In a recent paper, Robin Greenwood, Sam Hanson, Josh Rudolph and Larry Summers discuss the joint effect of Fed and Treasury policy on the maturity structure of government liabilities in the hands of the private sector. John Cochrane commends the paper in a blog post.

Greenwood, Hanson, Rudolph and Summers make several points. First, “monetary and fiscal policies have been pushing in opposite directions in recent years.” In spite of QE, long-term government debt held by the private sector increased, mostly due to government deficits but also because the government lengthened the maturity of its debt. Second, Fed and Treasury policies largely are uncoordinated. They argue that this is suboptimal, in particular when the Fed strongly intervenes as it did in the recent QE episodes.

The Federal Reserve has focused purely on the effects that its bond purchases were expected to have on long-term interest rates and, by extension, the economy more broadly. … it completely ignored any possible impact on government fiscal risk, even though the Federal Reserve’s profits and losses are remitted to the Treasury. Conversely, Treasury’s debt management announcements and the advice of the Treasury Borrowing Advisory Committee (TBAC) have focused on the assumed benefits of extending the average debt maturity from a fiscal risk perspective, and largely ignored the impact of policy changes on long-term yields. To the extent that the Federal Reserve and Treasury ever publicly mention the other institution’s mandate, it is usually in the context of avoiding the perception that one institution might be helping the other achieve an objective. Specifically, the Fed does not want to be seen as monetizing deficits, while the Treasury has been reluctant to acknowledge the Fed as anything more than a large investor.

Third, they argue that from a consolidated government policy perspective, the optimal debt maturity structure is rather short. This saves on interest payments to the private sector (on average) and reduces “liquidity transformation” by the financial sector with dangerous consequences for financial stability. They downplay the risk sharing benefits of longer-term debt and argue that short-term debt has additional advantages at the zero lower bound.

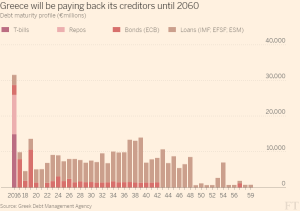

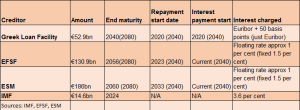

Pages 11-12 contain the following figure, among others: