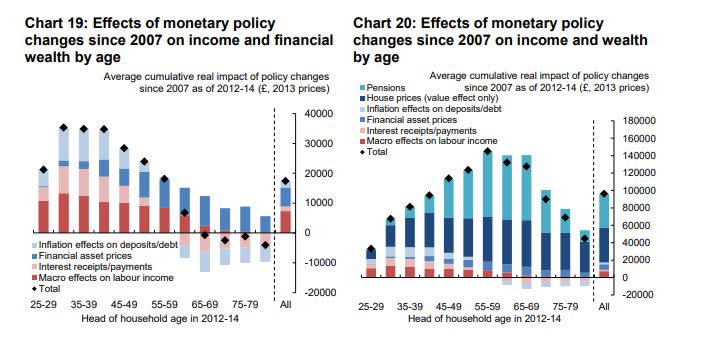

In a Staff Working Paper, the Bank of England’s Philip Bunn, Alice Pugh, and Chris Yeates discuss how monetary policy easing following the financial crisis affected income and wealth of different age groups.

The authors analyze survey panel data (ONS Wealth and Assets Survey) on households’ characteristics and balance sheet positions. They argue that

the overall effect of monetary policy on standard relative measures of income and wealth inequality has been small. Given the pre-existing disparities in income and wealth, we estimate that the impact on each household varied substantially across the income and wealth distributions in cash terms, but in percentage terms the effects were broadly similar. We estimate that households around retirement age gained the most from the support to wealth, but that support to incomes disproportionately benefited the young. Overall, our results illustrate the importance of taking a broad-based approach to studying the distributional impacts of monetary policy and of considering channels jointly rather than in isolation.