In the NZZ,

Tag Archives: Greece

Price Effects of Purchases of Greek Sovereign Debt by the ECB

In a CEPR discussion paper, Christoph Trebesch and Jeromin Zettelmeyer argue that

ECB bond buying had a large impact on the price of short and medium maturity bonds … However, the effects were limited to those sovereign bonds actually bought. We find little evidence for positive effects on market quality, or spillovers to close substitute bonds, CDS markets, or corporate bonds.

A multiple equilibria view of the crisis would probably suggest otherwise.

The IMF “In Principle” Approves Funding For Greece

In the FT, Mehreen Khan reports about the IMF’s conditional acceptance to lend to Greece.

The IMF’s “agreement in principle” (AIP) tool draws on a practice where the fund is able to greenlight its involvement in a debtor country, conditional on the government and its creditors agreeing to future debt relief measures.

Of course, the dispute about the merits of debt relief is unresolved. The IMF thinks Greek debt is ‘unsustainable’ and the European creditors should bear more losses, earlier on while some Euro area countries disagree. (For the numbers, see here).

Earlier in July, the European Stability Mechanism had approved a new cash injection (FT). This followed a dodgy compromise in June, as reported by Jim Brunsden in the FT:

Euro area ministers and the International Monetary Fund unveiled a deal … that will … sav[e Greece] … from default this summer. The IMF will join the bailout as a partner but withhold any money until euro area finance ministers give more detail on what debt relief they might offer Athens. …

Euro-area policymakers have been trying to reconcile competing EU and IMF visions of the €86bn programme and, crucially, whether it will make Greece’s debts sustainable.

Programme conditions set by euro area governments in 2015 included budget surplus targets that the IMF said were punishingly ambitious and unlikely to be met. The fund set out a different vision: lower primary surplus targets for Athens, coupled with comprehensive pension and tax reform and, crucially, far-reaching debt relief.

At the centre of the puzzle was Germany’s finance minister, Wolfgang Schäuble, who has insisted that the IMF must join if Greece is going to continue receiving tranches of bailout aid — but has also resisted significant debt relief commitments.

Given that the fund could not join up unless convinced that Greece’s debts were being put on to a sustainable path, the euro area and IMF had to find another solution — and it came in the form of asking Athens to do more.

To give the IMF confidence that Greece could hit budget surplus targets set by the euro area, Athens was asked to widen its income tax base and cut pensions. The measures, adopted in May, are estimated to be worth about 2 percentage points of gross domestic product.

In the meantime, Greece plans to regain market access by 2018 (FT).

Government Debt with State Contingent Coupons

On VoxEU, Myrvin Anthony, Narcissa Balta, Tom Best, Sanaa Nadeem, and Eriko Togo discuss the history of government debt with state contingent coupons and offer some lessons.

- In the mid-19th century, the Confederate states issued cotton-linked bonds

- In the late 1970s, Mexico issued oil-linked bonds

- In the 2000s, Turkey issued revenue-indexed bonds

- Since 2014, Uruguay issues nominal wage-issued bonds

- Some other examples (figure taken from the column):

- Obviously, confidence in data quality and thus, quality of institutions is important for the success of such issues.

State contingent securities also have been used in debt restructurings:

The first use of state contingent bonds in debt restructurings occurred in the Brady deals from 1989-97, which allowed commercial banks’ claims on debtor countries to be exchanged for tradable instruments, allowing the banks to clean up their balance sheets. Many of these instruments included ‘value recovery rights’, which envisaged additional debt payments in circumstances where the debtor country’s economic or terms of trade conditions improved substantially … Oil exporters generally linked the payments to oil prices, while other countries linked either to GDP or measures of the terms of trade. Many of the Brady instruments subsequently made significant ongoing upside payments (e.g. Bosnia and Venezuela), while in some cases sovereigns chose to repurchase the instruments as it became clear that upside payments would be triggered (e.g. Mexico, and Bulgaria in the mid-2000s).

More recently, ‘upside’ GDP-warrants have featured as part of the package of bonds issued to creditors in each of the three major restructurings of the past decade: Argentina (2005 and 2010), Greece (2012), and Ukraine (2015). In the case of Grenada (2015), the restructuring deal included instruments with both upside and downside features (Table 2).

Inflation linked bonds have been successful:

Inflation-linked bonds have a long history, dating back to a 1780 issuance by the State of Massachusetts … More recently, they emerged in Latin America in the 1950s and 1960s, in an environment of very high domestic inflation, and the UK became the first advanced economy to issue inflation-linked bonds in 1981. … the global stock of government inflation-linked bonds had grown to around USD 3 trillion by 2015 … Despite this recent growth, inflation-linked debt still accounts for a relatively small share of sovereign debt portfolios in most countries …

Related VoxEU column on policy implications.

Does Greece Need Official Debt Relief?

In a Peterson Institute working paper, Jeromin Zettelmeyer, Eike Kreplin, and Ugo Panizza conclude that the answer to that question depends on your assumptions.

The authors compare several scenarios, including

- scenarios A–C, the baseline scenario of the European institutions and two more pessimistic variants;

- scenario I which underlies the IMF reasoning and which assumes that “Greece will not undertake the structural reforms needed to achieve higher potential growth”;

- and scenario D, which corresponds to what Greece committed to when the third program was agreed, and which represents the German position.

They assume that interest rates on privately held debt rise with the debt-to-GDP ratio, and they use two “sustainability” metrics: The debt-to-GDP ratio (should fall), and gross financing needs as a share of GDP (should be smaller than 20%).

When running Monte Carlos simulations, the authors find that for each scenario, the assumptions about growth and primary surpluses are consistent with the conclusions drawn by the different institutions:

- In A (borderline) and D, debt is “sustainable.”

- Not so in B, C, and I, due to “accelerating substitution of official debt by more expensive borrowing from private sources”.

The authors then evaluate the plausibility of the scenario assumptions. They conclude that “international evidence does not support an adjustment path that envisages a primary surplus of above 3.5 percent for more than three to four years on a continuous basis and for more than seven years on an average basis” rendering B and C the most plausible scenarios, and suggesting that the debt is “unsustainable.”

In reaching their conclusions, the authors assume that primary surpluses in Greece will react to debt, inflation, and growth in line with the experience in other (developed) economies. (This means, for example, that surpluses rise as the debt burden increases, which seems to contradict the notion of debt overhang.) This is unconvincing, of course, if one takes the view underlying scenario D which presumes that feasible promises are kept. Or stated differently: Greece might well be able but not willing to pay—after all, in this very case official creditor intervention could have made sense in the first place although private lenders charged high interest rates. (With Harris Dellas, we make this argument precise in a paper in the Journal of International Economics.) Related, one can think of many reasons why the historical experience in other countries may be uninformative for the Greek case. The authors address one concern: They focus on episodes with very high debt-to-GDP ratios and find that in these cases, primary surpluses are maintained for longer. Moreover, there is the important question of measurement: The Greek debt-to-GDP ratio is not easily comparable with the ratio in other countries, see here and here, and most likely overstated.

Zettelmeyer, Kreplin, and Panizza make the case for a delay of Greece’s return to capital markets. In the conclusions, they write that

the debt relief measures put on the table by the Eurogroup in May 2016 could be sufficient to restore debt sustainability, but only if these measures are taken to an extreme. This means accepting an extremely long maturity extension of EFSF debts. In addition, it requires either substantial additional interest rate deferrals, or locking in significantly lower funding costs and hence lower interest rates than the EFSF currently expects, or a combination of both. While these measures are feasible within the red lines described by the Eurogroup, they are likely to be politically and/or technically difficult. Unless the EFSF manages to eke out substantial extra interest relief through creative long-term funding operations, its exposure to Greece will likely have to rise, possibly for decades, before it starts falling. A private sector creditor would not accept this type of restructuring because it gives the debtor country a strong incentive to default (or at least renegotiate) when the debt is at its peak.

… one way out of this dilemma would be to delay Greece’s return to capital markets, continuing to finance Greece through ESM programs until its private sector spreads are much lower than they are now. … this approach would lower the total need for debt relief and/or fiscal effort required to restore Greece to debt sustainability. While it would lead to a significant increase in official creditor exposure to Greece—requiring perhaps €100 billion of extra ESM financing—this is less than the rise in EFSF exposure that would be required in the Eurogroup’s approach, which aims to return Greece to private capital markets in 2018 while relying mainly on EFSF maturity extensions and interest rate deferrals … total official exposure to Greece would decline faster if ESM financing were to continue than if it were to end in 2018.

Importantly, they also point to the incentive effects of debt restructuring:

If [the threat of Grexit is essential to maintain incentives for reform] keeping the sword of Grexit … would help reduce debt levels only so long as Greece is being financed with cheap official funds. If, however, Greece returns to capital markets, any beneficial incentives of this approach would likely be offset by the risk premiums that private lenders would charge to a country whose euro membership remains at risk.

The official creditors will have to make up their minds: Not only the return on their lending is at stake, but also reform in Greece.

Deposit Outflows from Greek Banks, Again

In the FT, Mehreen Khan reports about the resurgence of deposit flight.

The IMF In Greece

The IMF has released a report with an ex-post evaluation of Greece’s 2012 Extended Fund Facility (Exceptional Access under the 2012 Extended Arrangement under the Extended Fund Facility with Greece).

A critical discussion by Charles Wyplosz on VoxEU.

The Greek authorities are more optimistic than IMF staff about the economy’s outlook.

Short-Term Debt Measures to Help Greece

The Eurogroup has approved short-term debt measures for Greece. The explanations on the ESM website are not very precise.

A chronology of the Greek debt crisis and the European institutions.

“The IMF and the Crises in Greece, Ireland, and Portugal”

The Independent Evaluation Office of the International Monetary Fund released a critical report on IMF supported policies in Greece, Ireland and Portugal. It questions the legitimacy of certain decisions. The executive summary states that

[t]he IMF’s pre-crisis surveillance mostly identified the right issues but did not foresee the magnitude of the risks … missed the build-up of banking system risks … shared the widely-held “Europe is different” mindset … Following the onset of the crisis, however, IMF surveillance successfully identified many unaddressed vulnerabilities, pushed for aggressive bank stress testing and recapitalization, and called for the formation of a banking union. …

In May 2010, the IMF Executive Board approved a decision to provide exceptional access financing to Greece without seeking preemptive debt restructuring, even though its sovereign debt was not deemed sustainable with a high probability. The risk of contagion was an important consideration … The IMF’s policy on exceptional access to Fund resources, which mandates early Board involvement, was followed only in a perfunctory manner. The 2002 framework for exceptional access was modified to allow exceptional access financing to go forward, but the modification process departed from the IMF’s usual deliberative process whereby decisions of such import receive careful review. Early and active Board involvement might or might not have led to a different decision, but it would have enhanced the legitimacy of any decision. …

The IMF, having considered the possibility of lending to a euro area member as unlikely, had never articulated how best it could design a program with a euro area country … where there was more than one conditional lender, the troika arrangement … proved to be an efficient mechanism … but the IMF lost its characteristic agility as a crisis manager. … the troika arrangement potentially subjected IMF staff’s technical judgments to political pressure …

The IMF-supported programs in Greece and Portugal incorporated overly optimistic growth projections. … Lessons from past crises were not always applied, for example when the IMF underestimated the likely negative response of private creditors to a high-risk program. …

The IMF’s handling of the euro area crisis raised issues of accountability and transparency, which helped create the perception that the IMF treated Europe differently. … Some documents on sensitive issues were prepared outside the regular, established channels; the IEO faced a lack of clarity in its terms of reference on what it could or could not evaluate; and there was no clear protocol on the modality of interactions between the IEO and IMF staff. The IMF did not complete internal reviews involving euro area programs on time, as mandated, which led to missed opportunities to draw timely lessons.

It lists the following recommendations:

… should develop procedures to minimize the room for political intervention in the IMF’s technical analysis. … should strengthen the existing processes to ensure that agreed policies are followed and that they are not changed without careful deliberation. … should clarify how guidelines on program design apply to currency union members. … should establish a policy on cooperation with regional financing arrangements. … should reaffirm their commitment to accountability and transparency and the role of independent evaluation …

In her response, the IMF’s Managing Director emphasizes that the IMF-supported programs did work in the cases of Ireland and Portugal (and in Cyprus) while Greece was a special case. She supports the report’s last four recommendations but disagrees with the premise of the first.

Greek Debt Sustainability

The IMF’s debt sustainability analysis paints a bleak picture … about previous IMF assessments and about the prospects for Greece.

New Questions about Greece’s Indebtedness

On the FT’s Alphaville blog, Matthew Klein reports about discrepancies between IMF and Greek (and EU) assessments of Greek net indebtedness. The IMF appears to report lower Greek financial asset holdings than the Greek Central Bank.

Matthew Klein quotes the Greek Central Bank:

We would like to clarify that the Bank of Greece compiles its financial accounts, from which data on the general government’s net debt are derived, according to European standards. The Bank of Greece’s data are compatible with the ECB’s and Eurostat’s rules (ESA 2010) regarding financial accounts and are used as an integral part in the production of the Monetary Union’s Financial Accounts. These data can also be accessed through the ECB’s Statistical Data Warehouse at http://sdw.ecb.europa.eu/reports.do?node=1000002429.

The IMF’s series on the general government’s net debt come from its WEO database and are not necessarily based on official statistics provided by Greek Statistical authorities. We understand that they may be compiled by IMF’s desk economists (and not its Statistics Department) and we cannot vouch for their accuracy, since they are adjusted according to the programming needs of the IMF. At first glance, they appear to be based on outdated information contained in past EDP [excessive deficit procedure] documentation.

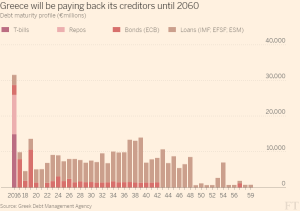

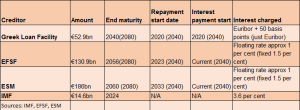

Greek Debt: Now and Then

In the FT, Mehreen Khan offers a “Greek debt dilemma cheat sheet.”

- Face value: EUR 321 billion, thereof EUR 248 billion owed to official creditors.

- Official creditors: Eurozone countries (Greek loan facility), eurozone rescue funds (EFSF and ESM), IMF, ECB.

- Maturity profile:

- IMF proposal for restructuring:

Measuring (Greek) Indebtedness

In a Vox column, Daniel Dias und Mark Wright propose various measures of the Greek, Portuguese and Irish public debt burden and emphasize the large variability of these measures.

The following figure, taken from Dias and Wright, shows the scheduled principal and interest payments of Greece, Portugal and Ireland as a percentage of 2014 GDP in the respective country. Not all public debt components are accounted for.

Dias and Wright write:

[B]oth Portugal and Ireland face far larger cash flow requirements, relative to the size of their economies, than Greece for the next ten years. [A]fter this ten-year period, the required repayments on Greece’s debt will far exceed those of Portugal and Ireland, measured as a fraction of their economies. [W]hether or not we view Greece as more or less indebted than Portugal and Ireland depends on how we weigh cash flows in the near future (next ten years) versus cash flows in the far future (more than ten years).

… we can discount a country’s entire debt repayment cash flows by the interest rates embodied in their currently traded debts to obtain an estimate of the market value of a country’s debt. This assumes that the likelihood of repayment of Greece’s EFSF debt, for example, is the same as that for privately held bonds. Under these assumptions, as shown in Table 5, Greece appears to have less than half as much debt as either Portugal or Ireland. These numbers are closer to the estimates computed under the IPSAS standard, which records a debt at market value at the time of issue, and allows for the accretion of this debt if the contracted interest rate on the debt is less than the yield to maturity of the debt. This approach has the counterintuitive implication that the more likely a country is to default, the less indebted it will look.

Dias and Wright contrast a conventional face-value debt measure (the sum of the blue bars corresponding to principal repayment obligations in the figure) with more informative measures. With the latter, Greek indebtedness typically is not as high compared with the other countries as with the first measure.

See also this earlier post and this earlier post on the topic.

Structural Problems in Greece—And in the EU

In a Project Syndicate column, Edmund Phelps documents structural problems in Greece. He emphasizes that other EU countries face similar challenges.

Good and Bad Reasons for Greek Debt Relief

In a Vox column, William Cline argues that

it is important to recognise that the headline debt figure overstates the true burden of Greek debt. Because most of the debt is owed to official sector partners at concessional interest rates, the interest burden is much lower than would usually be associated with the same gross debt. Under the Fund’s own criterion for sustainability in these circumstances (ratio of gross financing needs to GDP), Greek debt should remain within an acceptable range at least through 2030. It is questionable to base debt relief policy on problems that might or might not materialise beyond such a distant horizon. Moreover, most of the projected sharp increase in debt could be avoided by carrying out bank recapitalisation directly from the European Stability Mechanism (ESM) to the banks, rather than through the Greek government as an intermediary.

There is still an important potential role for using interest rate relief, for two purposes. First, if fiscal balances fall below target because of lower than expected growth (rather than policy slippage), a portion of interest otherwise accruing could be forgiven to avoid the need for additional fiscal tightening and its recession-aggravating consequences. Second, because Greek unemployment is at depression levels (26%), special employment programmes would seem appropriate, and forgiving a portion of the interest due could provide a significant source of funding for this purpose.

Cline also discusses the claim that Eurozone loans mainly saved Eurozone banks:

- not true, they received only one-third of the official sector support;

that the Troika called for too much austerity:

- true, the cyclically adjusted primary balance swung from -13.2% of GDP in 2009 to +5.3% in 2014, much more than in Portugal, Spain or Ireland;

- but Greece was cut off from financial markets;

- and Eurozone support as a share of GDP exceeded 100% in Greece compared with roughly 30% in Ireland and Portugal or 5% when the US supported Mexico;

- “even at the upper bound of the IMF’s upward-revised multipliers (1.7), smaller spending cuts would not have boosted GDP and revenue by enough to pay for themselves;”

- and the adjustment mostly occurred in the early years when spreads were high and would have been even higher with less adjustment.

Cline estimates that the third rescue package will raise Greek net debt by 10-15 billion Euros.

Loans vs. Transfers in the Third Greek Bailout

Hugo Dixon estimates that the new loans to Greece exceed the present value of repayments by roughly 40 billion Euros. That is, half of the new loans are transfers.

Eurozone Finance Ministers Approve Third Greek Bailout

In the FT, Duncan Robinson and Christian Oliver report about Eurozone finance ministers’ approval of the third bailout for Greece, amounting to 86 billion Euros.

Contrary to Germany’s recent demands, the approval came in spite of the fact that the IMF has not committed to participate in the new program. In fact, the IMF has committed not to participate unless Greece’s debt burden is further reduced. Finance ministers effectively promised such further cuts in the future.

The deal falls short of what the German government had hoped to secure (see also this previous blog post).

MoU between Greece and its Creditors

In the Guardian, Heather Stewarts reports about the contents of the memorandum of understanding that the Greek government and its creditors have agreed on. It contains four pillars:

- Fiscal sustainability, including pension reform and social welfare review;

- Financial stability, including bank recapitalization;

- Growth, competitiveness, investment, including liberalization of consumer markets, labor markets and professions;

- Modern state and administration, including judicial reform and anti corruption measures.

Reforms Under Way In Greece

In an Ekathimerini article, Dimitra Manifava reports about the reform measures under way following recent negotiations between Greece and her international creditors.

Greece’s Financial Position Is Widely Misreported

In an FT letter to the editor, Ian Ball, the Chair of CIPFA International (Chartered Institute of Public Finance and Accountancy), argues that Greece’s financial position is widely misreported. He writes:

While the debt burden is commonly cited as being between 175 and 180 per cent of gross domestic product, this number is incorrect and indefensible because it is based on the face value of Greece’s debt that doesn’t take into account long maturities and concessional interest rates, as well as grace periods.

Greek debt, calculated on an International Public Sector Accounting Standards (IPSAS) basis, is significantly lower, and at the end of 2013 was 68 per cent of GDP. If this is not an appropriate method for measuring debt, then every company on major stock exchanges around the world has got its debt measurement wrong. In neither accounting standards nor economic principle is debt measured at face value. This pervasive misunderstanding of Greece’s real fiscal position has seen agreements reached between Greece and its creditors that do not address the real problem and instead may actually intensify it.

See also my earlier blog post.

Advisors of the Greek Government

In a Politico column, Yannis Palaiologos bitterly complains about the counter productive role that Paul Krugman, Joseph Stiglitz, Jeffrey Sachs and James Galbraith played in supporting members of the Greek government in the run up to the recent climax of the Greek crisis.

Sovereign Debt Seniority

In a Vox column, Matthias Schlegl, Christoph Trebesch, and Mark Wright document an implicit seniority structure of external sovereign debt: IMF > Multinational > Bonds > Bilateral > Banks > Trade Credit (see the figure).

They argue that Greece’s recent default on the IMF constitutes an outlier.

… Greece in 2015 is clearly an outlier case, having defaulted on the most senior creditor (the IMF), while continuing to service historically more junior creditors. The evidence also suggests that the Eurozone rescue loans, which are essentially bilateral (government-to-government) credit, are likely to be a junior creditor class going forward. The evidence also rationalises why Greece may have an interest in exchanging the debt it owes to the IMF and the ECB into loans to the European Stability Mechanism, which is likely to be junior debt in the future, as discussed in the run-up to the July Eurozone summits. Policymakers should be aware of the associated changes in seniority and repayment incentives.

Greece and Austerity

In a Project Syndicate column, Edmund Phelps argues that it is not “austerity” which is to blame for Greece’s plight.

So spending more is not the remedy for Greece’s plight, just as spending less was not the cause. What is the remedy, then? No amount of debt restructuring, even debt forgiveness, will suffice to achieve prosperity (in the form of low unemployment and high job satisfaction). Such measures would only help Greece to revive government spending. Then the economy’s stultifying corporatism – clientelism and cronyism in the public sector and vested interests and entrenched elites in the private sector – would gain a new lease on life. The European left may advocate that, but it would hardly be in Europe’s interest.

The remedy must lie in adopting the right structural reforms. Whether or not the reforms sought by the eurozone members raise the chances that their loans will be repaid, these creditors have a political and economic interest in the monetary union’s survival and development. They should also be ready to help Greece with the costs of making the necessary changes.

“Grollaps (Grollapse),” NZZ, 2015

Neue Zürcher Zeitung online, August 1, 2015. HTML. Adapted from Ökonomenstimme, July 16, 2015. HTML.

The collapse in Greece is a consequence of major institutional problems. See earlier blog post.

“Institutionelle Schwächen der EU (Institutional Problems in the EU),” FuW, 2015

Finanz und Wirtschaft, July 15, 2015. PDF. Ökonomenstimme, July 16, 2015. HTML.

The collapse in Greece is a consequence of major institutional problems:

- Political decision makers in Berlin, Paris, Brussels, Frankfurt and Washington didn’t follow the rules. This seemed optimal ex post, but is suboptimal ex ante (see Kydland and Prescott).

- The ECB’s mandate is unclear.

- The monetary system is fragile.