euro area producer price indices, 2010=100; data file).

Relative to the long-term average, the CHF currently is overvalued in real terms by 14%. In December 2014, it was overvalued by 4%; and in August 2011, by 11%. But in December 2007, it was undervalued by 21%. According to the real exchange rate metric, importers (households) thus suffered more in 2007 than exporters suffer today. For a related assessment based on consumer (Big Mac) prices, see this blog post. - The real exchange rate is just one metric to assess whether a currency is overvalued. There are many others, see for example this IMF paper or this book. Also, foreign exchange market participants are willing to buy and hold CHFs and EURs at the going market rate; they seem to think that the price is right.

- If the price were right and policy weakened the CHF, then Switzerland would trade off “competitiveness” of the export sector on the one hand, and expected capital losses on the country’s EUR holdings that would have to be purchased to temporarily strengthen the EUR on the other. Back-of-the-envelope calculations by my colleague Harris Dellas suggest that weakening the CHF would not be worth it, financially speaking.

- Even if, for whatever reason, society favored a weaker CHF it is not clear that the SNB should intervene. The SNB should only act if its mandate of pursuing price stability calls for such action. In the short run, a weaker CHF would indeed help to push the inflation rate in the desired range. In the longer run, however, a further lengthening of the SNB’s balance sheet (resulting from forex market interventions) could undermine the SNB’s flexibility, in particular if political constraints were to bind.

- This does not rule out, however, that other institutions in Switzerland could or should enter the exchange rate business. In principle, fiscal policy makers could institute a sovereign wealth fund that is financed by issuing CHF bonds and invested in EUR assets. Fiscal policy makers could also try to redistribute from those currently benefiting to those suffering from the CHF/EUR exchange rate. Export subsidies could be an instrument. They would be hard to implement though if one wanted to account for intermediate inputs.

- That Switzerland has an independent currency is a choice that reflects repeated, in depth deliberations. Advantages of pursuing an independent monetary policy include the option value to pursue price stability even if other currency blocs don’t; and the ensuing credibility benefits for Switzerland as a whole. Disadvantages include temporary, but potentially long-lasting real exchange rate misalignments that strain some groups (e.g., workers in the export sector) while benefiting others (e.g., consumers). These advantages and disadvantages do not come as a surprise; Switzerland has chosen them.

“Leben ohne Bargeld (Life without Cash),” SRF, 2015

SRF, Echo der Zeit, May 18, 2015. AUDIO, HTML.

- The availability of cash has costs: It eases tax evasion and money laundering and obstructs monetary policy at the zero lower bound.

- But it also has benefits.

- And the zero lower bound constraint can be relaxed otherwise, using taxes or an exchange rate.

Swiss National Bank

The NZZ runs a series of articles about the Swiss National Bank covering topics such as the bank’s history, organization and directorate, its transparency, profits or gold reserves.

Limits on Cash Withdrawals?

Andreas Valda reports in Der Bund about speculation that the Swiss National Bank (SNB) and/or commercial banks may limit cash withdrawals in response to negative CHF interest rates. According to the report, SNB press officer Walter Meier clarified the instruments at the SNB’s disposal as follows:

Die Nationalbank hat sich gemäss Gesetz bei der Ausgabe von Banknoten nach den Bedürfnissen des Zahlungsverkehrs zu richten; sie kann dafür Vorschriften über die Art und Weise, Ort und Zeit von Notenbezügen erlassen. … [Solche Vorschriften] würden gegenüber Bargeldbezügern bei der SNB gelten, also typischerweise Banken und sogenannte Bargeld-Verarbeiter.

1.20 No Longer—Buiter Critique

In a Citi research note, Willem Buiter discusses the SNB’s decision to discontinue the exchange rate floor of the Swiss Franc vis-a-vis the Euro. His main points are:

- The removal of the 1.20 floor on the CHF-euro exchange rate was a mistake.

- Superior policy alternatives existed.

- The old regime was indefinitely sustainable.

- Removing the lower bound on nominal interest rates would have been the best choice. This can be done one of three ways.

- The economic damage can be limited by restoring the exchange rate floor at a level not below the old one, and/or by eliminating the lower bound on nominal interest rates.

- The rest of the world can learn from the SNB’s experience with a -0.75% deposit rate.

Buiter refers to his earlier work on removing the lower bound on nominal interest rates that I have discussed elsewhere (here and here).

1.20 No Longer

The Swiss National Bank announced that it discontinues the exchange rate floor of CHF 1.20 vis-a-vis the Euro and lowers interest rates, to -0.75%. Markets are surprised. Michael Hunter writes in the FT:

The move came as a surprise since Thomas Jordan, SNB chairman, said as recently as December that Switzerland’s defence of the SFr1.20 rate against the euro was “absolutely necessary”.

A graph of the exchange rate series (source):

Negative Interest on SNB Sight Deposit Account Balances

The Swiss National Bank imposes negative interest rates on sight deposit account balances. The press release explains the details, including the calculation of exemption thresholds.

The Swiss “Vollgeldinitiative”

On June 3, 2014 the Swiss group “Monetäre Modernisierung” (monetary modernisation) started to collect signatures with the aim to force a national referendum on changes to the Swiss constitution. (The group needs to collect 100,000 signatures within an 18 month period in order to succeed.) The referendum would put the “Vollgeldinitiative” (sovereign money initiative) to vote, an initiative that seeks to fundamentally change Switzerland’s monetary system. The group “Monetäre Modernisierung” is part of a broader international movement with partner groups in the UK, the European Union and the US.

According to the proposal, deposit claims vis-a-vis commercial banks would be transformed into claims vis-a-vis the central bank and deposit liabilities of commercial banks would be transformed into liabilities of those banks vis-a-vis the central bank. Within a certain time span, commercial banks would have to repay those liabilities. Moreover, they would be prohibited from ever creating deposits again—that is, all money should be base money. The proposal envisions the Swiss National Bank to bring new base money into circulation by transferring reserves to the treasury, allowing the government to partly finance its expenditures by means of “original seignorage,” or to citizens. The Swiss National Bank could also lend reserves to banks, against interest, to accommodate fluctuations in money demand. (The resulting interest seignorage would add to government revenues as well.) The initiative aims at a complete separation between money and debt; accordingly, base money would be booked as equity in the central bank’s balance sheet rather than debt.

The proposal goes further than Irving Fisher’s 100% money plan and other proposals for full-reserve banking (and narrow banking) where banks are required to keep the full amount of deposited funds in cash/reserves (or very liquid, safe assets). Under the “Vollgeldinitiative,” the amount of deposited funds does not only have to be kept in cash/reserves but deposits are abolished altogether.

Some background information (in German):

- The text of the proposed constitutional amendment, with explanations.

- Background paper by one of the intellectual father’s of the initiative, Joseph Huber. He explains that the name “Vollgeld” is the short form of “voll gültiges gesetzliches Zahlungsmittel,” or legally speaking, “unbeschränktes gesetzliches Zahlungsmittel.”

Some quotes from the Q&A section on the technical implementation of the proposed reform (in German):

Die Girokonten der Kunden werden aus der Bankenbilanz herausgelöst und separat als Vollgeldkonten geführt. Die Guthaben auf den Girokonten bleiben eins zu eins bestehen, werden Vollgeld und somit zu gesetzlichen Zahlungsmitteln gleich Münzen und Banknoten. Ab dann ist nur noch die Nationalbank autorisiert Zahlungsmittel zu schöpfen. Dadurch geschieht mit dem unbaren Giralgeld heute das gleiche wie vor hundert Jahren mit den Banknoten. …

Das bisherige Banken-Giralgeld wird von Gesetzes wegen zu Vollgeld umdeklariert. Liesse man es dabei bewenden, kämen die Banken mit einem Schlag in den Besitz von Vollgeld, obwohl sie nicht das (neue) Vollgeld, sondern nur das (alte) Giralgeld geschaffen haben. Deshalb übernimmt die Nationalbank im Moment der Umstellung alle bisherigen Giralgeld-Verbindlichkeiten der Banken und verpflichtet sich damit, den Bankkunden anstelle von Bankengiralgeld Vollgeld auszuzahlen. Diese Auszahlung erfolgt sofort, damit die umlaufende Geldmenge nicht vermindert wird, und sie erfolgt auf Geldkonten ausserhalb der Bankbilanz, also auf Konten, auf die die Bank keinen Zugriff mehr hat. Für die Bankkunden ist diese Umstellung äusserst relevant: Sie sind jetzt im persönlichen Besitz von gesetzlichem Zahlungsmittel in der Höhe der bisherigen Sichtkonten, die vor der Umstellung blosse Geldversprechen auf Konten der Bank, aber kein Geld waren. …

Nach der Vollgeld-Umstellung gibt es nur noch Nationalbank-Geld. Das elektronische Geld ist genauso vollwertiges Geld wie heute Münzen und Banknoten. Das heisst, die Vollgeld-Zahlungsverkehrskonten der Kunden befinden sich dann nicht mehr in der Bilanz der Banken, sondern diese werden von Banken wie heute Wertpapierdepots verwaltet. Das Geld auf dem Konto gehört nur dem Kunden, wie das Bargeld im Tresor, und ist nicht mehr wie heute, eine Forderung an die Bank. So hat auch der Zahlungsverkehr nichts mehr mit Forderungen und Verpflichtungen zwischen den Banken zu tun, weshalb das heute übliche Banken-Clearing unnötig wird. Wenn ein Kunde eine Überweisung an einen Kunden tätigt, wird einfach Vollgeld von einem Konto auf das andere transferiert. Es passiert dann das, was fast alle Menschen heute meinen, was bei einer Überweisung geschieht.

Diese direkte digitale Übertragung von Vollgeld vereinfacht den Zahlungsverkehr, da die bisherige komplizierte Verrechnung von Forderungen und Verbindlichkeiten zwischen den Banken und eventueller Ausgleich mit Nationalbank-Guthaben entfällt. Statt dessen können Überweisungen sofort ausgeführt und gebucht werden, genauso wie heute der Kauf von Aktien und Wertpapieren. Die bisherige Wartezeit von mehreren Tagen, bis das Geld ankommt, entfällt. Nach wenigen Minuten wird man den Geldeingang auf dem Konto sehen können.

I discuss the initiative here.