In the NZZ,

Tag Archives: European Stability Mechanism

The IMF “In Principle” Approves Funding For Greece

In the FT, Mehreen Khan reports about the IMF’s conditional acceptance to lend to Greece.

The IMF’s “agreement in principle” (AIP) tool draws on a practice where the fund is able to greenlight its involvement in a debtor country, conditional on the government and its creditors agreeing to future debt relief measures.

Of course, the dispute about the merits of debt relief is unresolved. The IMF thinks Greek debt is ‘unsustainable’ and the European creditors should bear more losses, earlier on while some Euro area countries disagree. (For the numbers, see here).

Earlier in July, the European Stability Mechanism had approved a new cash injection (FT). This followed a dodgy compromise in June, as reported by Jim Brunsden in the FT:

Euro area ministers and the International Monetary Fund unveiled a deal … that will … sav[e Greece] … from default this summer. The IMF will join the bailout as a partner but withhold any money until euro area finance ministers give more detail on what debt relief they might offer Athens. …

Euro-area policymakers have been trying to reconcile competing EU and IMF visions of the €86bn programme and, crucially, whether it will make Greece’s debts sustainable.

Programme conditions set by euro area governments in 2015 included budget surplus targets that the IMF said were punishingly ambitious and unlikely to be met. The fund set out a different vision: lower primary surplus targets for Athens, coupled with comprehensive pension and tax reform and, crucially, far-reaching debt relief.

At the centre of the puzzle was Germany’s finance minister, Wolfgang Schäuble, who has insisted that the IMF must join if Greece is going to continue receiving tranches of bailout aid — but has also resisted significant debt relief commitments.

Given that the fund could not join up unless convinced that Greece’s debts were being put on to a sustainable path, the euro area and IMF had to find another solution — and it came in the form of asking Athens to do more.

To give the IMF confidence that Greece could hit budget surplus targets set by the euro area, Athens was asked to widen its income tax base and cut pensions. The measures, adopted in May, are estimated to be worth about 2 percentage points of gross domestic product.

In the meantime, Greece plans to regain market access by 2018 (FT).

Short-Term Debt Measures to Help Greece

The Eurogroup has approved short-term debt measures for Greece. The explanations on the ESM website are not very precise.

A chronology of the Greek debt crisis and the European institutions.

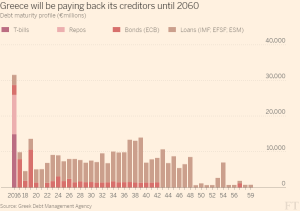

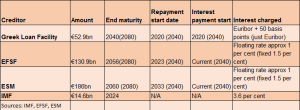

Greek Debt: Now and Then

In the FT, Mehreen Khan offers a “Greek debt dilemma cheat sheet.”

- Face value: EUR 321 billion, thereof EUR 248 billion owed to official creditors.

- Official creditors: Eurozone countries (Greek loan facility), eurozone rescue funds (EFSF and ESM), IMF, ECB.

- Maturity profile:

- IMF proposal for restructuring:

Accounting, Greek Debt, and Realism (Part Three)

In a Vox blog post, Julian Schumacher and Beatrice Weder di Mauro offer meaningful Greek government debt statistics. They quote an ESM estimate according to which the 2012 restructuring of Greek debt owed to official lenders amounted to a 50% haircut (see this previous blog post). And they argue that the net present value of Greek government debt relative to GDP amounted to 93% (presumably in 2013 or 2014), in line with other estimates (see this previous blog post).

How Greece Benefitted from European Debt Relief

The 2014 Annual Report of the ESM contains a box on “How Greece Benefitted from European Debt Relief” (p. 29). The concluding paragraph states:

The measures correspond to substantial economic debt relief … Considering these maturity extensions and interest rate deferrals over the entire debt servicing profile from a net present value (NPV) perspective shows a reduction in the overall debt burden and reveals implicit savings. … Stretching out principal repayment schedules over such an extended period of time, along with interest payment deferral, imply that these payments account for substantially less in NPV terms when assessed from the Greek side taking into account the financial market perspective.

No explanation is given as to why the NPV perspective should only reveal “implicit” savings. Whether a Euro must be paid in ten years or in twenty does make a difference, and a rather substantial one at the relevant interest rates. A footnote attached to the last sentence of the above quote is rather obscure as well. It says:

It should be noted that this does not entail any financial loss or write-down from an EFSF perspective. The EFSF is fully repaid; Greece has to cover any financing costs related to the agreed interest rate deferral in line with the amendment of the Master Financial Assistance Facility Agreement.

See the earlier post on how to correctly account for sovereign debt.

Last Exit Before Grexit?

Nicolai Kwasniewski reports in Der Spiegel about the last (?) chance for Greece to avoid Grexit.

- By Wednesday night, Greece has to submit a request for an ESM program.

- After discussing the request, Euro finance ministers will ask the “institutions” to evaluate it and to assess whether the stability of the Euro zone is under threat (a prerequisite for ESM funding), the program is sustainable etc.

- Greece has to submit detailed reform proposals until Thursday. To be acceptable, they will have to satisfy stricter requirements than those the Greek voters recently rejected.

- Euro finance ministers will evaluate the proposals on Saturday.

- EU prime ministers and presidents have the last word on Sunday.

Peter Spiegel, Anne-Sylvaine Chassany and Duncan Robinson report in the FT.

A Plan for Greece

In the FT, Willem Buiter proposes a 5 point plan for a way out of the Greek debt crisis:

- Greece effectively regains sovereignty and can do whatever it pleases, with some exceptions, see below.

- Greek debt held by the ECB is bought by the ESM: The ESM extends long-term, low-interest financing to Greece which Greece uses to repay the ECB debt. “Since most of Greece’s other sovereign liabilities have long maturities and deferred interest payments, payments to creditors would fall sharply.”

- No further financing by the IMF, the ESM or other official sources is extended to Greece.

- The ECB does no longer accept any Greek government debt paper as collateral or for purchase.

- Commercial banks in Greece are recapitalized or restructured using funds from the Hellenic Financial Stability Fund and other sources. The ECB bars Greek banks from accepting any Greek government debt paper.

The plan would require additional European taxpayer money for the ECB-ESM debt swap and the bank recapitalization. It would isolate the Greek banks from the mayhem triggered by government default.

Update: 7 July 2015

A related proposal by Willem Buiter and Ebrahim Rahbari.

Pari Passu and Collective Action Clauses: The New World

An IMF staff report published in September and entitled “Strengthening the Contractual Framework to Address Collective Action Problems in Sovereign Debt Restructuring” discusses recent legal developments of relevance for sovereign debt markets and implications for the sovereign debt restructuring process.

The New York court decisions (NML Capital, Ltd v. Republic of Argentina) have rendered a holdout strategy more likely to succeed. This tends to exacerbate collective action problems and raises the risk of more protracted debt restructuring processes. Market participants, including the International Capital Markets Association (ICMA) are discussing contractual clarifications and modifications in response to this challenge. The IMF observes these discussions and supports the preliminary results.

The New York court decisions established a broader interpretation of the standard pari passu clause in sovereign debt contracts. Specifically, they extended the standard notion of “protection of a creditor from legal subordination of its claims in favor of another creditor” to the broader notion that a sovereign must pay creditors on a pro rata basis. The court decisions prohibited Argentina from making payments to holders of restructured bonds unless it paid holdout creditors on a pro rata basis, and it prevented banks from making payments on Argentina’s behalf. In this context, the decisions also interpret the U.S. Foreign Sovereign Immunities Act. The scope of the rulings is not clear, not least because the decisions also refer to Argentina’s “course of conduct.” If interpreted broadly, the court decisions change the legal framework and are likely to complicate the restructuring of New York law-governed debt contracts (while probably not affecting London law-governed contracts).

Box 1 of the report discusses in detail the history of the Argentine litigation in the U.S. The report also contains an annex on the history of pari passu clauses in New York law-governed sovereign debt contracts.

Sovereign issuers have already reacted to the court decisions, by modifying the pari passu clauses in debt contracts. Also, ICMA has proposed a new standard pari passu clause, emphasising equal ranking as opposed to pro rata payments.

Collective action clauses enable a qualified majority of bondholders (e.g., 75%) of a specific bond issuance to bind the minority to the terms of a restructuring agreement. If collective action clauses operate on a series-by-series basis rather than on the total stock of debt then a blocking minority can more easily be formed and a strategy of holding out is more likely to succeed, in particular in light of the recent New York court decisions. The possibility to aggregate claims across bond series for voting purposes works in the opposite direction. Some countries have included aggregation clauses in the debt contracts, and the ESM treaty requires standardised aggregation clauses (“Euro CACs”) in Euro area government bonds as well. These clauses feature a “two limb” voting structure, requiring a majority of bondholders in each series and across all series but a lower quorum (e.g., 66%). Currently, “single limb” procedures are being discussed. These would solely require a majority across all series. To prevent abuse, such single limb procedures would have to be accompanied by safeguards that ensure inter-creditor equity, in particular a restriction to offer all affected bondholders the same (menu of) instruments. (Offering the same (menu of) instruments would generally imply that some creditors suffer larger restructuring losses than others, depending on the type of instruments they held initially. But already today, this is common and generally accepted.)

Box 2 of the report discusses the history of collective action clauses. Box 3 of the report discusses disenfranchisement provisions. Their purpose is to limit the risk of a sovereign manipulating voting processes by influencing votes of entities under its control.